Loan recasting mortgage strategy is one of those concepts that exists quietly in the background while everyone’s debating 20% down payments and interest rates. I had never heard of it until recently — and once I understood what it was, I couldn’t believe it wasn’t talked about more.

Let me break it down, including the parts some people get wrong.

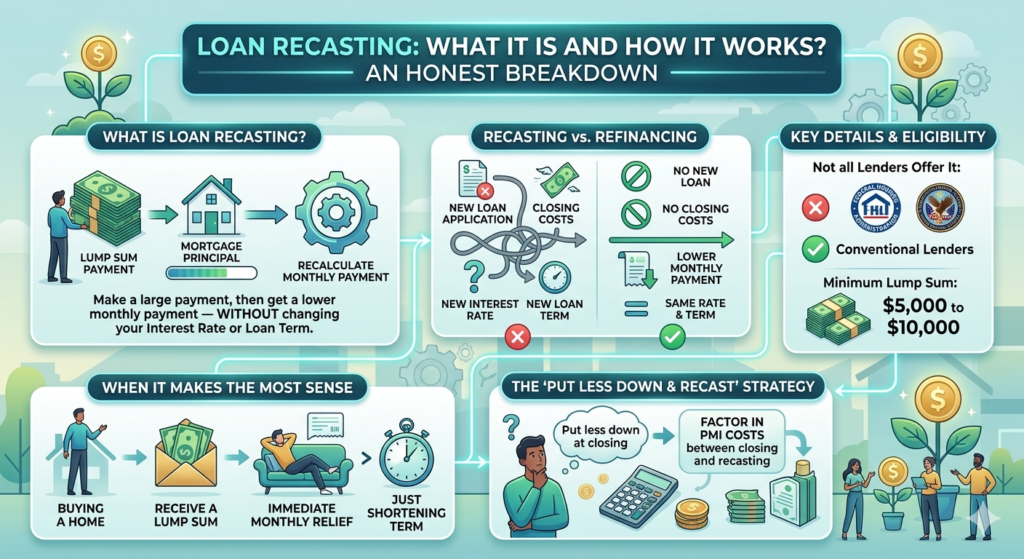

What Is Loan Recasting?

Loan recasting — also called mortgage recasting — is when you make a large lump sum payment toward your mortgage principal, and then ask your lender to recalculate your monthly payment based on the new, lower balance.

Your interest rate stays the same. Your loan term stays the same. The only thing that changes is your monthly payment — it goes down because the principal is smaller.

That’s it. Simple concept, surprisingly underused.

How Loan Recasting Works Step by Step

Let’s say you bought a home for $400,000 with 10% down ($40,000). Your loan is $360,000 at 7% for 30 years. Monthly payment: around $2,395.

A year later, you come into $50,000 — savings, a bonus, an inheritance. You put that $50,000 directly toward your principal. Now your balance is roughly $307,000.

Without loan recasting: your monthly payment stays at $2,395. The extra payment just shortens your loan term.

With loan recasting: you ask your lender to recalculate. Your new monthly payment drops to around $2,041. Same interest rate, same remaining term — just a lower payment every month going forward.

That’s a difference of $354 a month. Every month. For the life of the loan.

The Strategy Some People Suggest — And Where It Gets Complicated

Here’s a strategy combining loan recasting mortgage timing with your down payment:

- Put down the minimum down payment to get approved

- Right after closing, take the money you would have used for a 20% down payment and dump it into the principal

- Then recast the loan

The idea is that you get a lower monthly payment without locking up all your cash upfront at purchase.

It’s a clever structure. But there are a few things worth being honest about.

The Part That Doesn’t Quite Add Up

The version I heard claimed that putting 20% down actually results in a higher interest rate. That’s where I’d push back.

That’s generally not how it works. In most cases, a higher down payment means a lower LTV, which typically means a lower interest rate — not higher. Lenders see less risk when you have more skin in the game.

If someone’s telling you otherwise, ask them to show you actual loan estimates side by side before you believe it.

The PMI Problem in Loan Recasting Mortgage Strategy

Here’s something that often gets glossed over: PMI.

If you put less than 20% down, most conventional loans require Private Mortgage Insurance. PMI typically runs $100 to $300 a month depending on your loan size and credit score.

The good news: once you’ve made that lump sum payment and your LTV drops below 80%, you can request PMI cancellation. But it’s not automatic — you have to ask, and there’s usually a process including a potential appraisal.

The full math on any loan recasting mortgage strategy needs to include however many months of PMI you’re paying between closing and the recast.

What You Need to Know Before Trying Loan Recasting

Not every lender offers it. Government-backed loans like FHA and VA typically don’t allow loan recasting. Conventional loans usually do, but confirm with your specific lender before assuming it’s available.

There’s usually a minimum lump sum. Most lenders require at least $5,000 to $10,000 to qualify for a recast.

There’s a fee. Usually small — around $150 to $500 — but worth knowing about.

Timing matters. Some lenders require a certain number of payments before you can recast. Ask upfront.

According to the Consumer Financial Protection Bureau, loan recasting is available on most conventional mortgages but must be explicitly requested — lenders are not required to proactively offer it, which is why so many borrowers never know it exists.

Is Loan Recasting Mortgage Strategy Actually Worth It?

Yes — in the right situation.

If you already have a mortgage and you come into a chunk of money, loan recasting is often smarter than just making extra principal payments. You get immediate relief on your monthly payment instead of just shortening the loan term.

If you’re buying a home and trying to use the down payment plus recast strategy, the math can work — but run the real numbers including PMI costs, the recast fee, and what your actual rate would be at different down payment levels. Don’t take anyone’s word for it. Get loan estimates.

The concept is legitimate. The execution just needs to be done with eyes open.

Use the Mortgage Calculator to model your loan recasting mortgage scenario — plug in your current balance, lump sum payment, and see exactly what your new monthly payment would look like before you call your lender.

Not financial advice — just someone doing a lot of research and asking a lot of questions.