Every few weeks a new video pops up in my feed. The thumbnail is always some variation of a house on fire, a graph going straight down, or a panicked face. The title is always something like “HOUSING MARKET ABOUT TO EXPLODE” or “THE CRASH IS HERE.”

I click. I watch. I get mildly anxious. And then I go look at the actual data and feel better.

This has happened enough times that I’ve developed a reflex: when a YouTube video promises me a housing crash is imminent, I immediately want to see the sources.

Here’s what I’ve found when I actually look.

The Data Points That Are Real

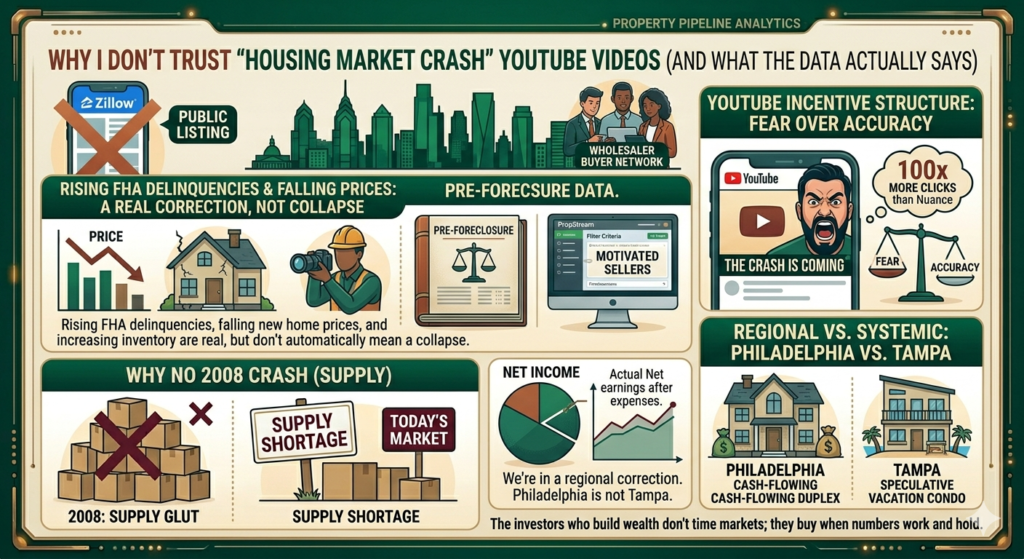

Let me be fair. The crash videos aren’t making things up entirely. Some of the data points they cite are real.

FHA delinquency rates are rising. 90-day delinquencies on FHA loans have increased meaningfully. This is worth watching — FHA borrowers tend to be lower-income and more vulnerable to economic stress.

New home prices have dropped. Builders have been cutting prices and offering rate buydowns to move inventory. The median new home sale price is down from its peak.

Inventory is rising. More homes are sitting on the market longer than they were in 2021–2022. In some markets — particularly Florida and parts of Texas — the increase is significant.

Foreclosure filings are up. After the pandemic moratoriums ended, foreclosure activity has been climbing back toward pre-pandemic levels.

All of this is true. None of it automatically means a crash is coming.

The Part Where the Videos Go Off the Rails

Here’s where I get skeptical.

Comparing to 2008

Every crash video compares current conditions to 2008. The implication is always the same: we’re heading for a repeat.

But 2008 happened for specific reasons that don’t exist today.

In 2008, the problem was too much supply and too many unqualified borrowers. Banks were handing out mortgages to people who couldn’t afford them — no income verification, no down payment, adjustable rates that reset to payments no one could make. When those loans started defaulting en masse, the whole system collapsed.

Today, lending standards are dramatically tighter. The people who have mortgages generally qualified for them under real scrutiny. And as we covered in the last post, many of them have 3% fixed rates they have zero incentive to give up — which means they’re not going to sell, which means supply stays constrained, which means prices have a floor.

“AI will eliminate 50% of white-collar jobs”

This is a prediction, not data. It might be right. It might be wildly off. Using it as the foundation for a housing market crash thesis is speculative at best.

“Property values are a fraud”

One video I watched recently claimed that the last five years of home value appreciation was essentially manufactured by corrupt appraisers to increase property tax revenue.

I’m going to be direct: this is not serious analysis. Home values reflect supply and demand. Demand exploded during the pandemic as remote work unlocked geographic flexibility and low rates unlocked purchasing power. Supply couldn’t keep up. Prices rose. That’s not fraud — that’s a market responding to conditions.

Why These Videos Exist

I don’t think most of these creators are deliberately lying. I think they’ve figured out something true about YouTube: fear drives clicks.

A video titled “Housing Market Remains Complicated With Regional Variation” gets 3,000 views. A video titled “THE CRASH IS COMING — GET OUT NOW” gets 300,000 views. The incentive structure rewards alarm, not accuracy.

This is true across financial YouTube — not just housing. The loudest voices are usually the most extreme ones. The people doing careful, nuanced analysis of data tend to have smaller audiences because careful and nuanced doesn’t make great thumbnails.

I try to remember this every time I feel the urge to panic-watch market commentary.

What the Data Actually Suggests

Here’s my honest read of the current market — not a prediction, just pattern recognition.

We’re in a correction, not a collapse. Some markets that ran too hot — parts of Florida, Phoenix, Boise — are seeing meaningful price declines. That’s healthy. It’s the market normalizing after an extraordinary period, not a systemic failure.

The lock-in effect is real and it’s a floor. As long as millions of homeowners have 3% mortgages, they’re not selling. As long as they’re not selling, supply stays low. As long as supply stays low, prices have significant downward resistance.

FHA delinquencies are worth watching, not panicking about. Rising delinquencies are a warning sign, not a verdict. The question is whether they cascade into mass defaults — and that depends on employment. As long as people have jobs, most will find a way to make their mortgage payment.

Regional variation matters enormously. “The housing market” is not one thing. Philadelphia is not the same as Tampa. A duplex in West Philly is not the same as a vacation condo in Cape Coral. Blanket crash predictions that treat all markets identically are almost always wrong somewhere and right somewhere else.

How I’m Actually Thinking About This

I’ll be honest about where I land personally.

I’m not buying anything right now — not because I think a crash is coming, but because my own preparation isn’t there yet. I’m building knowledge, building relationships, and building capital. When the right deal comes along in the right market at the right price, I want to be ready to move — not paralyzed by YouTube anxiety.

The investors I respect most aren’t trying to time the market. They’re buying when the numbers work, regardless of what the macro commentary says. A property that cash flows at today’s rates cash flows at today’s rates. If rates drop, you refinance and it cash flows even better. If values drop, you hold and wait.

The crash videos want you frozen — watching more videos, clicking more thumbnails, living in a state of perpetual uncertainty. That’s good for their view counts. It’s not good for your financial life.

Look at the actual data. Understand your local market. Run the numbers on specific deals. And maybe turn off the YouTube algorithm for a while.

Not financial advice — just someone doing a lot of research and asking a lot of questions.