Real estate deal analysis doesn’t start with picking a strategy. It starts with running the numbers — and letting the numbers tell you what kind of deal you’re looking at.

I used to do it backwards. I’d look at a property, decide what strategy I wanted to use, then try to make the numbers fit. That’s how you talk yourself into bad deals.

I came across a video recently where a father was teaching his son how to analyze deals, and the framework he used flipped everything around. Run the numbers first. The numbers tell you the strategy. Here’s exactly how it works.

The Two Numbers You Need for Real Estate Deal Analysis

Before you can classify any deal, you need two things:

All-in Cost — your purchase price plus your total estimated repair costs. Everything it takes to get the property to finished condition.

ARV (After Repair Value) — what the property will be worth once it’s fully renovated, based on real comparable sales in the area.

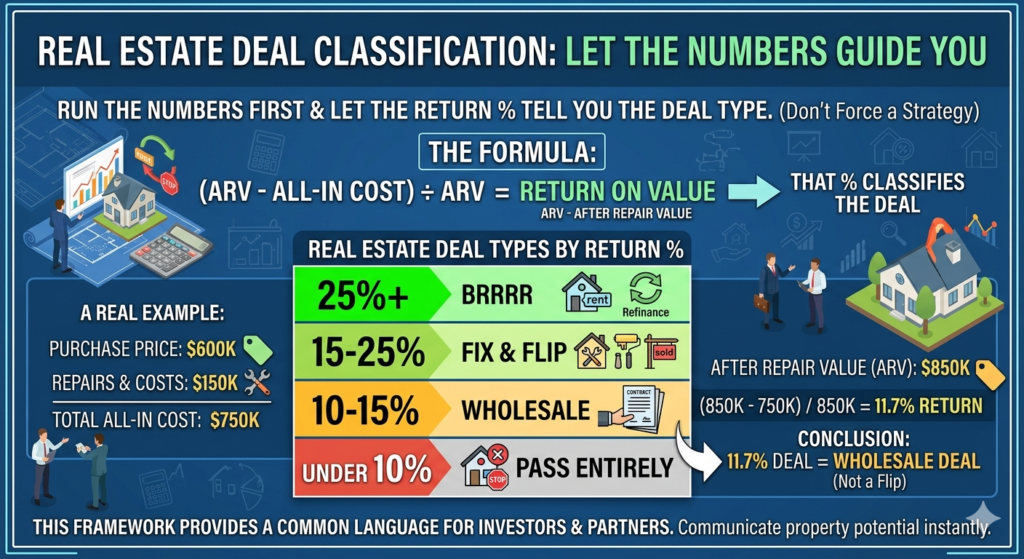

Once you have those two numbers, the real estate deal analysis formula is straightforward:

(ARV – All-in Cost) ÷ ARV = Return on Value

That percentage tells you exactly what kind of deal you’re looking at.

The Real Estate Deal Analysis Classification Framework

25%+ → BRRRR Deal Best case scenario. At this return level, the deal has enough margin to buy, rehab, rent, refinance, and repeat — pulling your capital back out while keeping the asset. These deals are hard to find, but when the numbers hit 25% or above, BRRRR is the move.

15% to 25% → Fix & Flip Deal Standard flip territory. There’s enough margin to cover purchase, rehab, holding costs, selling costs, and still walk away with meaningful profit. If you’re below 15%, the margin gets uncomfortably thin once real-world costs stack up.

10% to 15% → Wholesale Deal At this return level, the numbers don’t work for a flip or BRRRR — but there might still be a deal here for someone else. A wholesaler’s job is to find properties with potential and assign the contract to an investor who can make the numbers work. If your real estate deal analysis lands in this range, wholesale it — don’t hold it yourself.

Under 10% → Pass List it with a realtor or walk away entirely. There’s not enough margin to absorb the inevitable surprises that come with any renovation project.

A Real Example of Real Estate Deal Analysis in Action

The father walked his son through a deal he’d been offered:

| Purchase Price | $600,000 |

| Repair Costs | $150,000 |

| ARV | $850,000 |

| All-in Cost | $750,000 |

| Profit | $100,000 |

| Return | 11.7% |

Result: Wholesale deal. Not a flip, not a BRRRR — the margin isn’t there for either. But there’s potentially something for a wholesaler who can move it to the right buyer.

The math made the decision. No guessing, no gut feeling — just numbers plugged into a formula.

Why This Real Estate Deal Analysis Framework Actually Helps

This approach removes the backwards thinking most beginners do. You run the numbers with no agenda, and the numbers tell you what the deal is — or isn’t. If it doesn’t hit 10%, no amount of optimism changes that. If it hits 25%, you know you’ve found something worth pursuing hard.

It also gives you a clean way to communicate deals to lenders, partners, or wholesalers. Instead of saying “I think this could be a flip,” you can say “this is an 11.7% deal — wholesale territory.” That’s a language experienced investors understand immediately.

According to BiggerPockets, the most common mistake new investors make is deciding on a strategy before running the numbers — then reverse-engineering the analysis to justify the decision they already made. This framework prevents exactly that.

How I’m Using This Real Estate Deal Analysis Framework in Philadelphia

I’m getting back into flipping and actively analyzing deals right now. Before I had a framework like this, I’d look at a property, get excited about the potential, and sometimes struggle to articulate clearly why the numbers did or didn’t work.

Now the process is cleaner. Pull the ARV from comps. Estimate the all-in cost honestly — not optimistically. Run the formula. See where it lands.

If it’s under 10%, I move on without guilt. If it’s in flip territory, I dig deeper. If it ever hits 25% — well, that’s when things get interesting.

Use the Deal Type Classifier to run your own real estate deal analysis before you make any offer — plug in your ARV and all-in cost and it tells you exactly what kind of deal you’re looking at.

Not financial advice — just someone doing a lot of research and asking a lot of questions.