When I first started looking into Philadelphia Sheriff Sales, I thought it was just one thing — like, the city takes a house and sells it. Simple, right?

Nope.

Turns out there are two completely different types of foreclosure sales happening in Philadelphia, and if you mix them up, you’re going to be very confused very fast. I know because I spent an embarrassing amount of time confused before it finally clicked.

So let me break it down the way I wish someone had explained it to me.

What Is a Philadelphia Sheriff Sale, Actually?

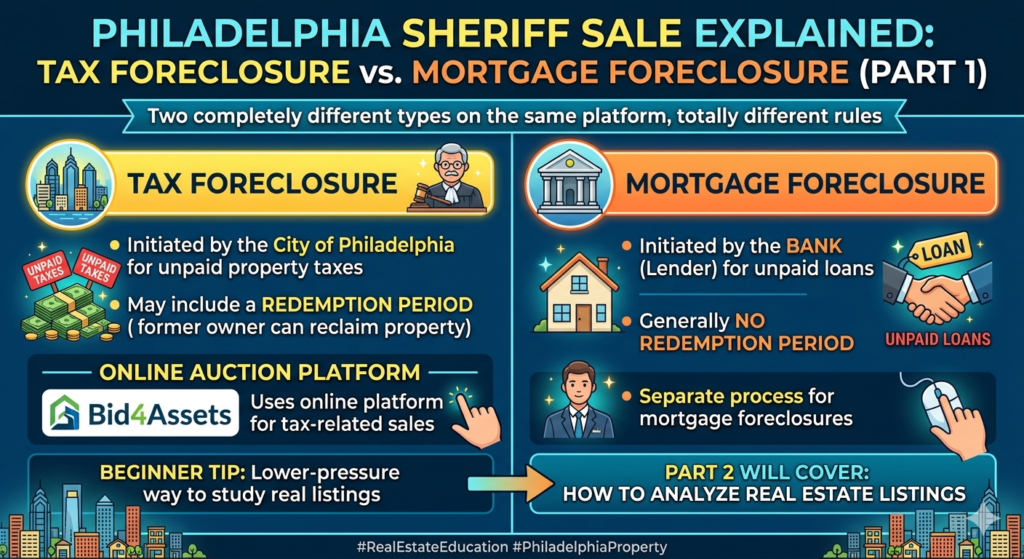

A Sheriff Sale is when a property gets sold by the court — specifically, through the Philadelphia Sheriff’s Office — because the owner couldn’t pay something. That “something” is what splits into two very different scenarios.

Scenario A: The owner didn’t pay their property taxes. Scenario B: The owner didn’t pay their mortgage.

Same auction platform, totally different rules. And the differences matter a lot if you’re thinking about buying.

Tax Foreclosure vs. Mortgage Foreclosure: The Basic Difference

Here’s the simplest way I can explain it:

Tax Foreclosure = The city is coming after you because you owe back taxes. Mortgage Foreclosure = The bank is coming after you because you stopped paying your loan.

Both can end up at the Sheriff Sale. But what happens after you buy is where it gets interesting.

Philadelphia Tax Sale: What You Need to Know

In Philadelphia, if a property owner hasn’t paid their property taxes, the city can eventually move to sell that property to recover what they’re owed.

These properties show up on Bid4Assets — that’s the online platform Philadelphia uses for its tax lien and tax deed auctions. You can browse listings, set up alerts, and bid from your couch. (Which sounds amazing until you realize you need to actually analyze what you’re bidding on, but more on that in Part 2.)

The big thing with tax foreclosures: Redemption Period.

In Pennsylvania, a former owner can sometimes come back after the sale and reclaim their property — as long as they pay off what was owed plus costs. This is called the redemption period, and it can be nerve-wracking if you don’t know it’s a thing.

The length of the redemption period can vary depending on the type of tax sale, so always verify the specific terms for each auction. Don’t assume.

The practical takeaway: with tax foreclosures, you might win the bid and still not have a fully clear path to the property right away. That’s not a reason to avoid it — it’s just something to factor into your timeline and budget.

Mortgage Foreclosure: A Completely Different Beast

When someone stops paying their mortgage, the bank is the one initiating the foreclosure process, not the city. After going through the courts, the property can end up at the Sheriff Sale too.

Here’s the key difference: mortgage foreclosures generally don’t have a redemption period in Pennsylvania.

Once the sale is confirmed by the court, the previous owner typically cannot come back and reclaim the property. The title transfer is more final.

Why? Because the legal framework is different. Tax sales are about recovering public funds — the government builds in some protections for homeowners. Mortgage foreclosures are a private contract dispute — once the court rules, it’s done.

This doesn’t mean mortgage foreclosures are automatically “better” deals. They come with their own complications (more on that soon). But knowing that there’s no redemption period can make the post-purchase timeline cleaner.

Sheriff Sale vs. Bid4Assets: What’s the Difference?

This is another thing that tripped me up early on.

Philadelphia Sheriff Sale = The actual legal process, run through the Sheriff’s Office. This is where mortgage foreclosure properties typically land. Sales used to happen in person; the format has shifted over time.

Bid4Assets = An online auction platform that Philadelphia uses for certain tax-related sales. More accessible, more listings visible upfront, you can browse without showing up anywhere.

Think of Bid4Assets as a window into one category of distressed properties. The Sheriff Sale process is a separate pipeline with different rules.

Both are worth watching. But they’re not interchangeable.

So Which One Should You Focus On?

Honest answer: it depends on what you’re trying to do and how much risk you can tolerate.

If you’re just starting to learn — like me — Bid4Assets is a good place to get your eyes on real properties without immediately putting money on the line. You can study listings, look up OPA records, check zoning, and start building your analysis muscle without being in a high-pressure auction room.

Mortgage foreclosure properties at Sheriff Sale can have better title clarity post-purchase, but they often require more upfront research and sometimes have more competition from experienced buyers.

I’m still in research mode. But I’ve been spending a lot of time on Bid4Assets lately, pulling up real listings and working through what the data actually tells you — ownership structure, zoning, assessed value vs. what people are actually bidding.

If you want to see how I broke down 151 real Philadelphia tax sale listings, that post is here.

That’s what Part 2 is going to be about.

Coming Up in Part 2

In the next post, I’m going to walk through how I actually analyze a Bid4Assets listing — including:

- How to read an OPA record (and what the numbers actually mean)

- What to look for when a property is owned by an LLC

- RSA-5 zoning: what it allows and why it matters

- Why “Pending” status shows up so much and what it actually means

- Homestead Exemption: what it tells you about who was living there

If you’ve been curious about Philadelphia tax sales but felt overwhelmed by the data — same. Let’s figure it out together.