Layered real estate financing is what most “no money down” content never actually explains. Use other people’s money. Find a private lender. Get creative. Cool. But what does that actually look like in practice?

Here are the real mechanics — what to offer a private lender, how to structure the terms, and what to do when a seller wants cash upfront but you don’t have any.

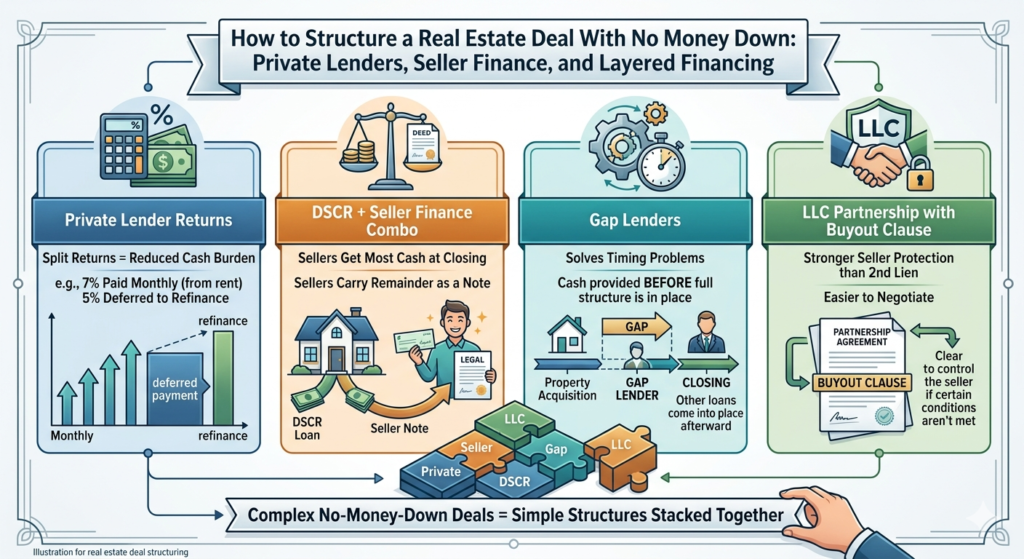

Part 1: Structuring Layered Real Estate Financing With a Private Lender

Private lenders aren’t banks. They don’t have a standard rate sheet. Everything is negotiated — which means you need to know what to offer before you walk into that conversation.

Here’s a structure that actually works, from a real 12-unit deal:

| Purchase price | $682,000 |

| Down payment needed (20%) | $136,000 |

| Rehab budget | $50,000 |

| Total private lender ask | $186,000 |

The return structure offered:

- 12% annual return on $186,000

- 7% paid monthly from rental income (~$1,085/month)

- 5% deferred — paid as a lump sum at refinance

Why split it this way? The monthly 7% keeps your private lender happy and feeling the returns in real time. The deferred 5% reduces your monthly cash burden during the rehab and stabilization phase — when cash flow is tightest. By the time you refinance, the property has appreciated enough that paying out that lump sum is straightforward.

What this costs you: $22,320/year on $186,000 at 12%. But if your value-add work takes the property from $682,000 to $1,100,000 — which happened in this case — you’ve created $418,000 in equity. Paying $22,000/year to access that opportunity is a very good trade.

What private lenders actually want to hear:

- What’s the property worth now, and what will it be worth after improvements?

- What’s the plan to increase NOI?

- What’s the timeline to refinance?

- What’s their security — first or second position?

- What happens if things go sideways?

A private lender isn’t just evaluating the deal. They’re evaluating you. That’s what makes layered real estate financing work — the relationship as much as the numbers.

Part 2: DSCR + Seller Finance — The Core of Layered Real Estate Financing

What about deals where the seller wants a large cash payment upfront and you still don’t have your own money? This is where layered real estate financing gets interesting.

Here’s the structure on a 16-unit deal:

| Purchase price | $1,300,000 |

| DSCR loan | $900,000 |

| Seller carries | $400,000 |

The seller gets $900,000 in cash at closing from the DSCR loan proceeds. The remaining $400,000 stays with the seller as a note — they become a lender on their own property, paid out over time.

Why would a seller agree to this?

Because they get most of their money now. The $900,000 hits their account at closing. The $400,000 becomes a steady income stream with interest — instead of a lump sum they’d just have to reinvest somewhere else. For a seller approaching retirement, that structured payout can actually be more attractive than a full cash sale.

The DSCR piece: Unlike conventional loans, DSCR lenders qualify the loan based on the property’s income — not yours. If the building’s rent covers 1.25x the debt service, you can qualify regardless of your W-2. On a 16-unit building generating solid rents, hitting a 1.25 DSCR on a $900,000 loan is very achievable.

Part 3: The Gap Problem in Layered Real Estate Financing

Here’s a wrinkle that trips up a lot of people on layered deals.

Even when DSCR plus seller finance covers the full purchase price, there’s often a timing gap. The DSCR lender needs to see the seller finance piece in place before they fund. The seller needs to see the DSCR commitment before they agree to carry. Everyone’s waiting on everyone else.

This is where short-term gap lenders or bridge lenders come in. They provide short-term capital — sometimes just for the duration of closing — to plug the gap between what the DSCR loan covers and what needs to hit the table.

It’s expensive. But if the deal only needs the gap capital for 30–60 days, the cost is manageable relative to the deal size. The key: model this cost into your layered real estate financing analysis upfront. Gap lending fees you didn’t account for can eat into returns fast.

Part 4: Protecting the Seller — The Critical Piece of Layered Real Estate Financing

One pushback you’ll get when pitching seller finance deals: “You’re asking my client to be in second position behind a bank. That’s risky.”

They’re not wrong. Three ways to structure around this:

Option 1: Second lien with strong cash flow. The seller stays in second position, but the deal cash flows well enough that default is genuinely unlikely. Show them the NOI, the DSCR, the occupancy history.

Option 2: LLC partnership structure. Instead of a traditional seller finance note, the seller becomes a partner in the LLC that owns the property. The agreement includes a buyout clause — once you pay the seller their $400,000, their partnership interest terminates and you own 100%. If you default on the buyout, control reverts to the seller. They get the property back without a foreclosure process.

Option 3: UCC-1 filing. A business lien filed against the LLC itself rather than the real property. Gives the seller a secured interest in the business entity that owns the property — another layer sophisticated sellers and their attorneys respond well to.

In practice, Option 2 — the LLC partnership with buyout clause — tends to be the most seller-friendly and easiest to explain at the table.

According to BiggerPockets, layered real estate financing structures combining DSCR loans and seller carry-back notes have become increasingly common in commercial multifamily acquisitions — precisely because they solve the capital gap problem without requiring the buyer to have the full purchase price in cash.

Putting Layered Real Estate Financing Together

These aren’t separate strategies. They’re tools you layer depending on what the deal requires.

- Private lender covering the down payment? Structure a split return — monthly interest now, deferred interest at refi.

- Seller wants cash upfront but you don’t have it? DSCR loan covers the bulk, seller carries the rest.

- Timing gap at closing? Short-term gap lending bridges it.

- Seller nervous about second position? LLC partnership with buyout clause gives them real protection.

The deals that look impossible from the outside — large multifamily, no money down, complex financing — are usually just multiple simple structures stacked on top of each other. The skill is knowing which pieces to use and how to combine them for a specific deal.

Use the DSCR Loan Qualifier to check whether the income side of your layered real estate financing deal qualifies before you start approaching lenders or sellers.

Not financial advice — just someone doing a lot of research and asking a lot of questions.