No Money Down Real Estate: What Actually Works, Part 3

Okay. We’ve covered the money side. We’ve covered the deal side. Now let’s talk about what it actually looks like when you put it all together.

This is the part where theory becomes a transaction.

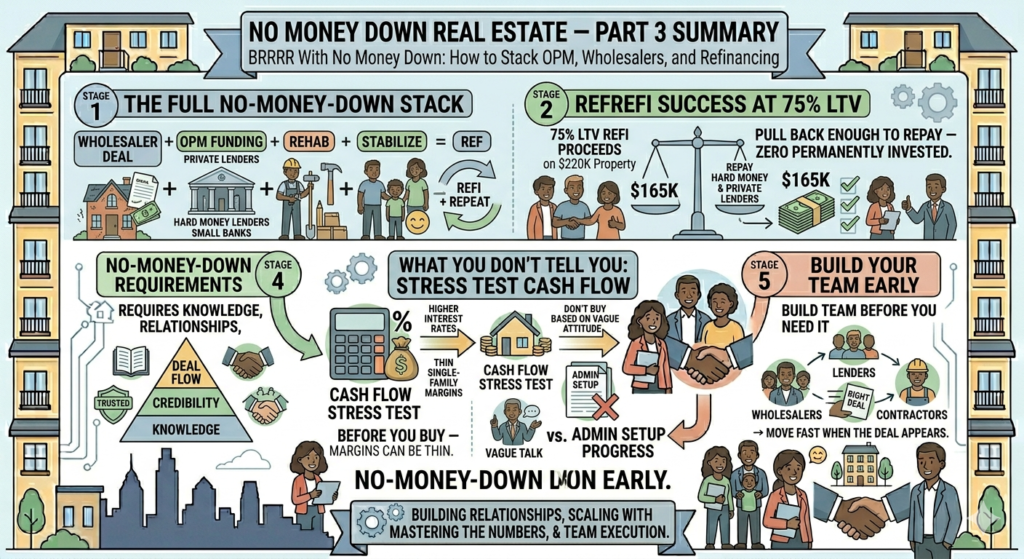

The Full Stack: What You’re Actually Building

Here’s the framework, end to end:

- Build your team first — hard money lender, private lender, wholesaler relationships, contractor, title company

- Get a deal from your wholesaler network that meets your criteria

- Fund it with OPM — hard money for acquisition and rehab

- Rehab and stabilize — get it rented, NOI optimized

- Refinance into long-term financing, pull capital back out

- Repeat with the same capital recycled into the next deal

None of your own money permanently tied up. The tenants pay the mortgage. The asset appreciates. You move on to the next one.

That’s the loop. Simple in concept. Let’s walk through it with real numbers.

A Real-ish Example: Philadelphia Row House

Let’s say a wholesaler sends you a 3-bedroom row house in West Philadelphia. Here’s what the numbers look like:

The Deal:

- ARV (After Repair Value): $220,000

- Wholesaler asking price: $105,000

- Estimated repairs: $45,000

- Total cost basis: $150,000

- Equity at ARV: $70,000

The 70% Rule Check: Hard money lenders typically want all-in costs at or below 70% of ARV:

$220,000 × 0.70 = $154,000 max Your all-in: $150,000 ✓ — deal passes

Funding with Hard Money:

- Hard money lender covers 90% of purchase + 100% of rehab (common structure)

- Your out of pocket: roughly $10,500 (10% of purchase)

- Or — a private lender covers that 10% gap

- Your out of pocket: $0

The Rehab Phase

This is where a lot of no-money-down deals fall apart — not because the financing didn’t work, but because the rehab went sideways.

Hard money lenders typically release rehab funds in draws — you complete a phase of work, they inspect, they release the next chunk. Which means your contractor needs to be able to front costs temporarily, or you need a small working capital cushion.

This is also why your contractor relationship matters as much as your lender relationship. A contractor who disappears mid-project, or who wildly underestimates costs, can blow up a deal that looked perfect on paper.

Vet your contractors before you need them. Get multiple bids. Check references. And build a 10–15% contingency into every rehab budget — because something always comes up.

Stabilization: Getting It Rent-Ready

Once rehab is done, you need a tenant — fast. Every month the property sits vacant is a month you’re paying hard money interest with no income coming in.

For a single-family in West Philadelphia, you’re looking at market rents somewhere in the $1,400–$1,800 range depending on condition and exact location. Price it right, screen tenants properly, and get it occupied.

Once it’s rented and stable, you’re ready for the refinance.

The Refinance: Getting Your Money Back Out

Now you go to a conventional lender or portfolio lender with a stabilized, rented property appraised at $220,000.

Most lenders will do a cash-out refinance at 75–80% LTV on an investment property:

$220,000 × 0.75 = $165,000 loan

Your hard money loan balance: ~$150,000

Cash out: $165,000 − $150,000 = $15,000 back in your pocket

Plus you’ve repaid the private lender who covered your down payment gap.

Net result: you own a rented property in West Philadelphia. You have a conventional 30-year loan at a manageable rate. Your tenants are covering the mortgage. And you’ve recycled your capital — or in a true no-money-down structure, you’ve returned borrowed capital — and you’re ready for the next deal.

The Part Nobody Talks About: Does It Actually Cash Flow?

Let’s stress test this honestly.

Monthly income: $1,600 rent

Monthly expenses:

- Mortgage (30yr, 7.5%, $165K): ~$1,154

- Taxes + Insurance: ~$350

- Property management (10%): ~$160

- Maintenance reserve (5%): ~$80

- Vacancy reserve (5%): ~$80

Total expenses: ~$1,824

Monthly cash flow: -$224

Negative. Slightly.

And this is the part where I have to be straight with you — because too many YouTube videos skip right past this.

At today’s interest rates, a lot of BRRRR deals in expensive markets don’t cash flow strongly after refinance. The strategy still builds equity. It still gets your capital back. But the monthly cash flow might be thin or even slightly negative depending on the numbers.

This doesn’t make the strategy wrong. It means you have to know going in what you’re optimizing for — equity building, capital recycling, cash flow, or some combination. And you have to run the post-refi numbers before you buy, not after.

If cash flow is your primary goal right now, you might need to find a deal with more margin — lower purchase price, lower rehab, higher rents. Or look at small multifamily where the rent-to-price ratios are better.

What “No Money Down” Actually Requires

Let me be real about what this whole strategy actually demands — because it’s not nothing:

Knowledge — You need to understand ARV, rehab estimating, cap rates, loan structures, and refinance math before you do your first deal. Not after.

Relationships — Hard money lender, private lender, wholesaler, contractor, title company, property manager. You’re building a team, not just buying a house.

Credibility — Private lenders especially want to know you know what you’re doing. Your first deal is the hardest because you don’t have a track record yet. That’s why some people partner with an experienced investor on deal one — to learn and to borrow credibility.

Deal flow — One good wholesaler relationship isn’t enough. You might look at 20 deals before one actually meets your criteria. That’s normal. That’s the business.

Execution — The strategy works on paper. Making it work in real life means managing contractors, lenders, tenants, timelines, and unexpected problems simultaneously.

None of this is impossible. People do it regularly. But it’s a skill set you build — not a hack you stumble into because a YouTube video made it sound easy.

Where to Start If You’re Not Ready to Pull the Trigger Yet

Honestly? Start building the team before you need it.

- Call two or three hard money lenders in Philadelphia. Ask them their criteria. Find out what deals they’ll fund.

- Show up to one REI meetup. Introduce yourself to a wholesaler.

- Run the numbers on five deals you’ll never buy — just to practice the math.

- Open a relationship with a community bank and have a conversation about investment property lending.

By the time the right deal shows up, you want all of that already in place. The investors who move fast on good deals are the ones who built their infrastructure before they needed it.

That’s where I am right now. Studying the framework, building the relationships, waiting for the deal that actually pencils out.

When it does — I’ll write about it.

Not financial advice — just someone doing a lot of research and asking a lot of questions.