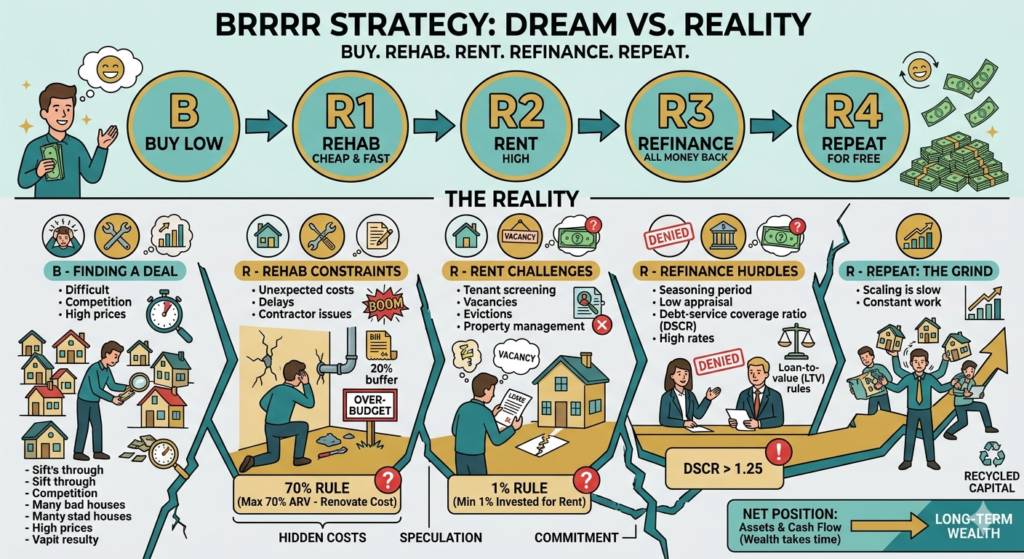

If you’ve spent any time in real estate investing content — on TikTok, YouTube, or Reddit — you’ve probably heard someone explain the BRRRR strategy like it’s a magic trick. Buy a distressed property. Fix it up. Rent it out. Refinance to pull your money back out. Repeat forever. Build wealth with no money down.

The BRRRR strategy sounds almost too clean.

I’m not here to tell you it doesn’t work. It does — for investors who run the numbers correctly, have the right financing in place, and don’t make the mistakes I made on my first deal. But I want to walk you through what actually happens at each step of the BRRRR strategy, because the version you see on social media leaves out a lot.

BRRRR Strategy Step 1: Buy Below Market Value

The whole BRRRR strategy starts with finding a property significantly below market value. Not a little below. Significantly. You’re looking for distressed properties — foreclosures, estate sales, sheriff sales, properties that need substantial work — priced low enough that after renovation, the numbers still make sense.

In Philadelphia, this is actually more realistic than in most major cities. I walk through Germantown every day looking at properties. There are rowhouses here that need serious work but sit in neighborhoods where renovated comps are selling for $200,000 to $300,000. That gap is where BRRRR investors make their money.

The rule most investors use: your purchase price plus renovation costs should not exceed 75% of the after repair value. If you can’t buy cheap enough to hit that number, walk away.

BRRRR Strategy Step 2: Rehab Without Blowing the Budget

This is where most beginners underestimate their costs. Contractor bids come in lower than reality. Unexpected problems appear behind walls. Timelines stretch. Every extra month costs you money in carrying costs — whether that’s hard money loan interest, property taxes, or utilities.

The investors who do the BRRRR strategy well build a contingency buffer of at least 10% to 20% on top of their renovation estimate. They also have contractor relationships already in place before they close on the property.

I didn’t have any of that on my first deal in Los Angeles. I trusted people I shouldn’t have trusted and paid for it.

BRRRR Strategy Step 3: Rent It Right

Before you buy, you need to know what the property will rent for after renovation. Not what you hope it will rent for. What comparable units in that specific neighborhood are actually renting for right now.

In Philadelphia, rental demand is strong — particularly for renovated rowhouses near transit. But rental rates vary significantly by neighborhood. A renovated two-bedroom in West Philadelphia rents for a different number than the same unit in Fishtown. Do your research before you make an offer.

Your rental income needs to cover your future mortgage payment after refinancing, plus taxes, insurance, and maintenance. If it doesn’t, the BRRRR strategy falls apart at this step.

BRRRR Strategy Step 4: Refinance and Pull Your Money Out

This is the step that makes the BRRRR strategy different from a standard buy-and-hold approach. After your renovation is complete and the property is rented, you refinance based on the new appraised value — not what you paid for it.

If the numbers worked on the buy side, the refinance should return most or all of your original cash investment. That’s the capital you use to fund your next deal.

Here’s what the math looks like on a real Philadelphia example:

Purchase price: $95,000 Renovation: $45,000 Total invested: $140,000 After repair value: $220,000 Refinance at 75% LTV: $165,000

That $165,000 refinance loan covers your $140,000 investment and puts $25,000 back in your pocket. Your tenant’s rent covers the mortgage. You own a cash-flowing rental property with none of your original money still in the deal.

That’s the version of the BRRRR strategy that works.

BRRRR Strategy Step 5: Repeat — But Only If the Numbers Work

With your capital returned, you find the next deal and do it again. Over time, you build a portfolio of cash-flowing properties without needing to save up a new down payment for each one.

In theory.

In practice, the refinance doesn’t always return 100% of your capital. Appraisals come in lower than expected. Lenders apply stricter criteria than you anticipated. The rental income barely covers the mortgage after all expenses. Each of these gaps requires cash you need to have available.

What I’d Tell Someone Starting Out

Run the numbers before you fall in love with a property. Use a calculator — I built one specifically for the BRRRR strategy — and stress test your assumptions. What happens if the appraisal comes in 10% lower than you expected? What happens if the property sits vacant for two months?

The BRRRR strategy works. But it works when the math works, not when you need it to work.

Start with one deal. Learn the process. Build your contractor relationships. Understand your local rental market. And don’t let anyone on social media make you feel like you’re behind because you’re being careful.

Being careful is how you stay in the game.

Use the BRRRR Calculator below to run the numbers on your next deal before you make an offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions.