OPM real estate investing is the concept behind every “I bought a rental with NO money down!” video you’ve ever seen. And I’ll be honest — my first reaction was the same as most people’s. Yeah, right. The guy with the Lamborghini in the thumbnail is making money selling courses, not from the strategy he’s teaching.

But after digging into this for a while, I realized the concept itself isn’t a scam. The math is real. The structures exist. What’s misleading is how easy these videos make it sound.

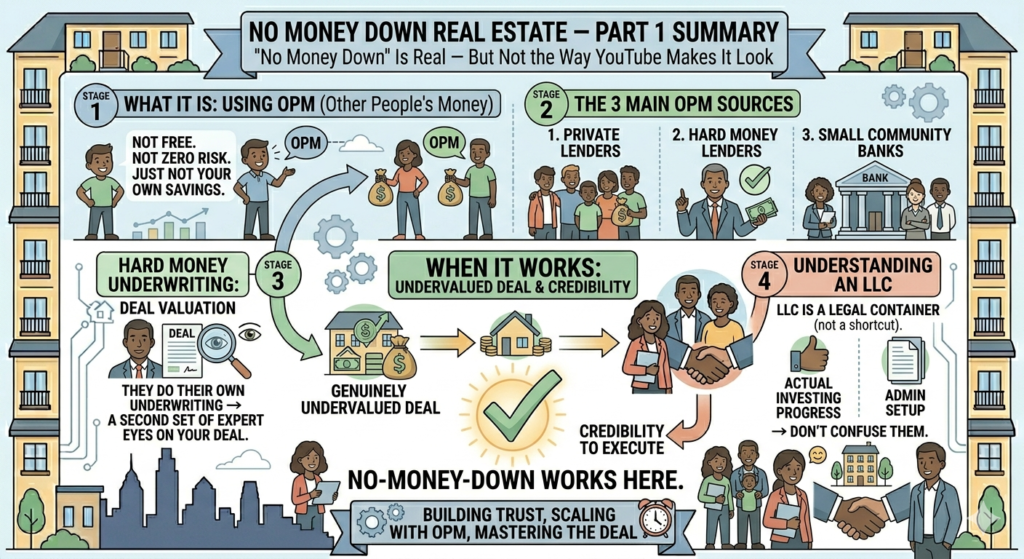

Here’s how OPM real estate actually works.

What “No Money Down” Actually Means in OPM Real Estate

It doesn’t mean free. It doesn’t mean zero risk. It means you’re using other people’s capital instead of your own savings to fund the deal.

In real estate investing circles, this is called OPM — Other People’s Money. And there are three main sources of OPM real estate financing.

OPM Real Estate Source 1: Private Lenders

These are individuals — not banks, not institutions — who have capital sitting around earning minimal returns and are open to lending it for better ones.

Think: a dentist with $200K in a savings account earning 4%. A retired engineer with a self-directed IRA looking for better yield. A real estate agent who’s accumulated capital but doesn’t want to manage properties herself.

These people exist. They’re in your network, or one degree away from it. The OPM real estate pitch isn’t complicated: “I found a deal that will return X%. Would you be interested in lending against it?”

The terms are negotiable — interest rate, repayment timeline, whether they’re in first or second position on the loan. It’s a private agreement between two people.

Is this easy to pull off as a complete beginner with no track record? Honestly, no. Private lenders want to know you know what you’re doing. But it’s a relationship you can start building now, before you need it.

OPM Real Estate Source 2: Hard Money Lenders

Hard money lenders are professional short-term lenders who specialize in real estate investment deals. Higher interest rates than a bank — typically 10–14% — but they move fast and they don’t care about your W-2.

What they care about is the deal. Is the property undervalued? Is there enough equity cushion? Does the math work?

Here’s something I didn’t expect: a good hard money lender is actually doing their own underwriting on your deal. Which means if they say yes, you’ve got a second set of experienced eyes confirming the deal makes sense. That’s worth something when you’re still learning.

Hard money is typically used for the acquisition and rehab phase — not as a long-term hold loan. The OPM real estate plan is always to refinance into conventional or commercial financing once the property is stabilized.

OPM Real Estate Source 3: Small Local and Community Banks

This one surprises people. Big banks — Chase, Wells Fargo, Bank of America — have rigid underwriting boxes. If you don’t fit the box, you don’t get the loan.

Small community banks and credit unions operate differently. They’re portfolio lenders, meaning they hold the loans they make instead of selling them on the secondary market. Which means they have flexibility to evaluate deals on their own terms.

A lot of small local banks actively want to lend to real estate investors. And they’ll often look at the deal itself — the property’s income, the borrower’s experience, the local market — rather than just running your tax returns through an algorithm.

If your reported income is low — which is a lot of us who are self-employed or run businesses — a community bank relationship is worth developing as part of your OPM real estate strategy.

The LLC Question in OPM Real Estate

Almost every “no money down” video leads with: step one, set up an LLC.

There are real benefits — liability protection, tax deductions. But I want to be real about something: an LLC doesn’t get you a loan. It doesn’t find you a deal. It doesn’t make a bad investment good.

It’s a legal structure. Set it up — yes, eventually, and talk to an actual attorney and CPA about how to do it properly. But don’t confuse administrative setup with actual OPM real estate investing progress. I’ve seen people spend three weeks perfecting their LLC paperwork while never looking at a single property.

The LLC is the container. The deal is what goes in it.

So Is OPM Real Estate Actually Possible?

Yes. With conditions.

You need to find a genuinely undervalued deal — not a mediocre property where you’re just hoping it works out. The deal has to be good enough that a private lender or hard money lender looks at it and says yes.

You need some level of credibility — either experience, knowledge, or a strong enough network that someone trusts you to execute.

And you need to understand the exit before you enter. How are you refinancing out of the hard money loan? What does the property need to look like to qualify for conventional financing?

According to BiggerPockets, OPM real estate strategies work consistently for investors who bring deal quality and execution credibility — and almost never for investors who bring neither and are simply hoping other people’s money will compensate for a weak deal.

None of this is impossible. But it’s also not a Tuesday afternoon project for someone who just discovered real estate last month.

Use the No Money Down Calculator to model your OPM real estate deal structure — private lender terms, hard money rates, and projected refinance exit — before you approach any capital source.

Not financial advice — just someone doing a lot of research and asking a lot of questions.