FHA self sufficiency test is the rule most house hackers don’t find out about until they’re already deep into the process — and it stops a lot of deals cold.

If you’ve been researching house hacking with an FHA loan, you’ve probably seen the pitch: 3.5% down, buy a triplex or fourplex, let your tenants cover your mortgage, live almost for free.

For a duplex, it often works exactly like that. For a triplex or fourplex? There’s a hidden rule worth understanding before you fall in love with a property.

What Is the FHA Self Sufficiency Test?

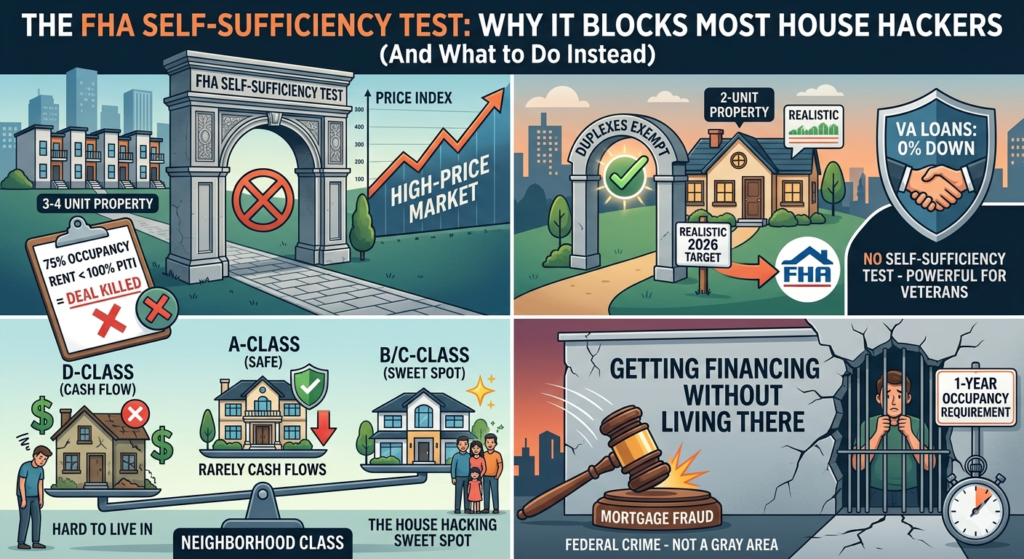

For 3 and 4 unit properties, FHA requires that the projected rental income from all units — including the one you’ll live in — covers at least 100% of the monthly mortgage payment (PITI: principal, interest, taxes, and insurance).

In other words: the building has to pay for itself. Completely.

The FHA self sufficiency test doesn’t apply to duplexes. A 2-unit property just needs to meet standard FHA debt-to-income requirements. But the moment you go to 3 or 4 units, this test kicks in.

Why does this matter right now? Property prices have risen significantly faster than rents in most markets. A fourplex that would have passed this test easily in 2019 might fail it today — not because the rents are bad, but because the purchase price is so much higher.

Example:

You find a fourplex in Philadelphia listed at $550,000. Market rents total $5,200/month. Estimated PITI at current rates: $3,800/month.

The FHA self sufficiency test uses 75% of projected rents to account for vacancy:

$5,200 × 0.75 = $3,900 — covers $3,800. Barely passes.

Same scenario at $600,000:

- PITI: ~$4,200/month

- 75% of rents: $3,900

Fails. Deal dead for FHA purposes — even though the rents are solid and the property cash flows fine on paper.

This is why so many house hackers who want a triplex or fourplex end up settling for a duplex. Not because they wanted to, but because the FHA self sufficiency test math stops working in today’s market.

Your Options When the FHA Self Sufficiency Test Fails

Option 1: Duplex instead of triplex/fourplex

The FHA self sufficiency test doesn’t apply to 2-unit properties. If the fourplex math isn’t working, step back to a duplex. You lose one rental unit but keep the FHA benefits — 3.5% down, lower credit requirements, owner-occupant financing.

In Philadelphia specifically, solid duplexes in B and C neighborhoods can still generate enough rent to cover most or all of your mortgage.

Option 2: VA Loan (if you qualify)

If you have military service, the VA loan is flat-out better for house hacking than FHA in almost every way:

- 0% down payment vs 3.5% FHA

- No FHA self sufficiency test for 3–4 unit properties

- No mortgage insurance premium (FHA charges MIP for the life of the loan)

- Generally competitive interest rates

The VA loan is one of the best wealth-building tools available to veterans and it’s chronically underutilized.

Option 3: Conventional owner-occupant financing

Conventional lenders typically require 15% down on a 2–4 unit property you’ll live in — versus 25% for a pure investment property. There’s no FHA self sufficiency test and no lifetime mortgage insurance.

If your credit is strong (720+) and you have some capital to work with, conventional owner-occupant financing might get you into a triplex or fourplex that FHA would reject.

Neighborhood Class: Where to Actually Live While House Hacking

You have to live there. This changes the calculus compared to pure investment analysis.

D-class neighborhoods: High cash flow potential, high management intensity. As someone who lives in the building — usually not worth it.

A-class neighborhoods: Safe and desirable — but high purchase prices and rents that often don’t cover the mortgage. The house hacking math usually breaks down here.

B and C-class neighborhoods: The sweet spot. Reasonable prices, rents that actually cover most or all of the mortgage. In Philadelphia, parts of Germantown, West Philly, and certain parts of North Philly fall into this range depending on the specific block.

Walk the neighborhood at different times of day before you commit. You’re not just buying an investment — you’re choosing where you’re going to live, potentially for years.

The Mortgage Fraud Warning Nobody Talks About

When you get owner-occupant financing — FHA, VA, or conventional — you are legally required to move into the property as your primary residence, typically within 60 days of closing, for at least one year.

Getting owner-occupant financing with no intention of living there is mortgage fraud. Not a gray area. A federal crime.

What’s legitimate:

- You genuinely move in, live there for a year, then move out and convert to a full rental

- Life circumstances change and you have to move sooner — document everything and consult an attorney

What’s not legitimate:

- Buying with owner-occupant financing when you never planned to live there

- Moving in for 30 days and then leaving

According to HUD.gov, occupancy fraud is one of the most actively investigated forms of mortgage fraud — and FHA lenders are required to report suspicious patterns of owner-occupant financing followed by immediate rental conversion.

What to Check Before You Make an Offer

CapEx items: Roof, HVAC, plumbing, electrical, foundation. Get an inspector who specializes in multifamily. One surprise $15,000 furnace replacement can wipe out a year of cash flow.

Existing tenants: In Pennsylvania, you generally need to give 30–60 days notice if you need a unit vacated for owner occupancy. Factor this into your timeline.

Utility separation: Are utilities separately metered per unit, or does one master meter serve the whole building? Separately metered is much cleaner.

Rental history: Ask for actual rent rolls and leases, not just what the seller claims units “could rent for.” Verify current rents against market comps.

Use the Philadelphia House Hacking Calculator to run your FHA self sufficiency test math before you make any offer — plug in rents, purchase price, and PITI to see if the property passes before you fall in love with it.

Not financial advice — just someone doing a lot of research and asking a lot of questions.