I’ll be honest with you. Getting a bank loan for real estate investing is one of the most intimidating steps I’ve taken as an immigrant investor — and nobody prepares you for what it actually feels like. when I first walked into a major bank in this country, I wasn’t trying to get a bank loan for real estate investing. I just wanted to open a checking account. My own money. My own account. And somehow I still felt like I was being tolerated rather than welcomed.

I moved to the U.S. from Korea in my 30s. My English works — but it’s not perfect, and when I get nervous, it gets worse. Walking into a bank alone, trying to explain what I want, feeling the subtle shift in how they look at you when your accent comes through — that’s a real thing. And if you’ve experienced it, you know exactly what I mean.

So when I started seriously researching bank loan real estate investing options, I knew I couldn’t just follow the generic advice. I had to figure out a version that actually works for someone like me.

Here’s what I found — and a few things I figured out on my own.

Why Getting a Bank Loan for Real Estate Investing Is Harder Than People Think

Most advice online assumes you walk in confident, fluent, and already know everyone at the branch. That’s not most of us.

The truth is, bank loan real estate investing isn’t just about credit scores and income statements. It’s about how the banker perceives you the moment you walk in. Are you someone they want to help? Or are you someone they’re going to hand a pamphlet and send home?

That perception gap is real. And once I understood it, I started working with it instead of against it.

7 Things That Will Kill Your Bank Loan Real Estate Investing Chances

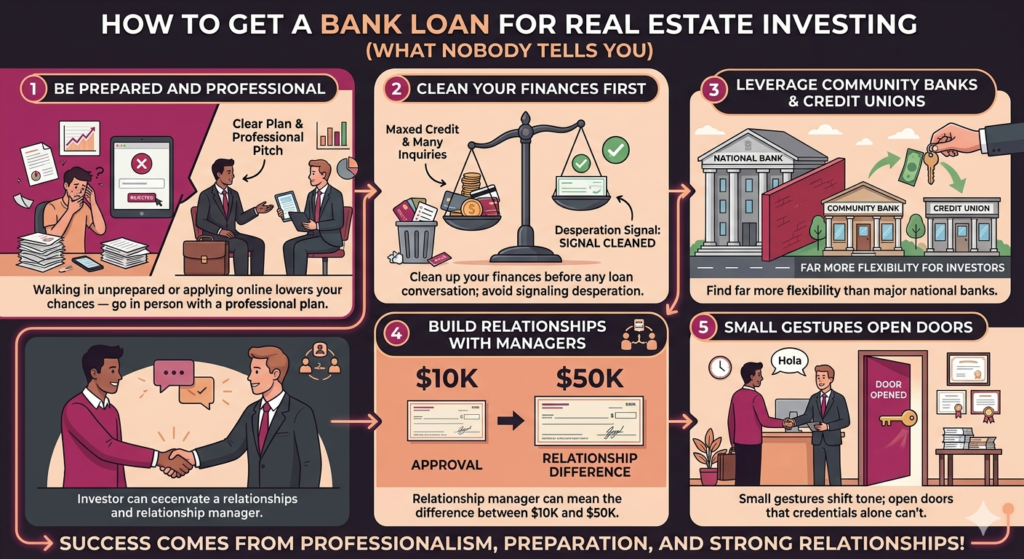

1. Walking In Without Preparation

“I’m just here to learn about my options” is the fastest way to get a low offer or a flat no. Banks lend to people who look like they already know what they’re doing — even if they’re still learning.

Before you go in, have your numbers ready. What property are you looking at? What’s the ARV? What’s your plan? Write it down. Practice saying it. You don’t need to be perfect. You need to sound like you’ve thought about it.

2. Applying Online

For serious money, skip the website. Online applications go through automated systems with no room for nuance, no relationship, no negotiation. You get a box score — and if you don’t fit perfectly, you’re out.

Go in person. Ask to speak with a relationship manager, not just a teller. That conversation is where real decisions get made.

3. Maxed Out Credit Before You Apply

If your credit cards are near their limits when you walk in, the bank sees someone who’s stretched. Clean that up first. Pay down balances. Give yourself some breathing room before you ever have the loan conversation.

Use the Credit Score Improvement Tracker to get your credit in shape before you start any bank loan real estate investing conversation.

4. Too Many Credit Inquiries in a Short Window

Multiple hard pulls in a short period send a signal: this person is desperate and getting rejected everywhere. Space out your applications strategically, or bundle them correctly so they count as rate shopping rather than a credit spiral.

5. Saying “I’m Thinking About Trying Real Estate”

Banks don’t fund experiments. They fund businesses.

“I’m thinking about getting into flipping” → red flag. “I’m a residential developer focused on fix-and-flip properties in the Philadelphia market” → completely different conversation.

Same person. Same situation. Completely different outcome based on how you frame it.

6. Only Talking to One Bank

One bank is one opinion. If you want real money — $100K, $200K, more — you need relationships at multiple institutions. Community banks, credit unions, regional lenders. Each one is a different conversation and a different set of options.

According to the FDIC, community banks make up the majority of small business and real estate lending in the U.S. — and they operate very differently from the big nationals when it comes to flexibility.

7. Ignoring the Relationship

The difference between a $10,000 credit line and a $50,000 approval is often one person: the relationship manager who decides how hard to push your file internally.

That relationship takes time. Check in. Update them when you close a deal. Bring them good news occasionally. Treat them like a business partner, not an ATM.

The Thing Nobody Else Is Going to Tell You

Here’s the tip I figured out on my own — and I’m sharing it because I genuinely think it helps.

I speak a little Spanish. Some Arabic. A bit of Mandarin. Enough to say hello, ask how someone’s doing, maybe crack a small joke.

When I walk into a branch and the banker is clearly from an Arabic-speaking background, I’ll open with a greeting in Arabic. Just a few words. Nothing fancy.

You want to talk about walls coming down? It’s instant.

People light up when you meet them in their own language — even just a word or two. It signals respect. It signals that you see them as a person, not just a function. And suddenly the whole tone of the conversation shifts.

I know this sounds small. But when you’re an immigrant whose English gets shaky under pressure, and you’re trying to get a bank loan for real estate investing — anything that makes the other person want to help you matters.

I’m not going to pretend I’m not nervous about doing this alone. Getting a loan by yourself, in a language that isn’t your first, in a system you didn’t grow up in — it’s genuinely intimidating. That’s exactly why I’ve been studying all of this. So that when I walk in, I’m as prepared as I can possibly be.

And now you have this too.

Community Banks vs. Big Banks for Real Estate Loans

This is why bank loan real estate investing works so much better through community banks than national lenders.

This deserves its own section because it’s that important.

Major national banks have rigid underwriting. Everything goes through a system. If you don’t fit the box perfectly — W-2 income, clean credit, years of U.S. banking history — you’re going to have a hard time.

Community banks and credit unions work differently. They make portfolio loans — loans they keep on their own books rather than selling to the secondary market. That means they have more flexibility on structure, terms, and who they lend to.

For anyone pursuing bank loan real estate investing seriously, community banks are often the better starting point. The relationship manager actually has decision-making power. Your story matters, not just your score.

Before You Walk Into Any Bank

The truth is, bank loan real estate investing success starts long before you ever walk through the door.

Know your numbers. Know your plan. Know what you’re asking for and why it makes sense.

Not financial advice — just someone doing a lot of research and asking a lot of questions.