The $3,000 Monthly Interest Payment Nobody Warned Me About

When I invested in my first fix-and-flip in Los Angeles, I knew there would be a hard money loan involved. What I didn’t fully understand was what that hard money loan was actually costing me every single month while the renovation was happening.

The answer was somewhere around $3,000. Every month. Whether the renovation was on schedule or not. Whether the property was generating any income or not. Just gone, as interest, to a hard money lender I had never spoken to directly.

That’s what hard money loans do. And if you’re getting into fix-and-flip investing without understanding how they work, you need to read this first.

What Is a Hard Money Loan?

A hard money loan is a short-term loan used primarily for real estate investment — specifically for properties that need renovation and can’t qualify for traditional financing in their current condition.

Traditional banks won’t lend on a distressed property. Hard money lenders will. They move fast, they don’t care as much about your credit score, and they base the hard money loan primarily on the value of the property itself.

The tradeoff is cost. Hard money loans are expensive.

What Hard Money Loans Actually Cost

Here’s what you need to understand before you sign anything:

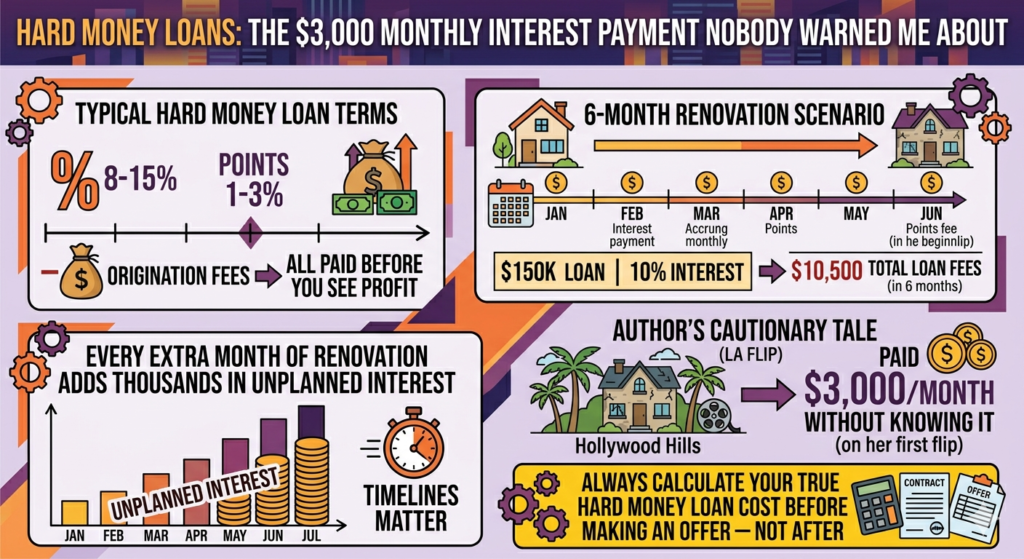

Hard money loans typically charge interest rates between 8% and 15% annually. But unlike a traditional mortgage where you’re paying down principal each month, most hard money loans are interest-only. You pay the interest every month and repay the full principal when you sell or refinance.

On top of the interest rate, hard money loan lenders charge origination fees — typically 1 to 3 points, meaning 1% to 3% of the loan amount, paid upfront at closing.

Let me show you what this looks like in real numbers.

Say you borrow $150,000 at 10% annual interest with a 2-point origination fee for a 6-month renovation project.

Monthly interest: $150,000 × 10% ÷ 12 = $1,250 per month Total interest over 6 months: $7,500 Origination fee: $150,000 × 2% = $3,000 True total cost of the hard money loan: $10,500

That $10,500 comes directly out of your profit before you see a dollar.

Now imagine the renovation takes 9 months instead of 6. That’s an extra $3,750 in interest you didn’t plan for. This is why renovation timelines matter so much in fix-and-flip investing.

Why I’ll Never Use a Middleman Again

On my Los Angeles deal, I never dealt directly with the hard money lender. The company I invested with handled all of that. I just saw the final number at the end — $20,000 profit on a $170,000 investment over 13 months.

What I didn’t see was exactly how much of my return went to hard money loan interest, how long the loan was actually outstanding, or whether the terms were competitive. I trusted people I shouldn’t have trusted with information I should have demanded to see myself.

Direct investing means more work. You have to find your own deals. You have to talk directly to lenders. You have to understand every line of every document you sign.

But you also keep full control of your money. And you learn exactly where every dollar goes.

How to Use a Hard Money Loan the Right Way

Hard money loans are a legitimate tool. The investors who use them well understand a few things:

First, speed is their advantage. Hard money lenders can close in days, not months. In a competitive market like Philadelphia, that speed can be the difference between getting a deal and losing it.

Second, the hard money loan cost has to be built into your numbers before you make an offer. The interest, the origination fee, the carrying costs — all of it needs to be factored into your maximum purchase price calculation. If the deal only works if everything goes perfectly, it doesn’t work.

Third, relationships matter. The best hard money loan terms go to investors with track records. Your first deal will cost more than your fifth. That’s just how it works.

Calculate Your Hard Money Loan Cost Before You Borrow

I built a free Hard Money Loan Calculator so you can see exactly what any loan will cost you before you sign anything.

Enter your loan amount, interest rate, loan term, and origination fee points — and it will show you your monthly interest payment, total interest, origination fee, and the true total cost of the loan.

And once you know your loan cost, run the full deal through the Philly Flip Profit Calculator to see if the numbers still work.

Know the number before you borrow. I learned that the hard way.

Not financial advice — just someone doing a lot of research and asking a lot of questions.