If you grew up in Korea like I did, the words “high interest loan” probably send a chill down your spine. In Korea, borrowing money at 10% interest is the kind of thing that ends badly — families destroyed, people disappearing overnight. It carries a shame so heavy that most people won’t even say the words out loud.

So when I first heard about hard money loans, I was terrified.

Then I learned what they actually were. And everything changed.

What Is a Hard Money Loan?

A hard money loan is a short-term, asset-based loan used primarily by real estate investors. Unlike a conventional mortgage — which looks at your income, your W-2s, your credit history, and your entire financial life — a hard money loan is based almost entirely on the value of the property you’re buying.

This matters enormously for investors. When you’re trying to fix and flip a property, a conventional loan won’t work. Banks want two years of W-2 income history. They want stable employment. They want paperwork that takes months to process. By the time a bank approves your loan, someone else has already bought the property, renovated it, and put it back on the market.

Hard money lenders move fast. We’re talking days, not months.

My First Hard Money Loan — And What I Didn’t Understand

I came to the United States not long after my divorce. My English was almost nonexistent. My husband had handled all of our finances during our marriage, which meant I was starting from zero — not just emotionally, but financially.

I wanted to invest in real estate. I had always been drawn to it. But I had no W-2 income, no two-year employment history in the US, and no idea how any of this worked. A conventional loan was completely out of reach.

That’s when I found a Korean-owned company in Los Angeles that handled everything — finding the property, managing the renovation, selling it — in exchange for splitting the profits 50/50. They used hard money loans to finance the deals. I put down 20% and they handled the rest.

My interest rate was around 10%. My monthly interest payments were $3,300 to $3,500. The plan was to flip the property in three to four months.

I put down $170,000 on my first deal. That’s not a typo. $170,000 — because Los Angeles real estate prices are so high that a 20% down payment on an investment property costs that much. At the time, I had no idea that other American cities existed at different price points. I genuinely thought all of America cost the same as California. I didn’t know yet that $170,000 in Philadelphia could buy you an entire house.

The ROI Problem Nobody Told Me About

Here’s where the math gets uncomfortable.

My first flip took four months. I made $20,000. My second flip took eight months. I made $20,000. My third flip took thirteen months. I made $20,000.

Every single time: $20,000.

I invested $170,000. I waited an average of eight months. I walked away with $20,000.

$20,000 ÷ $170,000 = 11.7% ROI — across eight months. Annualized, that’s less than 9%.

You could have put that money in a high-yield savings account and done almost as well — without the stress, the hard money interest, or the thirteen months of waiting.

Something was off. I knew it even then. But I was new to the country, my English wasn’t strong enough to ask the right questions, and I trusted the company completely because they spoke my language. I assumed shared culture meant shared interests.

It didn’t.

The company was taking their 50% cut off the top, after all costs. The hard money interest, the renovation costs, the agent commissions, the closing costs — all of that came out first. Then they split what was left. By the time I saw my share, the number had been quietly compressed in ways I couldn’t track because I didn’t know what to look for.

How Hard Money Loans Actually Work

Now that I understand the system, let me break it down so you don’t make the same mistakes I did.

Interest rates: Hard money loans typically carry rates between 8% and 15%, depending on the lender, the market, and your track record. Mine was around 10%.

Term: Short-term — usually six to twelve months. Designed to be paid off when you sell or refinance into a conventional loan.

Points: Most hard money lenders charge 1–3 points upfront. One point = 1% of the loan amount. On a $200,000 loan, two points means $4,000 paid at closing before you’ve touched the property.

Speed: This is the real value of hard money loans. A good lender can fund in five to ten days. In a competitive market like Philadelphia, that speed is the difference between getting the deal and watching someone else get it.

The math you must do before you borrow:

Monthly interest = Loan Amount × (Annual Rate ÷ 12)

On a $150,000 loan at 10%: $150,000 × (10% ÷ 12) = $1,250/month

Every month your project runs over schedule costs you $1,250. Three months over costs you $3,750 — directly out of your profit. This is why timeline management is everything in fix and flip. Not because of stress. Because of math.

Hard Money Loans in Philadelphia vs. Los Angeles

This is the part that makes me laugh now, even though it hurt at the time.

In Los Angeles, a fix and flip might involve a purchase price of $600,000–$800,000. A hard money loan at 10% on $500,000 costs $4,166 per month in interest alone. The margins are thin, the stakes are enormous, and one bad month can wipe out an entire project’s profit.Want to run your flip numbers before you borrow? Try the Philly Flip Profit Calculator.

In Philadelphia, I can find investment-grade properties for $80,000–$150,000. A hard money loan at 10% on $100,000 costs $833 per month. The pressure is completely different. The margin for error is much more forgiving.

If I had known Philadelphia existed when I was starting out in LA — if I had understood that America has many cities at many price points, not just the one I happened to land in — I would have started here.

I’m here now. That’s what matters. See exactly what a Philadelphia deal looks like with the BRRRR Calculator.

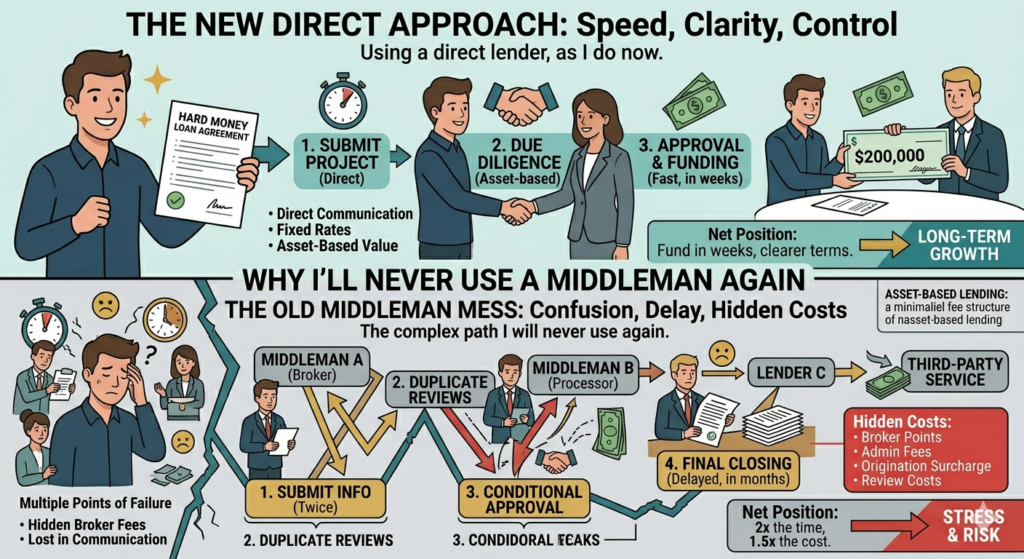

Why I’ll Never Use a Middleman Again

The fix and flip company I worked with in LA wasn’t doing anything illegal. They were running a business, and their business model worked well — for them.

But here’s what I know now that I didn’t know then: every layer of middleman between you and your investment compresses your return. The company took 50% of profits. The hard money lender took 10% annually. The agents took 5–6% on the sale. By the time all of that came out, my $170,000 investment returned $20,000 over eight months.

Direct investing means more work. You have to find your own deals. Manage your own contractors. Understand your own numbers. Negotiate directly with lenders.

But you also keep your full share of the profit.

That’s why I moved to Philadelphia. That’s why I walk Germantown Avenue every day looking at properties. That’s why I’m studying for my real estate license and learning everything I should have learned before I ever wired that first $170,000. If you’re figuring out your financing options, the DSCR Loan Qualifier is a good place to start.

Philadelphia is my second chance. And this time, I’m doing it myself.

Not financial advice — just someone doing a lot of research and asking a lot of questions.