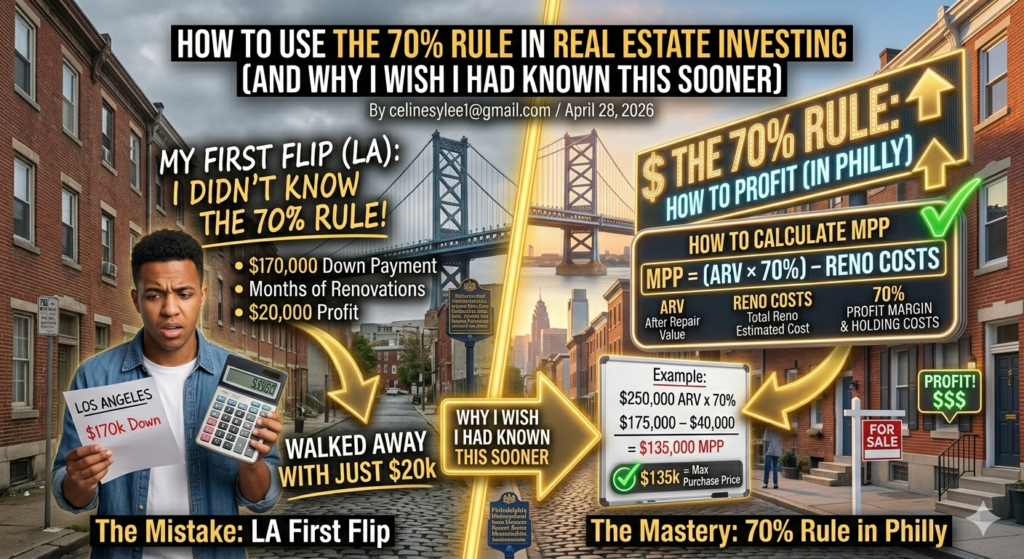

If you’re new to fix-and-flip investing, the 70% rule is one of the most important concepts you’ll ever learn. I’m going to be honest with you — when I did my first flip in Los Angeles, I had no idea this rule existed. I put down $170,000 as a 20% down payment, spent months watching renovations, and walked away with just $20,000 in profit. Something felt off, but I didn’t have the knowledge to understand why.

Now I do. And I’m going to explain it in the simplest way possible, so you don’t make the same mistakes I did.

What Is the 70% Rule?

The 70% rule is a quick formula that real estate investors use to figure out the maximum price they should pay for a fix-and-flip property.

Here’s the formula:

Maximum Purchase Price = (ARV × 70%) − Renovation Costs

That’s it. Let’s break it down.

ARV stands for After Repair Value — the estimated market value of the property after all renovations are complete. This is not what the house is worth today. This is what it will be worth once it’s fully fixed up and ready to sell.

The 70% is your safety margin. It accounts for your profit, holding costs, closing costs, agent commissions, and unexpected expenses that always seem to show up during a renovation.

Renovation Costs are exactly what they sound like — the total estimated cost to fix the property.

A Simple Example

Let’s say you find a property in Philadelphia. After researching comparable sales in the neighborhood, you estimate the ARV is $250,000. You get contractor bids and estimate renovations will cost $40,000.

Here’s how the 70% rule works:

$250,000 × 70% = $175,000 $175,000 − $40,000 = $135,000

That means the maximum you should pay for this property is $135,000. If the seller is asking $160,000, the deal doesn’t work. Walk away.

Simple. Powerful. And if I had known this before my first flip, I would have asked very different questions before signing anything.

Why Did I Only Make $20,000 on My First Flip?

This is the part I wish someone had explained to me before I wired that $170,000 down payment with shaking hands.

When I did my first flip in Los Angeles through a company that handled everything — finding the deal, managing renovations, selling the property — I trusted them completely. I was a beginner. I had just immigrated, my English wasn’t strong, and I was figuring out how to rebuild my life after a divorce. I didn’t know what questions to ask.

What I didn’t realize at the time was that every cost gets deducted from the sale price before you see a dollar of profit. Hard money loan interest — which was running over $3,000 per month. Renovation costs. Holding costs. The company’s fees. Agent commissions on the sale. By the time all of that came out, my share was $20,000 on a property that sold for hundreds of thousands of dollars.

Was the 70% rule being applied? Maybe. But I had no way to verify it, because I didn’t know it existed.

That’s why I’m writing this. Not to scare you away from flipping — I still believe in it, which is why I moved to Philadelphia to pursue it more seriously. But to make sure you go in with your eyes open.

The 70% Rule in Philadelphia

One of the reasons I love the Philadelphia market for fix-and-flip investing is that the numbers actually work here. In Los Angeles, ARVs are so high that even small mistakes get swallowed up. In Philadelphia, where you can buy properties for $80,000 to $150,000 and achieve ARVs of $200,000 to $300,000 after renovation, the 70% rule gives you real room to work with.

Let me walk through a real Philadelphia example:

Imagine a rowhouse in Germantown — a neighborhood I now live in and walk through every day looking at properties. The house needs significant work but has great bones. Comparable sales in the area suggest an ARV of $220,000. Renovation estimate comes in at $45,000.

$220,000 × 70% = $154,000 $154,000 − $45,000 = $109,000

If you can buy that house for $109,000 or less, the deal has potential. If the seller wants $130,000, you either negotiate down or move on.

That’s the discipline the 70% rule gives you. It takes emotion out of the equation and replaces it with math.

The Limits of the 70% Rule

The 70% rule is a starting point, not a guarantee. Here’s what it doesn’t account for:

Inaccurate ARV estimates. If your comparable sales analysis is wrong, your entire calculation is wrong. This is the most common mistake beginners make — overestimating what a renovated property will actually sell for.

Renovation cost surprises. Experienced investors build a contingency buffer — usually 10% to 20% on top of contractor estimates — because something always costs more than expected.

Market timing. A property that looks great on paper today might sit on the market for six months if you’re selling into a slow market. Every extra month of holding costs eats into your profit.

The 70% rule won’t protect you from all of these risks. But it will stop you from overpaying for a property before you even start — which is the most preventable mistake in fix-and-flip investing.

Final Thoughts

If there’s one thing I want you to take away from this article, it’s this: learn the numbers before you touch the money.

When I did my first flip, I was newly divorced, still finding my footing in America, and my English wasn’t strong enough to ask the right questions. So I trusted a company run by people from my own community. I assumed that shared background meant shared interests. It didn’t.

The 70% rule takes five minutes to understand and could save you from years of regret. No one is going to protect your money the way you will — not a company, not a partner, not someone who looks like you or speaks your language.

You have to study. There are no shortcuts.

I learned that the hard way in Los Angeles. You don’t have to.

🏠 Free ARV Calculator

ARV × 70%

$—

Max Purchase Price

$—

Formula: (ARV × 70%) − Renovation Costs = Max Purchase Price