Flip financing strategy is what separates investors doing 2 flips a year from investors doing 20. When I first started studying real estate, I thought the goal was obvious: find a deal, make as much money as possible on that deal, repeat.

Then I started paying attention to what experienced flippers actually do. And it broke my brain a little.

The best investors — the ones doing 20, 30, 50 flips a year — are often making less per deal than a beginner who carefully squeezes every dollar out of one property. And they’re building wealth dramatically faster.

Here’s why.

The One-Deal-At-A-Time Trap

Most people getting into house flipping think about it like this: find a distressed property, put in $40,000 of repairs, sell it for $60,000 more than you paid, pocket the difference.

That’s a legitimate strategy. But it has a hard ceiling.

If you’re tying up $50,000 of your own cash in a single deal for 9 months, that money is locked. It can’t work anywhere else. You’re a one-project-at-a-time operation, and your income is limited by how many deals you can physically fund and manage sequentially.

The investors who break that ceiling use a completely different flip financing strategy.

100% Financing: The Flip Financing Strategy That Changes the Math

There are lenders who will finance 100% of a fix and flip deal — the purchase price plus the repair costs — with no money down from the investor.

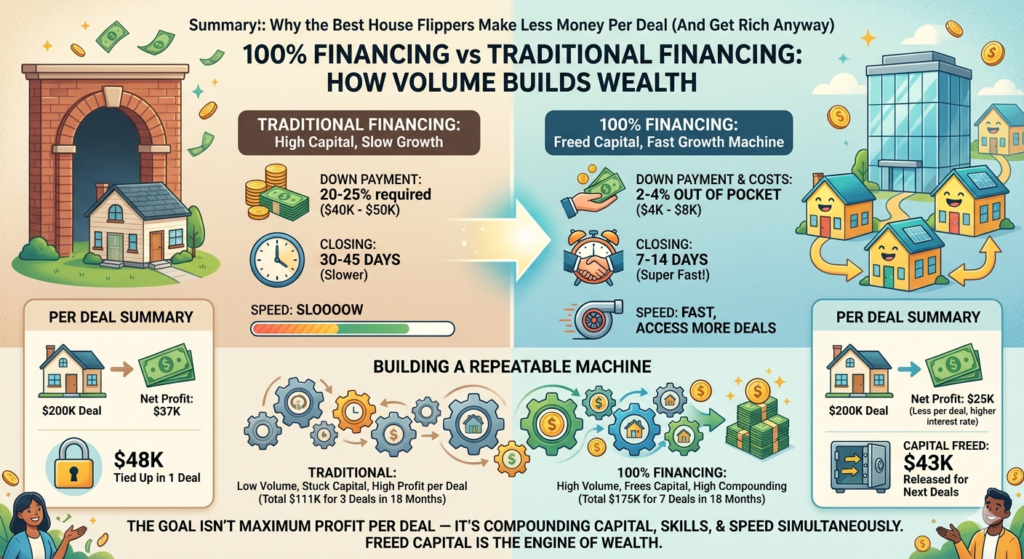

Not zero costs. You’ll still pay closing costs, typically 2–4% of the purchase price. On a $200,000 property, that’s $4,000–$8,000 out of pocket. Compare that to the $40,000–$50,000 down payment a traditional hard money lender requires on the same deal.

The catch: the interest rate is higher. Where a standard hard money loan might run 10–12% with 2–3 points, a 100% financing flip financing strategy might come in at 13–15% with 3–5 points. The lender is taking on more risk, and they price that in.

So your profit per deal goes down. Sometimes significantly.

The Math That Makes This Flip Financing Strategy Work Anyway

The deal: $200,000 purchase price, $40,000 in repairs, $300,000 ARV, 9-month hold.

Traditional hard money (80% LTV):

- Your cash in: ~$48,000

- Interest + points: ~$23,000

- Estimated net profit: ~$37,000

- Return on your $48K: about 77%

100% financing flip financing strategy:

- Your cash in: ~$5,000 (closing costs only)

- Interest + points: ~$35,000

- Estimated net profit: ~$25,000

- Return on your $5K: about 500%

Yes, you made $12,000 less on the deal.

But here’s the question that matters: what did you do with the $43,000 you didn’t tie up?

If that capital is sitting in a savings account, 100% financing just cost you $12,000. But if you put that $43,000 into a second deal running simultaneously — and made even a modest $20,000 on that one — you’ve now made $45,000 total instead of $37,000. With less capital at risk.

Not less money per deal. More deals per dollar. That’s the flip financing strategy.

Speed Is the Other Half of the Equation

Lenders who specialize in 100% financing are typically moving fast — 7 to 14 days to fund. In a competitive market, the ability to close in two weeks changes what deals you can even access.

Sellers of distressed properties — estate sales, tired landlords, someone facing foreclosure — often want out fast. A buyer who can close in 10 days beats a buyer with a higher offer who needs 45 days to sort out financing.

Speed is a negotiating tool. And it’s a competitive advantage that most beginning investors don’t have.

What This Flip Financing Strategy Looks Like at Scale

An investor doing 2 flips a year with traditional hard money, netting $35,000 each: $70,000 in annual profit, with $50,000+ of capital tied up at any given time.

An investor using 100% financing to run 6 flips a year simultaneously, netting $22,000 each: $132,000 in annual profit, with $30,000 or less of their own capital in play.

The second investor is making nearly twice the money with less capital at risk. They’re also building relationships with lenders, contractors, and buyers at three times the speed.

Compounding doesn’t just apply to interest. It applies to skills, networks, and reputation too.

According to BiggerPockets, volume-based flipping with higher-rate financing consistently outperforms low-volume flipping with cheaper capital — because the velocity of deals compounds the learning curve and relationship-building as much as the financial returns.

The Honest Tradeoffs of This Flip Financing Strategy

100% financing is not free money. The higher rates mean you need deals with real margin — properties where the ARV genuinely supports the numbers after all costs. A thin deal with traditional financing becomes a losing deal with 100% financing.

You also need to vet lenders carefully. Terms vary enormously. Some have prepayment penalties, draw structures that create cash flow problems mid-renovation, or fees buried in the fine print.

And the “close in 7 days” promise only works if your deal analysis is solid going in. Speed is an advantage when you know what you’re doing. It’s a liability when you’re still learning.

This flip financing strategy makes the most sense for investors who have already done a few deals, have a reliable contractor, and have enough cash reserves to handle surprises.

Where I’m Landing With This

The more I study how serious investors actually operate, the more I realize the goal isn’t to maximize profit on any single deal. The goal is to build a machine that generates deals, executes consistently, and compounds over time.

The right flip financing strategy is one tool in that machine. Used correctly — on the right deals, with the right lenders, with enough experience behind you — it’s the difference between doing 2 flips a year and doing 8.

That math adds up fast.

Use the Hard Money Loan Calculator to model both financing scenarios on your next deal — traditional hard money vs 100% financing — and see which flip financing strategy makes sense for your specific situation.

Not financial advice — just someone doing a lot of research and asking a lot of questions.