How to Buy Property at Philadelphia Sheriff Sales: What I Wish Someone Had Told Me

The first time I walked into a philadelphia sheriff sale tips session — meaning, a room full of people actually bidding on real properties — I had no idea what I was doing.

I had done my research online. I had read the articles. I thought I understood the process. What I didn’t understand was how fast everything moves, how little time you have to think, and how easy it is to make an expensive mistake when you’re standing in a room full of experienced investors who have done this dozens of times.

Here are the philadelphia sheriff sale tips I wish someone had told me before I walked through that door.

Philadelphia Sheriff Sale Tips: What a Sheriff Sale Actually Is

A sheriff sale is a court-ordered auction of a property. In Philadelphia, properties end up at sheriff sale for one of two main reasons: the owner has defaulted on their mortgage, or the owner has failed to pay property taxes.

The City of Philadelphia holds sheriff sales regularly. Properties are listed in advance, and buyers can research them, inspect the exterior, and run their numbers before the auction date.

The winning bidder at a sheriff sale acquires the property — but not always free and clear. This is the part that trips up most beginners.

Philadelphia Sheriff Sale Tips: The Title Problem

When you buy a property at a Philadelphia sheriff sale, the type of sale matters — a lot. And this is the part most beginners get wrong.

Tax Lien Sales: When a property is sold for delinquent taxes, the sale wipes out most municipal liens — including back taxes and most city-related debts. You’re largely getting a clean slate on those. However, there are two things that can survive: federal tax liens (IRS) and the Right of Redemption — the original owner has 9 months after the deed is recorded to pay the back taxes and reclaim the property. That means you can’t do major renovations or resell for at least 9 months.

Mortgage Foreclosure Sales: When a property is sold because the owner defaulted on their mortgage, lien priority matters. The senior lien (first mortgage) gets paid first from the sale proceeds — and if you’re buying, you may be taking on that senior mortgage. Junior liens below the foreclosing lender are typically wiped out. Always verify which liens are senior and which are junior before you bid.

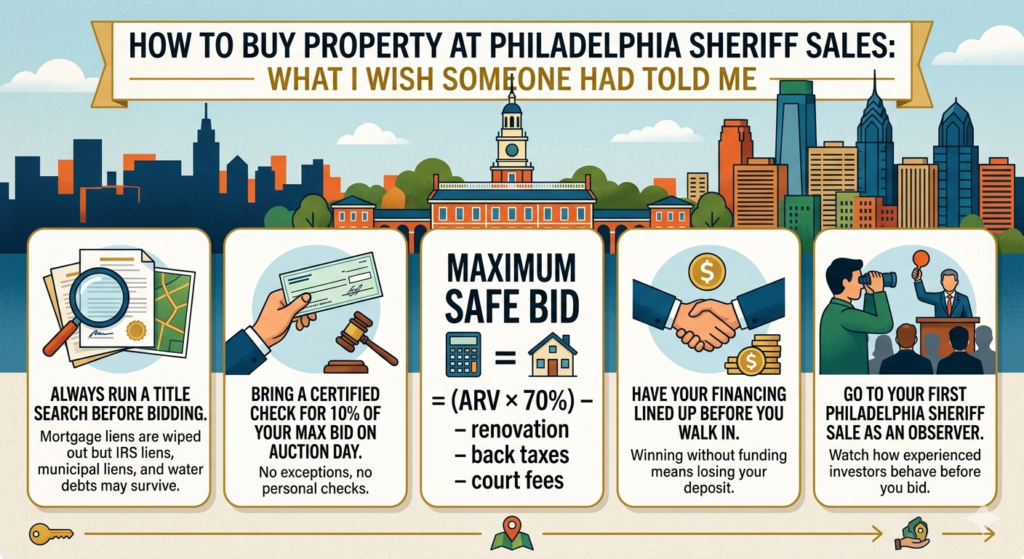

The rule that applies to both: Get a title search before you bid — not after. A title search will show you exactly what survives, what gets wiped, and what you’d be inheriting. Factor every surviving lien into your maximum bid calculation.

Philadelphia Sheriff Sale Tips: Registration and Deposits

To bid at a Philadelphia sheriff sale, you need to register in advance. You’ll need to bring a deposit — typically 10% of your maximum intended bid — in the form of a certified check or money order made out to the Sheriff of Philadelphia County.

If you win and fail to complete the purchase, you lose your deposit. This is not a casual process.

Registration happens before the sale begins. Show up early. Bring your identification. Have your deposit ready.

Philadelphia Sheriff Sale Tips: How the Bidding Works

Sheriff sales in Philadelphia move fast. Properties are called one at a time. The opening bid is typically the amount owed to the plaintiff — the lender or the city — which can be significantly below market value or close to it depending on the situation.

Bidding goes up in increments. Experienced investors know their maximum number before they walk in the room. They don’t get caught up in the energy of the auction. They hit their number and they stop.

This is the discipline that separates investors who make money at Philadelphia sheriff sales from investors who overpay in the heat of the moment.

Philadelphia Sheriff Sale Tips: Calculating Your Maximum Bid

Your maximum bid at a Philadelphia sheriff sale is not the ARV. It’s not even the 70% rule number. It’s lower than that, because you have additional costs that a standard purchase doesn’t have.

Here’s what you need to account for:

Your standard 70% rule calculation — ARV times 70%, minus renovation costs — gives you a starting point. From that number, subtract the back taxes owed on the property, the estimated court and filing fees, and any known liens you’ve identified in your title search.

What’s left is your maximum safe bid.

On a property with an ARV of $220,000 and $45,000 in renovation costs: $220,000 × 70% = $154,000 $154,000 − $45,000 renovation = $109,000 $109,000 − $8,000 back taxes = $101,000 $101,000 − $2,000 court fees = $99,000 maximum bid

If bidding goes above $99,000, you walk away. No exceptions.

Philadelphia Sheriff Sale Tips: What Happens After You Win

If you’re the winning bidder, you’ll pay your deposit immediately and sign the necessary paperwork. You then have a set period — typically 30 days in Philadelphia — to pay the remaining balance in full.

This means you need your financing arranged before you bid, not after. Hard money lenders who work with sheriff sale purchases exist, but you need to have that relationship established in advance. Walking in without financing lined up and winning a bid is a fast way to lose your deposit.

Philadelphia Sheriff Sale Tips: The Properties Worth Looking At

Not every property at a Philadelphia sheriff sale is a good deal. Some are priced at or above market value because of the liens attached. Some are in neighborhoods where the numbers don’t work no matter how low you buy.

The properties worth looking at are the ones where the opening bid is well below your maximum calculated bid, the title search shows manageable liens, and the neighborhood comps support a strong ARV after renovation.

These deals exist. Philadelphia has enough distressed inventory that patient investors find them regularly. But you have to do the work — the title search, the comp analysis, the renovation estimate — before you walk into the room. Start with the Philadelphia Deal Finder to identify neighborhoods where the numbers actually work.

One More Philadelphia Sheriff Sale Tip

Bring cash for the deposit. Bring your calculations on paper. Know your maximum number before you sit down.

And if you’ve never been to a Philadelphia sheriff sale before, go once just to watch. Don’t bid. Just observe how it works, how fast it moves, and how the experienced investors behave.

Then go home, run your numbers, and come back ready.

Not financial advice — just someone doing a lot of research and asking a lot of questions.