How Much Equity Do You Actually Have In Your Home?

Most homeowners know they have equity in their home. What most of them do not know is exactly how much — or what they can actually do with it.

I did not fully understand home equity until I started studying real estate investing seriously. And once I understood it, I realized it is one of the most powerful financial tools available to homeowners who know how to use it.

Here is what you actually need to know.

What Home Equity Is

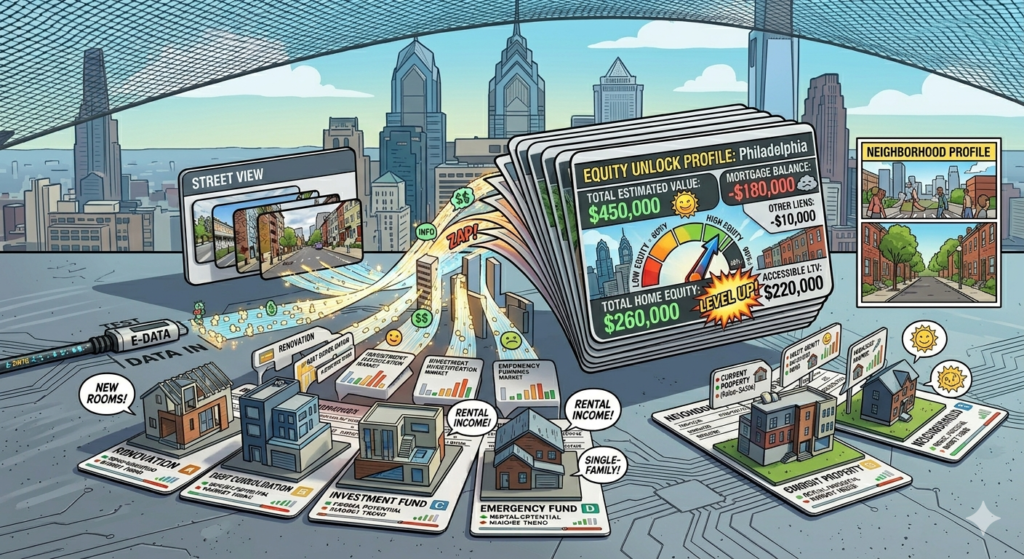

Home equity is simple. It is the difference between what your home is worth right now and what you still owe on your mortgage.

If your home is worth $300,000 and you owe $180,000 on your mortgage, you have $120,000 in equity.

That $120,000 is yours. It sits in your home like money in a savings account — except it is not liquid. You cannot spend it directly. But you can access it, and when you do, it can change your financial picture significantly.

How Equity Builds Over Time

Equity builds in two ways.

The first is through your mortgage payments. Every payment you make reduces your principal balance — slowly at first, because early payments are weighted heavily toward interest, and faster over time as the balance decreases. After ten years of payments on a 30-year mortgage, you have paid down a meaningful chunk of your principal.

The second is through appreciation. If your home increases in value — because the neighborhood improved, because you renovated, because the market moved — your equity grows even if you have not made a single extra payment.

In Philadelphia, both have been happening. Homeowners who bought in neighborhoods like Point Breeze, East Passyunk, and parts of North Philadelphia five to ten years ago have seen significant appreciation on top of their mortgage paydown. Some of them are sitting on equity they do not even know they have.

What You Can Do With It

This is where it gets interesting for real estate investors and homeowners alike.

The most common way to access home equity is through a Home Equity Line of Credit — a HELOC. A HELOC works like a credit card secured by your home. You are approved for a maximum amount, you draw from it as needed, and you pay interest only on what you use.

Most lenders will let you borrow up to 80% of your home’s value minus what you owe. So on a $300,000 home with $180,000 owed, the math looks like this:

$300,000 × 80% = $240,000 $240,000 − $180,000 = $60,000 available HELOC

That $60,000 could fund a renovation on an investment property. It could cover a down payment on a rental. It could pay for a sheriff sale bid. Real estate investors use HELOCs as a source of capital all the time — because the interest rates are typically lower than hard money loans and the flexibility is hard to beat.

The Risk You Need to Understand

A HELOC is secured by your home. That means if you cannot repay it, you could lose your house.

This is not a reason to avoid HELOCs. It is a reason to use them carefully. Only draw on a HELOC for investments where the numbers genuinely work — not because you want to move fast or because a deal feels right. The math has to support the repayment.

I have seen investors use their home equity wisely to build real wealth. I have also seen people treat their home equity like a piggy bank and end up in serious trouble. The difference is discipline.

Cash-Out Refinancing

Another way to access equity is through a cash-out refinance. Instead of a line of credit, you refinance your entire mortgage for a higher amount and take the difference in cash.

If you owe $180,000 on a $300,000 home and refinance for $240,000, you receive $60,000 in cash at closing. Your new mortgage is larger and your monthly payment goes up, but you have liquid capital to deploy.

Cash-out refinancing made more sense when rates were lower. At today’s rates, a HELOC is often more practical for most homeowners — you keep your existing mortgage rate intact and only pay interest on what you draw.

How to Know If You Have Enough Equity to Act

The two numbers that matter are your loan-to-value ratio and your available equity.

Loan-to-value is your mortgage balance divided by your home’s current value. Most lenders want to see an LTV of 80% or below before they will approve a HELOC. If your LTV is above 80%, you either need to pay down more principal or wait for your home to appreciate further.

Available equity is what you can actually access — your home’s value times 80%, minus your current balance. If that number is positive and meaningful, you have options.

Find Out Where You Stand

I built a free Home Equity Calculator so you can see exactly how much equity you have, what your loan-to-value ratio is, and how much you might be able to access through a HELOC.

Enter your current home value, your remaining mortgage balance, and your original purchase price. It shows you your equity, your LTV, how much your home has appreciated since you bought it, and your estimated maximum HELOC availability.

Know your number. It might be larger than you think.

Use the free Home Equity Calculator below to find out exactly where you stand.