Conventional multifamily loan options just got significantly better. Fannie Mae recently changed one of its rules in a way that’s genuinely significant for anyone thinking about house hacking — and most people haven’t heard about it yet.

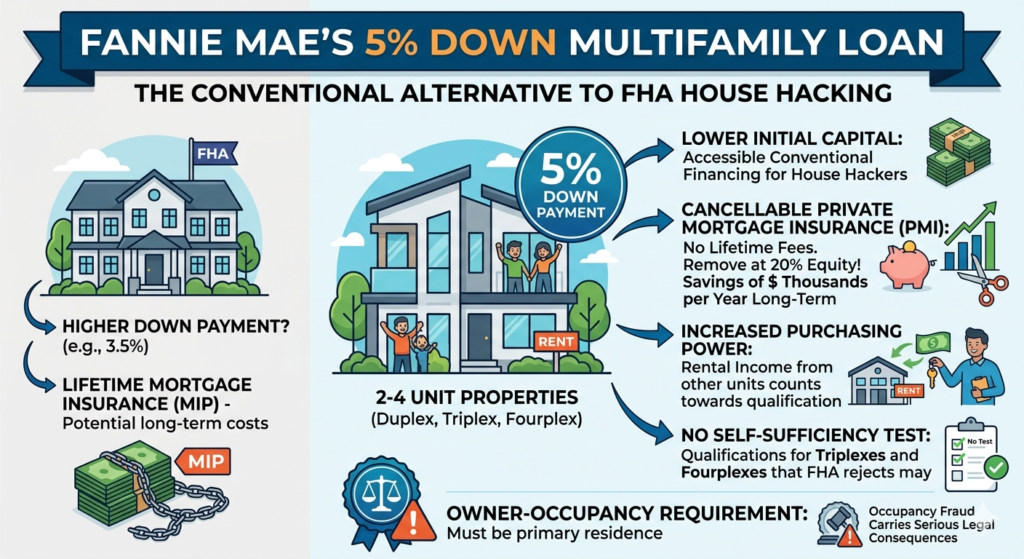

Previously, buying a 2–4 unit property with conventional financing required 15–25% down. Now, if you’re planning to live in one of the units, Fannie Mae allows as little as 5% down on a 2–4 unit property.

That’s a big deal. Here’s exactly why.

Conventional Multifamily Loan vs FHA: What’s the Difference?

You might be thinking — FHA already allows 3.5% down. Why does this matter?

The difference is in the long-term costs and flexibility.

FHA:

- 3.5% down (slightly lower)

- Mortgage Insurance Premium (MIP) for the life of the loan if you put less than 10% down

- Self-sufficiency test for 3–4 unit properties (total rents must cover 100% of PITI)

- More flexible credit requirements (580+ minimum)

Conventional Multifamily Loan at 5% Down:

- 5% down (slightly higher)

- Private Mortgage Insurance (PMI) — but cancellable once you hit 20% equity

- No self-sufficiency test

- Generally requires stronger credit (620+ minimum, better rates at 740+)

The PMI difference is huge over time.

On a $500,000 loan with FHA, you’re paying MIP of roughly $230/month — forever, unless you refinance into a conventional loan. That’s $2,760/year, potentially for 30 years.

With the conventional multifamily loan, once your equity hits 20%, you request PMI cancellation and that cost disappears. Done.

For someone buying in Philadelphia where properties have been appreciating, hitting 20% equity is realistic. At that point the conventional multifamily loan becomes significantly cheaper than FHA long-term.

The Self-Sufficiency Test Problem — Solved by the Conventional Multifamily Loan

FHA has a self-sufficiency test for 3 and 4 unit properties. The projected rents at 75% occupancy have to cover 100% of your mortgage payment. In today’s market, this test kills a lot of triplex and fourplex deals.

Fannie Mae’s conventional multifamily loan at 5% down doesn’t have this requirement.

You still need to qualify based on your income and debt-to-income ratio. And the lender will look at projected rental income — up to 75% of market rents can be counted toward your qualifying income. But there’s no separate self-sufficiency hurdle the property itself has to clear.

This means deals that FHA would reject on a triplex or fourplex might work fine under the conventional multifamily loan guidelines.

The Numbers: What the Conventional Multifamily Loan Looks Like in Philadelphia

Property: Triplex in West Philadelphia Purchase price: $420,000 Down payment (5%): $21,000 Loan amount: $399,000

| Expense | Monthly |

|---|---|

| Principal & interest (7.0%, 30yr) | ~$2,656 |

| Property taxes | ~$350 |

| Insurance | ~$150 |

| PMI (~0.5%/yr on $399K) | ~$166 |

| Total PITI + PMI | ~$3,322 |

| Rental income (2 units × $1,400) | -$2,800 |

| Your effective housing cost | $522/month |

You’re living in a triplex in West Philly for $522/month. Once the property appreciates enough to hit 20% equity — which at 3–4% annual appreciation could happen within 5–7 years — PMI drops off and that number gets even better.

Compare that to renting a one-bedroom in the same neighborhood for $1,400+/month. The math speaks for itself.

What You Actually Need to Qualify for the Conventional Multifamily Loan

Credit score: Minimum 620, but realistically 700+ for decent rates. At 740+ you get the best pricing.

Debt-to-income ratio: Generally 45% or below, including your new mortgage payment plus all existing monthly debt obligations.

Reserves: Fannie Mae typically wants 2–6 months of mortgage payments in reserves after closing. You’re putting less down, but you still need cash reserves sitting in the bank.

Owner occupancy: You must move into one of the units as your primary residence. This is not an investor product — it’s for people who will actually live there.

Property condition: The property needs to meet Fannie Mae’s standards — no major deferred maintenance issues affecting habitability.

The Rental Income Advantage of the Conventional Multifamily Loan

One of the most underappreciated aspects of buying a multifamily property is how rental income affects your purchasing power.

With a single-family home, the bank qualifies you on your personal income alone. With the conventional multifamily loan on a 2–4 unit property, lenders can count 75% of projected rental income from the other units toward your qualifying income.

Example:

- Your personal income qualifies you for a $280,000 single-family loan

- You’re buying a triplex where two units rent for $1,400/month each

- 75% of $2,800/month = $2,100/month added to qualifying income

- That could increase your qualifying loan amount by $150,000–$200,000+

Same person. Same job. Dramatically different purchasing power — just because the property generates income.

According to BiggerPockets, Fannie Mae’s 5% down conventional multifamily loan program has opened up house hacking to a significantly broader pool of buyers — particularly those who were blocked by FHA’s self-sufficiency test on triplex and fourplex properties.

Who the Conventional Multifamily Loan Is Best For

Good fit:

- Someone with decent credit (700+) who wants to house hack

- Anyone frustrated by FHA’s self-sufficiency test on triplexes and fourplexes

- People who want the long-term savings of cancellable PMI vs lifetime FHA MIP

- First-time buyers with some savings but not enough for 15–25% down

Less ideal:

- Credit below 620 — FHA is more accessible at lower credit scores

- Someone who truly can’t afford more than 3.5% down — FHA’s slightly lower threshold might be necessary

- Veterans — VA loan is still better than both (0% down, no PMI, no self-sufficiency test)

Use the Philadelphia House Hacking Calculator to run both FHA and conventional multifamily loan scenarios on your target property — side by side — before you commit to either path.

Not financial advice — just someone doing a lot of research and asking a lot of questions.