Construction to perm loan — when I first heard this, my reaction was the same as most people’s: sounds too good to be true. No $100K down payment? No GC license? One closing and done?

Turns out it’s real. I’ve flipped three houses, but the financing side of real estate is something I’m still actively learning. And once you understand how the construction to perm loan actually works, the math starts to make a lot of sense — especially if your goal is to eventually stop paying rent and start building something.

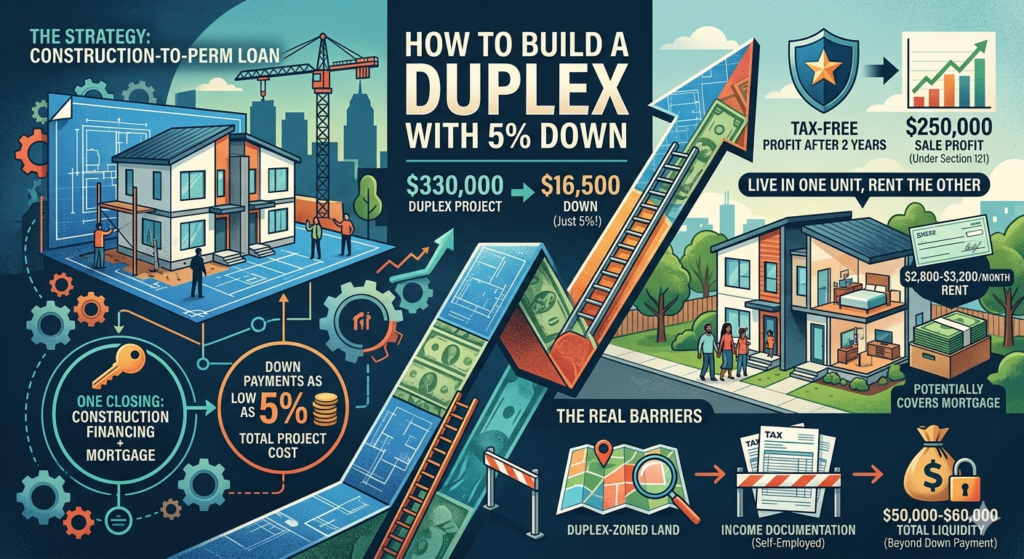

What Is a Construction to Perm Loan?

Most people who want to build from scratch run into the same two-step problem. First you need a construction loan to fund the build. Then, once the house is done, you refinance into a regular mortgage. Two separate applications, two sets of closing costs, two rounds of underwriting. Expensive and slow.

A construction to perm loan collapses that into one transaction. You apply once. During construction, the loan funds the build in draws as work is completed. When the house is finished and you move in, the loan automatically converts to a 30-year mortgage. No refinance. No second application. No additional closing costs.

That single-close structure is what makes the numbers work at 5% down.

The 5% Down Piece

With a construction to perm loan structured as a primary residence purchase, some lenders will go as low as 5% down — calculated on the total project cost, meaning land plus construction combined.

So if you’re looking at a duplex project in the Philadelphia suburbs with a total cost of $330,000 — land, construction, permits, everything — your down payment is:

$330,000 × 5% = $16,500

That’s a real number. Not zero, but not $100,000 either.

The No GC License Part

You don’t need to be a licensed general contractor to build a house. What you need is to hire one.

With a construction to perm loan, you hire a licensed GC through a Cost-Plus Contract — meaning they charge you their actual costs plus a management fee. You’re the owner. They’re running the build. The lender releases funds in draws as construction milestones are hit.

You don’t need a license. You need to find a good builder and understand enough about the process to manage the relationship — which is a learnable skill, not a credential.

Why a Duplex Specifically

This is where the construction to perm loan strategy gets genuinely interesting.

You build a duplex. You live in one unit — which satisfies the owner-occupancy requirement for the loan. You rent out the other unit.

In the Philadelphia suburbs — Cheltenham, Abington, Springfield — a new construction duplex unit rents for significantly more than people assume. A well-built two or three bedroom unit in a good suburban school district can realistically pull $2,800 to $3,200 a month for brand new construction.

On a $330,000 total project, your 30-year mortgage at current rates is roughly $2,100 to $2,300 a month. If the unit next door is renting for $3,000, you’re cash flow positive while living for free.

That’s house hacking at its most functional.

The Tax Bonus Nobody Talks About

If you live in one unit of the duplex as your primary residence for at least two years, you qualify for the Section 121 exclusion when you sell. That means up to $250,000 in profit is completely tax-free if you’re filing as a single. Up to $500,000 if married filing jointly.

Build a duplex with a construction to perm loan, live in it for two years while collecting rent from the other unit, sell it, and potentially walk away with a six-figure tax-free gain.

That’s not a loophole. That’s the tax code working exactly as intended for owner-occupants. According to IRS.gov, the Section 121 exclusion applies to primary residences where the owner has lived for at least two of the last five years — making the duplex house hack one of the most tax-efficient real estate strategies available.

The Real Barriers to a Construction to Perm Loan

Zoning. You need a lot zoned for duplex construction in the right location. That’s not always easy to find and takes time.

Income documentation. Construction to perm lenders want to see qualifying income. If your tax returns show lower income than your actual financial picture — common among self-employed people and business owners — you may not qualify even if the cash flow math works perfectly.

Cash buffer beyond the down payment. The 5% down gets you in the door, but you need reserves for permits, design fees, unexpected construction costs, and carrying costs during the build. Realistically, $50,000–$60,000 in total liquidity puts you in a much more comfortable position than $16,500 alone.

My Own Roadmap

The construction to perm loan strategy makes complete sense to me. The numbers work. The house hacking angle is exactly aligned with where I want to go — building toward multifamily development over time, starting with something manageable and owner-occupied.

But right now, income documentation is a challenge — something a lot of self-employed people and entrepreneurs deal with. My roadmap: get back into flipping, generate documented income and profit history, build the financial paper trail that lenders want to see, and then revisit this strategy when the documentation actually supports the application.

The goal hasn’t changed. The sequencing has to be right.

If you’re in a cleaner income documentation situation — W-2 income, strong tax returns, or a business with clear provable revenue — the construction to perm loan is worth a serious conversation with a lender who specializes in this product.

Use the House Build Cost Calculator to model your full duplex project budget before you approach any lender — land, construction, permits, and all-in costs.

Not financial advice — just someone doing a lot of research and asking a lot of questions.