Real estate depreciation taxes are one of the most powerful — and most misunderstood — tools available to property investors. I didn’t fully get it until recently. And once it clicked, I couldn’t believe more people weren’t talking about it.

Here’s the short version: the IRS lets you deduct the “wear and tear” on your building every single year — even if your property is actually going up in value. You’re not losing money. The building isn’t falling apart. But on paper, you get to claim a loss. And that loss reduces your taxable income.

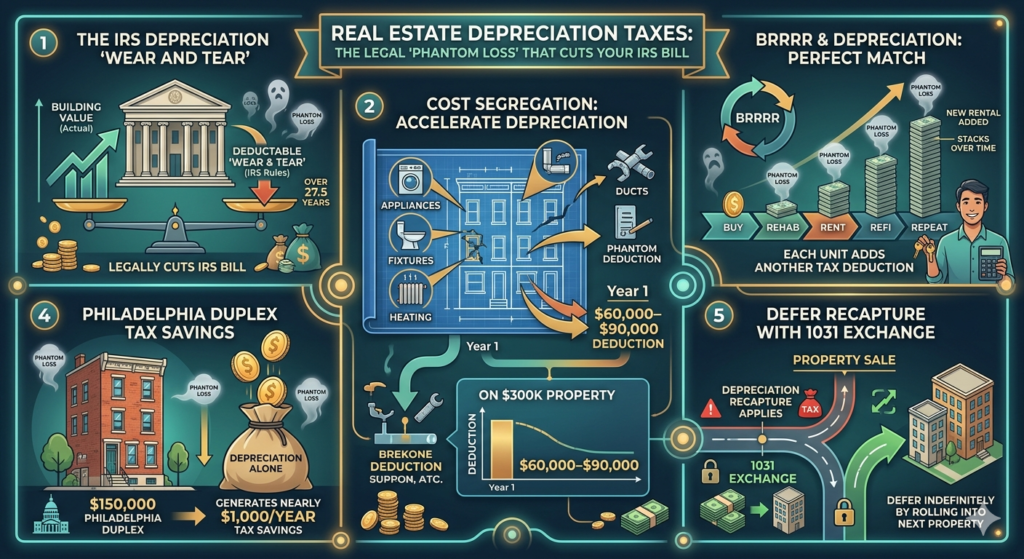

That’s what investors call a Phantom Loss — and it’s completely legal.

How Real Estate Depreciation Taxes Actually Work

The IRS assumes every residential rental property wears out over 27.5 years. That’s a fixed rule — not negotiable, not optional. It applies to every landlord in America equally.

So if you buy a rental property and the building portion is worth $275,000, here’s the math:

- $275,000 ÷ 27.5 years = $10,000 per year depreciation

That $10,000 gets subtracted from your taxable income every single year — even if your property went up in value that year.

Example:

- Rental income: $18,000/year

- Expenses: $5,000/year

- Net income before depreciation: $13,000

- Minus depreciation: $10,000

- Taxable income: $3,000 (instead of $13,000)

At a 30% tax rate, you just saved $3,000 in taxes. On money you never actually lost.

Cost Segregation: How to Accelerate Real Estate Depreciation Taxes

Standard depreciation spreads everything over 27.5 years. Cost Segregation speeds that up dramatically.

Here’s how it works: instead of treating the entire building as one asset, a Cost Segregation study breaks it into components:

- Carpet, lighting, appliances → 5-year depreciation

- Parking lot, landscaping → 15-year depreciation

- Building structure → 27.5-year depreciation

The short-life components can then qualify for Bonus Depreciation — meaning you can deduct them all in year one instead of spreading them out.

On a $300,000 property, roughly 20–30% might qualify as short-life components. That’s $60,000–$90,000 in accelerated deductions potentially available in year one alone.

Why does this matter? Because money saved on taxes today is worth more than money saved five years from now. That $20,000–$25,000 in tax savings can go straight into your next deal.

According to the IRS Cost Segregation Audit Techniques Guide, this is a fully legal and widely used strategy — not a loophole, but an intentional part of the tax code.

Why BRRRR and Real Estate Depreciation Taxes Are a Perfect Match

This is where it gets really interesting.

BRRRR (Buy, Rehab, Rent, Refinance, Repeat) is already a powerful strategy on its own. But combine it with depreciation and the numbers get even better.

Here’s why:

- Buy → Get into the deal with limited cash

- Rehab → Force appreciation, increase value

- Rent → Depreciation clock starts the moment you place a tenant ✅

- Refinance → Pull your cash back out

- Repeat → Buy another property → another depreciation deduction ✅

Every time you add a rental to your portfolio, you add another depreciation deduction. Two properties = two deductions. Five properties = five deductions. The tax benefits stack as your portfolio grows.

And here’s the part that really got me: the building can be going up in value — which it often does in markets like Philadelphia right now — while you’re simultaneously claiming depreciation on it. You’re building wealth AND reducing your tax bill at the same time.

Use the BRRRR Calculator to run your numbers before you commit to any deal.

What This Looks Like for a Small Investor Starting Out

You don’t need a $2 million building to benefit from real estate depreciation taxes. A $150,000 duplex in Philadelphia works the same way.

Example:

- Purchase price: $120,000

- Building value (land excluded): $90,000

- Annual depreciation: $90,000 ÷ 27.5 = $3,272/year

- At 30% tax rate: $981 saved every year — without spending a single extra dollar

That’s nearly $1,000 back in your pocket annually just from owning the property. And if you do a Cost Segregation study and accelerate some of that depreciation into year one, the savings get significantly larger.

Philadelphia’s land values have been climbing steadily. That means the asset is appreciating while the depreciation benefit runs in parallel — a combination that’s hard to beat.

Use the Rental Property ROI Calculator to see what your actual return looks like when you factor in depreciation.

One Important Caveat

Depreciation isn’t free forever. When you eventually sell the property, the IRS “recaptures” the depreciation you claimed and taxes it — typically at 25%. This is called depreciation recapture.

The good news: a 1031 Exchange lets you defer that recapture by rolling your proceeds into another property. Which means you can keep pushing that tax bill forward indefinitely — as long as you keep investing.

This is why serious real estate investors rarely sell. They refinance, they exchange, they hold. The tax code is built to reward long-term ownership.

The Bottom Line

Real estate depreciation taxes are one of the few places where the tax code genuinely works in the small investor’s favor. You don’t need to be wealthy to use it. You just need to own a rental property and understand the rules.

Start with one deal. Run the BRRRR strategy. Keep the property as a rental. Let depreciation work in the background while your asset appreciates.

Not financial advice — just someone doing a lot of research and asking a lot of questions.