Philadelphia hard money lenders are something I wish I’d researched before my first flip — not after.

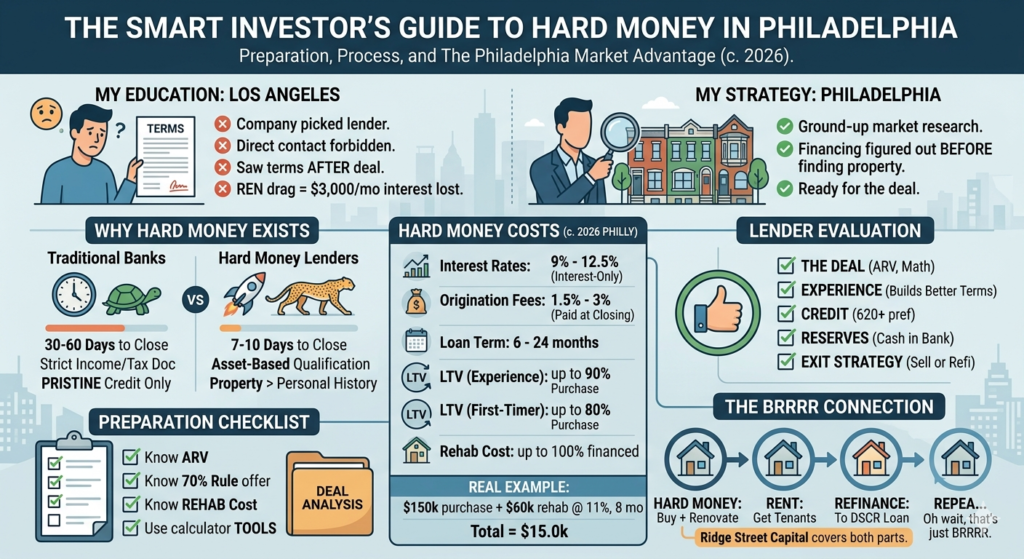

When I did my first flip in Los Angeles, I didn’t pick my hard money lender. The company I invested with picked one for me. I never spoke to the lender directly. I never saw the terms until after the deal was done. I just watched $3,000 a month disappear in interest while the renovation dragged on.

That was my education.

Now I’m in Philadelphia, studying this market from the ground up. One of the first things I did was research Philadelphia hard money lenders — not because I have a deal right now, but because when the deal comes, I need to be ready. The investors who win here are the ones who have their financing figured out before they find the property, not after.

Here’s everything I’ve learned.

Why Philadelphia Hard Money Lenders Exist

Traditional banks are built for stability. They want two years of tax returns, steady employment, pristine credit, and properties already in good condition. They take 30 to 60 days to close.

Philadelphia fix-and-flip deals don’t wait 60 days. Good distressed properties get multiple offers within days. By the time a bank approves your loan, the deal is gone.

Philadelphia hard money lenders exist to solve this problem. They’re private lenders — individuals or firms — who lend based primarily on the value of the property, not your personal financial history. They can close in 7 to 10 days. Sometimes faster.

The tradeoff is cost. Hard money loans are expensive. But for the right deal, the cost is worth it.

What Philadelphia Hard Money Lenders Actually Charge in 2026

Philadelphia’s hard money market is more competitive than most people realize. Because Pennsylvania has a relatively lender-friendly legal framework, rates here tend to run a bit lower than in markets like New York.

Here’s what to expect:

- Interest rates: 9% to 12.5% annually, interest-only payments

- Origination fees: 1.5% to 3% of the loan amount, paid at closing

- Loan term: 6 to 24 months

- LTV: Up to 80–90% of purchase price for experienced investors, 75–80% for first-timers

- Rehab costs: Many lenders will finance 100% of renovation costs on top of the purchase loan

On a $150,000 purchase with a $60,000 rehab budget at 11% interest for 8 months:

- Monthly interest: ~$1,375

- Total interest over 8 months: $11,000

- Origination fee (2%): $3,000

- Total loan cost: ~$14,000

That $14,000 needs to be built into your deal analysis before you make an offer — not discovered after. Run it through the Hard Money Loan Calculator first.

Philadelphia Hard Money Lenders Worth Knowing

Ridge Street Capital Philadelphia-focused lender specializing in fix-and-flip and DSCR loans. First-time investors: up to 80% purchase + 100% rehab. Experienced investors: up to 90% purchase + 100% rehab. Fix and flip rates from 10.5% to 11.25%, origination 1.5% to 2.99%. Also offers DSCR loans from 6.75% to 7.99% for BRRRR refinances. Closes in as little as 7 days.

Direct Mortgage Loan Company Philadelphia-based since 1956. Funds acquisition, rehab, and new construction across Philadelphia, Southeastern Pennsylvania, and New Jersey. Over $250 million in loans funded in the last five years.

Legacy Capital Pennsylvania-based with a strong Philadelphia presence. Known for working with investors at all experience levels, including first-timers.

Alpha Funding Corp Can close in as fast as 3 days for pre-approved borrowers. Rates from 9% to 12.5%. Strong coverage of Philadelphia metro and surrounding markets.

Malve Capital No income docs required. Soft credit pull only. Same-day terms. Works with both new and experienced investors nationwide including Philadelphia.

What Philadelphia Hard Money Lenders Actually Look At

Since they’re not focused on your personal income, here’s what matters:

- The deal — ARV, purchase price, renovation budget, and the math between them

- Your experience — First-time investors get slightly less favorable terms

- Credit score — Most want 620 or above, though some go lower with stronger deal metrics

- Reserves — Having nothing in the bank after closing raises flags

- Exit strategy — Selling the property? Refinancing into a DSCR loan? They want to understand your plan

The BRRRR Connection

One of the most powerful combinations in Philadelphia right now is hard money into DSCR refinance — the BRRRR strategy.

You use a hard money loan to buy and renovate a distressed property. Once it’s renovated and rented, you refinance out of the hard money loan into a long-term DSCR loan based on the new appraised value. If your numbers worked on the buy side, the refinance covers your costs and leaves you holding a cash-flowing rental with a manageable long-term rate.

Ridge Street Capital specifically offers both products, making them worth a conversation if BRRRR is your strategy.

Before You Call Philadelphia Hard Money Lenders

Know your numbers before you pick up the phone. A lender wants to hear: here’s the property, here’s what I’m paying, here’s the ARV, here’s the rehab budget, here’s my exit.

If you can walk through that clearly, you’re taken seriously. If you can’t, you’re not.

The deals are here in Philadelphia. The financing exists. The gap between where most investors are and where they want to be is usually preparation, not opportunity.

Not financial advice — just someone doing a lot of research and asking a lot of questions.