Rent or buy Philadelphia — this is the question I ran the numbers on before I even moved here from Los Angeles. People thought I was crazy leaving LA. LA has the weather, the glamour, the real estate prices that make people feel like they’re sitting on gold.

Philadelphia has rowhouses, soft pretzels, and property taxes that won’t make you cry.

I’ll take Philadelphia.

Here’s what the math actually says about whether to rent or buy Philadelphia in 2026.

Should You Rent or Buy Philadelphia Right Now?

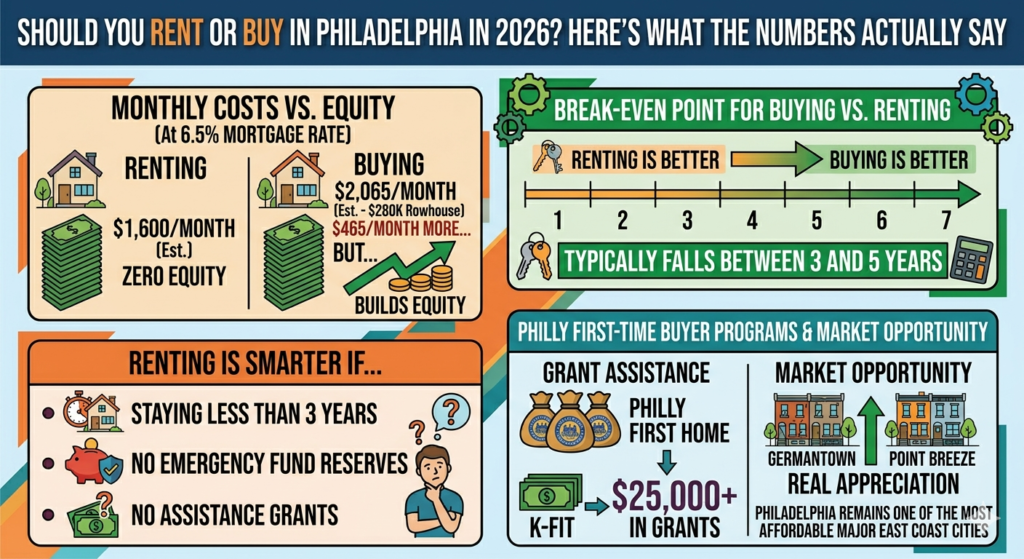

With mortgage rates still elevated around 6.5% and home prices rising steadily, a lot of people are asking the same question: does it actually make financial sense to rent or buy Philadelphia right now, or should you keep renting and wait?

The honest answer: it depends on your specific numbers. But I can show you what the math looks like for a typical Philadelphia buyer in 2026.

A Real Rent or Buy Philadelphia Example

Let’s say you’re currently renting a two-bedroom in West Philadelphia for $1,800 a month. You’ve found a rowhouse nearby listed at $280,000. You have $25,000 saved for a down payment.

Here’s what buying looks like:

| Expense | Monthly |

|---|---|

| Mortgage ($255K at 6.5%, 30yr) | $1,612 |

| Philadelphia property tax (1.3% annually) | $303 |

| Homeowner’s insurance | $117 |

| Maintenance reserve (1% annually) | $233 |

| Total monthly cost of owning | $2,265 |

Compared to your $1,800 rent, buying costs you $465 more per month. On the surface, renting looks cheaper.

But that’s only part of the rent or buy Philadelphia picture.

What Renting Costs You Over Time in the Rent or Buy Philadelphia Decision

Over 5 years of renting at $1,800 per month, you spend $108,000 in rent. You own nothing at the end of it. That money is gone.

Over the same 5 years of owning, your $280,000 home — appreciating at Philadelphia’s historical rate of roughly 3% per year — is worth approximately $324,000. You’ve paid down some of your mortgage. You’ve built equity.

When you factor in appreciation and equity building, buying typically wins over a 5-year horizon in Philadelphia — even at today’s rates.

The rent or buy Philadelphia break-even point — the moment when buying becomes cheaper than renting on a total cost basis — typically falls somewhere between 3 and 5 years in most Philadelphia neighborhoods right now.

When Renting Still Makes Sense in the Rent or Buy Philadelphia Decision

The rent or buy Philadelphia decision doesn’t always favor buying. Renting is probably smarter if:

You’re not sure you’ll stay for at least 3 years. The transaction costs of buying and selling — agent commissions, closing costs, transfer taxes — are significant. If you sell too soon, you won’t have enough appreciation to cover them.

Your down payment would wipe out your entire emergency fund. Homeownership comes with unexpected costs. HVAC systems fail. Roofs leak. You need reserves.

Your debt-to-income ratio is too high to qualify for a reasonable rate. A higher interest rate changes the rent or buy Philadelphia math significantly. Take the time to pay down debt first.

Why Philadelphia Specifically Makes Sense for the Rent or Buy Philadelphia Decision Right Now

Philadelphia is one of the most affordable major cities on the East Coast. The median home price here is a fraction of what you’d pay in New York, Boston, or Washington DC — cities within easy driving distance.

Neighborhoods that were overlooked five years ago are seeing real price appreciation now. Germantown, Kensington, East Passyunk, Point Breeze — buyers who got in early in these neighborhoods have seen significant gains.

And Philadelphia has some of the most generous first-time homebuyer assistance programs in the country. Between Philly First Home, K-FIT, and other programs, eligible buyers can receive $25,000 or more in grant assistance. That changes the rent or buy Philadelphia math dramatically.

According to Census.gov, Philadelphia’s homeownership rate has consistently lagged comparable East Coast cities — meaning more renters are paying into someone else’s equity instead of their own, making the rent or buy Philadelphia decision more consequential here than in markets with higher ownership rates.

Run Your Own Rent or Buy Philadelphia Numbers

Every rent or buy Philadelphia situation is different. Your rent, your target purchase price, your down payment, how long you plan to stay — all of it affects the calculation.

Don’t make this decision based on what someone told you at a dinner party. Run the numbers yourself.

Use the Philadelphia Rent vs Buy Calculator to plug in your specific numbers and see exactly where the rent or buy Philadelphia break-even point is for your situation.

Not financial advice — just someone doing a lot of research and asking a lot of questions.