I came across a video recently that kind of broke my brain a little — in the best way.

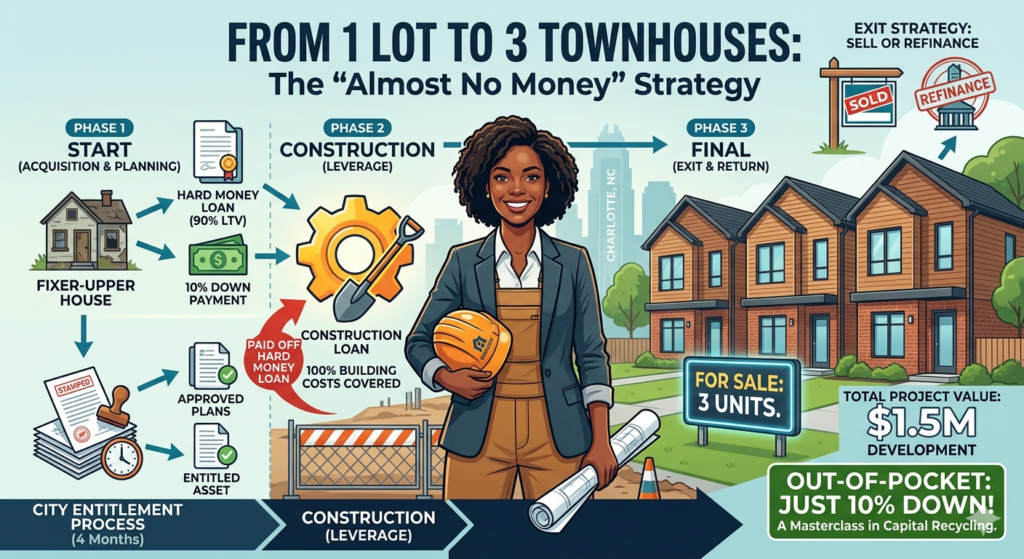

A woman in Charlotte, NC built three townhouses — a $1.5 million development — and the only money she put in out of pocket was a 10% down payment on the original land purchase. That’s it. No massive bank account. No rich uncle. Just a really smart sequencing of financing using a hard money construction loan strategy.

Here’s exactly how she did it, and why I think it’s worth understanding if you’re anywhere near the Philadelphia market.

She Started with a Flip — Then Changed Her Mind

The original plan was simple: buy a distressed property in Charlotte, fix it up, sell it, make around $40K. Normal flip strategy.

To buy the property, she used a hard money lender — which covered 90% of the purchase price. So she only needed 10% of her own money to get in the door.

But once she owned it, she started looking at the land differently. The lot had more potential than a single flip. Instead of just renovating the existing structure, she decided to tear it down and build three townhouses.

That pivot changed everything — and it started with a hard money construction loan sequence that most investors never think to use.

The Entitlement Process: The Part Nobody Talks About

Before she could break ground, she had to get the city of Charlotte to approve her development plans — zoning approvals, architectural plans, permits. This is called the entitlement process.

It took about four months.

This is the part most beginner investors skip over when they imagine becoming a developer. It’s not just building stuff — there’s a whole bureaucratic process before a single nail goes in. In Philadelphia, this process exists too, and it can take longer depending on the neighborhood and what you’re trying to do.

But here’s the thing: once she had those approvals in hand, she had something valuable. An entitled piece of land with approved plans is worth significantly more than raw land. That’s leverage — and it’s what made the next step possible.

The Hard Money Construction Loan: Where the Magic Happened

With city approval secured, she went to a construction lender.

Construction loans work differently from regular mortgages. They’re designed to fund the building process — lenders release funds in stages called draws as construction milestones are hit, not all at once upfront.

Here’s the key part of her hard money construction loan strategy: the construction loan covered 100% of the building costs. And with that loan, she also paid off the original hard money loan she used to buy the property.

So at this point:

- Hard money loan: paid off ✅

- Construction fully funded ✅

- Her own cash still in the deal: just that original 10% down payment

She essentially recycled her capital through the deal structure. That’s what makes this strategy so powerful — you’re not stacking more of your own money into the deal at each stage.

Breaking Down the Hard Money Construction Loan Strategy Step by Step

| Step | What She Did | Financing Used |

|---|---|---|

| Buy the property | Purchased distressed lot | Hard money loan (90% LTV) |

| Pivot the plan | Decided to develop instead of flip | No new money needed |

| Get approved | Entitlement process | Time, not money |

| Secure construction loan | Got 100% construction financing | Construction lender |

| Pay off hard money | Used construction loan proceeds | Recycled capital |

| Build 3 townhouses | Full development | Construction loan draws |

Total out of pocket: roughly 10% of the original purchase price on a $1.5 million project.

According to BiggerPockets, the hard money to construction loan bridge is one of the most underutilized sequences in small-scale real estate development — precisely because most investors don’t realize construction lenders will pay off the acquisition loan as part of the deal.

Could This Hard Money Construction Loan Strategy Work in Philadelphia?

Honestly? Yes — and Philadelphia might actually be a better market for this than Charlotte right now.

Philly has tons of underutilized lots, aging rowhouses on large footprints, and neighborhoods where new construction is starting to pencil out. Germantown, Brewerytown, parts of North Philly — there are parcels sitting there that aren’t being used to their full potential.

The entitlement process in Philadelphia runs through the Department of Licenses and Inspections (L&I), and yes, it can be slow. Zoning variances, civic design reviews, neighborhood meetings — it adds time. But that time is also a barrier to entry that keeps competition lower than in markets like Austin or Charlotte.

The financing stack she used — hard money to acquire, construction loan to build — is available in Philadelphia. Hard money lenders operate actively here. Construction lenders exist. The question is whether the numbers work on a specific deal.

That’s where the math has to be done carefully before you commit. Use the Hard Money Loan Calculator to model your acquisition costs and carrying costs before you decide whether a development play makes sense on a specific property.

What I’m Taking Away from This

I’ve been focused on fix-and-flip as the entry point into real estate — and that’s still valid. But this hard money construction loan strategy made me think differently about what the exit can look like.

You don’t have to flip. Sometimes the land is worth more as a development play. The key is recognizing that moment — like she did — when you’re already in a deal and the opportunity is bigger than what you originally planned for.

It requires more patience, more coordination with lenders, and more risk tolerance. But the upside is a completely different scale.

I’m not saying I’m doing this tomorrow. I’m saying I’m paying attention.

Not financial advice — just someone doing a lot of research and asking a lot of questions.