I didn’t know there was a wall.

Not a physical one — a financial one. The kind that stops a lot of real estate investors cold the moment they try to scale from a small rental into something bigger.

I’ve been deep in the research rabbit hole lately, and I stumbled across something that completely changed how I think about 5 unit property financing — and honestly, about real estate debt in general. So let me walk you through what I learned, because nobody really explains this stuff in plain English.

What Changes the Second You Cross 5 Units

Here’s the thing nobody tells you when you’re buying your first duplex or triplex: the rules are completely different once you hit five units.

With 1 to 4 units, you’re in residential territory. You can get a 30-year fixed mortgage, go through a regular lender, and lock in your rate for three decades. It’s not easy, but the structure is familiar.

The moment you buy a 5-unit property? You’ve crossed into commercial lending. And 5 unit property financing does not work the same way.

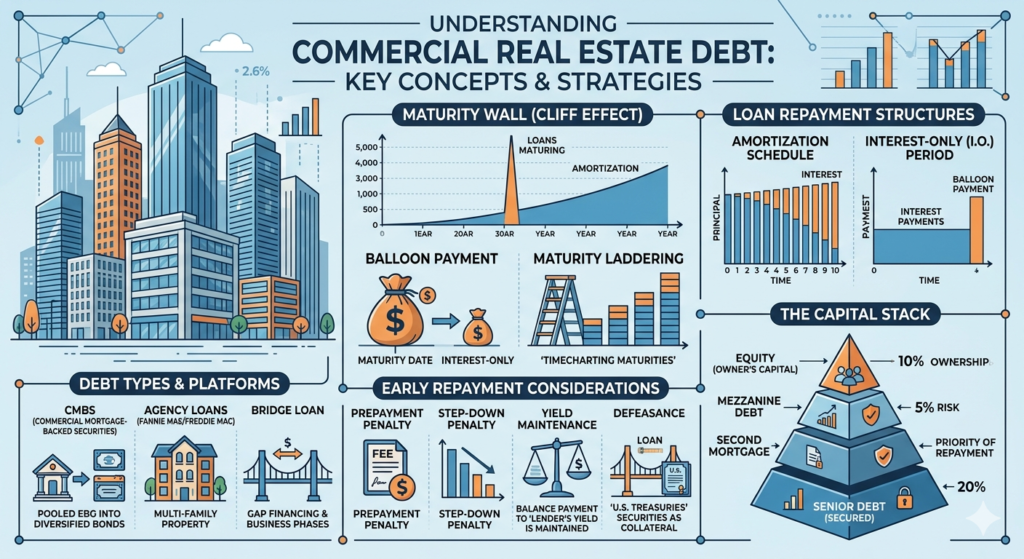

- Loan terms are shorter — typically 5, 7, or 10 years

- After that term ends, you don’t just keep paying. The whole loan comes due — that’s called a balloon payment

- You have to refinance or pay it off entirely

- The rate you refinance at depends on whatever the market looks like at that moment

That last part is what trips people up.

The $875 Billion Problem (And Why It Matters to Small Investors)

You might’ve seen headlines about the commercial real estate debt crisis in 2026. Here’s the short version.

A huge wave of commercial loans — including a lot of multifamily apartment buildings — were originated back in 2020 and 2021 when interest rates were at historic lows. Around 2 to 3 percent. Investors borrowed big, bought big, and felt great about it.

Those loans had 5-year terms. Which means they’re all coming due right now, in 2026.

According to the Mortgage Bankers Association, roughly $875 billion in commercial and multifamily mortgage debt is maturing in 2026 alone. And current rates are sitting around 6 to 7 percent — more than double what these investors originally borrowed at.

So they have to refinance at twice the rate. Monthly payments shoot up. Some properties that were cash-flowing fine are suddenly barely breaking even. Some investors can’t qualify for the new loan at all.

This is what people mean when they say “maturity wall.” And it’s not just a big-investor problem. That 50-unit apartment building down the street from you? Same issue. That 12-unit your mentor just sold? Same issue.

5 unit property financing is just a smaller version of the same game.

The Mistake Everyone Makes: Creating the Next Wall

Okay, so you understand the problem. Now here’s where it gets interesting.

When a lot of these commercial borrowers go to refinance right now, they’re doing the obvious thing — just rolling everything into another 5-year loan. Same structure, just a new rate.

The problem? They’re setting themselves up for a 2031 maturity wall.

Same situation. Same squeeze. Just five years later.

The smarter play — and this is something I hadn’t thought about before I went down this research hole — is called maturity laddering. Instead of refinancing everything into one term, you split it. Half goes to 5 years, half goes to 7 or 10 years. Your debt matures at different times, so you’re never caught refinancing everything at once in a bad market.

It’s the same reason you don’t put all your savings into one CD with the same maturity date. You stagger it. You give yourself options.

For someone like me, who’s still in the research phase of understanding 5 unit property financing and beyond, this was genuinely eye-opening. It’s not just about getting the loan. It’s about structuring the loan smartly from day one.

So How Do You Actually Finance a 5+ Unit Property?

If you’re thinking about making the jump from small residential to multifamily, here are the main financing routes people use for 5 unit property financing:

DSCR-Based Commercial Loans The lender looks at the property’s income, not your personal income. If the rents cover the debt service — usually at a ratio of 1.25x or higher — you can qualify. This is one of the more accessible routes for investors who are self-employed or have non-traditional income. I use this [DSCR Calculator] to run quick numbers before I even think about calling a lender.

Agency Loans (Fannie Mae / Freddie Mac Multifamily) These are specifically designed for 5+ unit residential properties. Terms tend to be better than standard commercial loans, and they can go up to 30 years in some cases. But there are stricter property condition requirements and it takes longer to close.

Bridge Loans Short-term financing — usually 12 to 36 months — used to stabilize a property before refinancing into permanent debt. You’d use this if the building has high vacancy or needs work. Higher rates, but buys you time.

Private or Hard Money Faster and more flexible. Rates are high (think 10 to 13 percent) but useful when you need to move quickly or when traditional lenders say no. And “no” from a bank isn’t permanent — it usually just means “not right now with this structure. Run your numbers first with this [Hard Money Loan Calculator] — the interest adds up fast.

The Part That Actually Surprised Me

I’ve been focused almost entirely on residential deals — flips, BRRRR, maybe a small rental or two. Commercial felt like some other world I wasn’t ready for yet.

But here’s what clicked for me: the concepts are the same, just scaled up.

BRRRR is basically a bridge-to-permanent refinance strategy. The maturity wall is just what happens when thousands of investors all did their BRRRR in the same year with the same loan term. Maturity laddering is just… not putting all your eggs in one basket.

Understanding 5 unit property financing doesn’t mean you have to go buy a 10-unit tomorrow. But knowing how this works — how commercial debt is structured, why terms matter, why the timing of your refinance is as important as the rate — makes you a smarter investor at every level.

Even if you’re still on your first deal.

Not financial advice — just someone doing a lot of research and asking a lot of questions.