I’ve been studying new construction investing for a while now. And the more I dig into it, the more one specific strategy keeps jumping out as the sweet spot that most people completely overlook.

Not a single-family spec home. Not a large apartment complex. A fourplex. Four units, built from the ground up, on a piece of land you control.

Here’s why the math on this is so compelling — and why the fourplex sits in a uniquely advantageous position that nothing else quite replicates.

The Magic Number: Why 4 Units Changes Everything

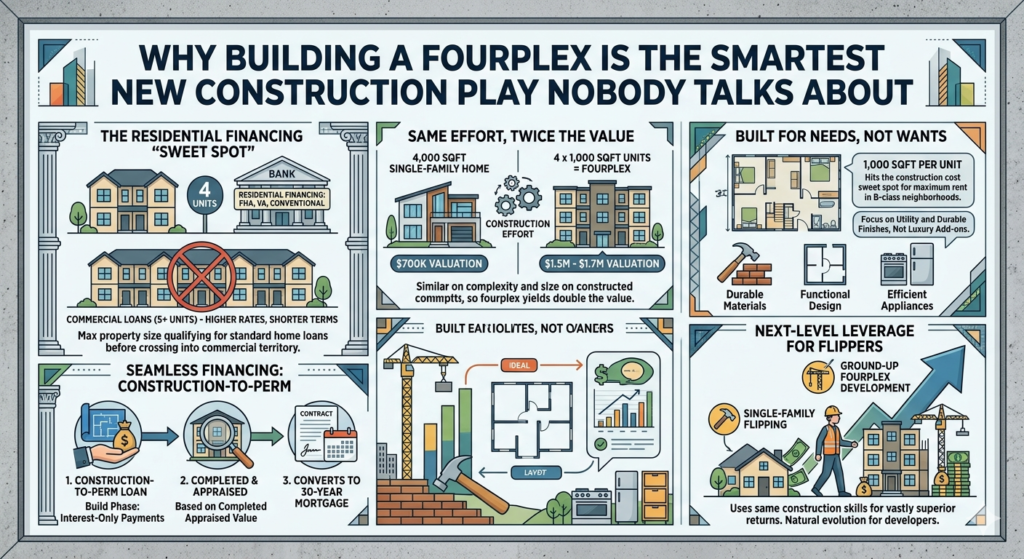

In the eyes of lenders, there’s a hard line at 5 units.

1–4 units = residential asset. Conventional financing, FHA loans, VA loans, owner-occupant programs — all available.

5+ units = commercial asset. Higher down payments, stricter underwriting, shorter loan terms, balloon payments, higher rates.

This distinction is enormous. And it means a fourplex — the largest property you can build while still accessing residential financing — occupies a uniquely powerful position.

You get:

- Commercial-level income (four rent checks per month)

- Residential loan terms (30-year fixed, low down payment options)

- Owner-occupant financing if you live in one unit

Nothing above four units gets you this combination. A fiveplex immediately crosses into commercial territory and the financing picture changes dramatically.

The fourplex is the ceiling of residential financing — and smart investors build right up to that ceiling.

Same Effort, Twice the Value

Here’s the comparison that stopped me mid-scroll when I first understood it.

Building a 4,000 square foot single-family home and building a fourplex with four 1,000 square foot units involves roughly the same construction process. Same foundation work. Same framing. Similar materials. Similar timeline. Similar contractor coordination.

The difference is what you end up with.

Single-family home (4,000 sqft):

- Valued by neighborhood comps

- One income stream (or zero if it’s your primary residence)

- Appraised at roughly $700,000 in many markets

Fourplex (4 × 1,000 sqft units):

- Valued by income (NOI ÷ Cap Rate)

- Four income streams

- Appraised at $1.5M–$1.7M based on rental income

Same construction effort. Potentially $800,000–$1,000,000 difference in value.

That gap exists because the valuation method is completely different. A single-family home is worth what similar homes nearby sold for. A fourplex is worth what its income produces — and you control that income.

The Numbers: Building a $1.7M Asset

Let me walk through the math on a realistic fourplex build.

Construction costs:

- Land acquisition: $200,000

- Construction costs (4 units × ~$185/sqft × 4,000 sqft): $740,000

- Soft costs (permits, architecture, engineering): $60,000

- Financing costs (construction loan interest): $45,000

- Contingency (10%): ~$90,000

- Total all-in cost: ~$1,135,000

Some markets will be lower, some higher. But this is a reasonable baseline for a mid-tier market.

Income side:

- 4 units at $2,500/month each: $120,000/year gross

- Vacancy (5%): -$6,000

- Operating expenses (20%): -$24,000

- NOI: ~$90,000/year

Valuation: At a 5.5% cap rate:

$90,000 ÷ 0.055 = $1,636,000

At a 5% cap rate (stronger market):

$90,000 ÷ 0.05 = $1,800,000

Equity created:

$1,636,000 − $1,135,000 = $501,000 in equity

Built in roughly 12–14 months. From a vacant lot.

That’s not a flip profit — that’s permanent equity in a cash-flowing asset you can refinance, hold, or sell.

The Construction-to-Perm Loan: How to Finance the Build

Building a fourplex requires different financing than buying one. You can’t get a 30-year mortgage on a property that doesn’t exist yet.

The solution is a construction-to-permanent loan — a two-phase financing product that covers both the build and the long-term hold.

Phase 1: Construction loan

- Covers land acquisition and construction costs

- You draw funds in stages as construction progresses

- During construction, you pay interest only on the amount drawn

- Typically 12–18 months

Phase 2: Permanent conversion

- Once construction is complete and the property is appraised

- Loan automatically converts to a standard 30-year mortgage

- Based on the completed appraised value — not your construction costs

This second phase is where the equity play happens. If you built for $1,135,000 and the property appraises at $1,636,000, your permanent loan is based on the $1,636,000 value. At 75% LTV:

$1,636,000 × 0.75 = $1,227,000 permanent loan

That loan pays off your construction loan balance and potentially returns cash to you — all while converting to a long-term fixed rate you can hold indefinitely.

Owner-Occupant Advantage: Living There While It Pays You

If you’re willing to live in one of the four units, the financing picture gets even better.

As an owner-occupant on a 1–4 unit property, you can access:

FHA financing: 3.5% down on the completed property value VA financing: 0% down (if you qualify) Fannie Mae 5% down: Conventional financing with cancellable PMI Construction-to-perm with owner-occupant terms: Lower down payment requirements during the build

Living in one unit while renting the other three is classic house hacking — except you built the asset from scratch, which means you captured the construction equity before you ever moved in.

Three units at $2,500/month = $7,500/month covering your mortgage, taxes, insurance, and then some. Your housing cost could approach zero — or actually generate cash flow — from day one.

The 1,000 Square Foot Rule: Build for Needs, Not Wants

Here’s a design principle worth internalizing: build what the market needs, not what looks impressive in a rendition.

Four units at 1,000 square feet each is the sweet spot. Large enough for a family — two or three bedrooms, functional kitchen, adequate living space. Small enough to keep construction costs manageable and rents accessible to a wide tenant pool.

The temptation in new construction is to add features. Quartz countertops. Open floor plans. High ceilings. Premium finishes throughout.

Resist it. Every dollar you add to construction costs has to be justified by either higher rents or higher appraised value. And in the working-class and middle-market neighborhoods where fourplex investing makes the most sense, tenants need functional, clean, and well-maintained — not luxury.

A $2,500/month rent in a solid B-class neighborhood is achievable with a well-designed 1,000 square foot unit. The same unit with $50,000 in premium finishes might get $2,700. That $200/month increase does not justify $50,000 in additional construction cost.

Build practical. Build durable. Build what families actually need.

Why This Is my Roadmap

I’ll be honest about where I am. I’m not building a fourplex tomorrow. My current focus is on single-family flips — building experience, relationships, and capital.

But this is exactly the next step on my roadmap. Once you’ve done a flip or two, you understand construction. You have contractor relationships. You know how to manage a project timeline and a budget. You’ve seen what can go wrong and how to handle it.

That’s when a ground-up fourplex starts to make sense. You’re not learning construction for the first time on a $1M+ project. You’re applying skills you already have to a bigger, more leveraged opportunity.

The gap between a single-family flip and a ground-up fourplex is smaller than most people think. The construction process is similar. The financing is more complex but learnable. And the outcome — half a million dollars in equity from a single project — is a different category of result.

That’s worth working toward.