BRRRR apartment investing is where the math starts to sound too good to be true — but it’s actually just a refinance strategy. What if you could own an asset with none of your own money still in the deal?

That’s what people mean when they say “infinite return.” Let me walk through how it actually works.

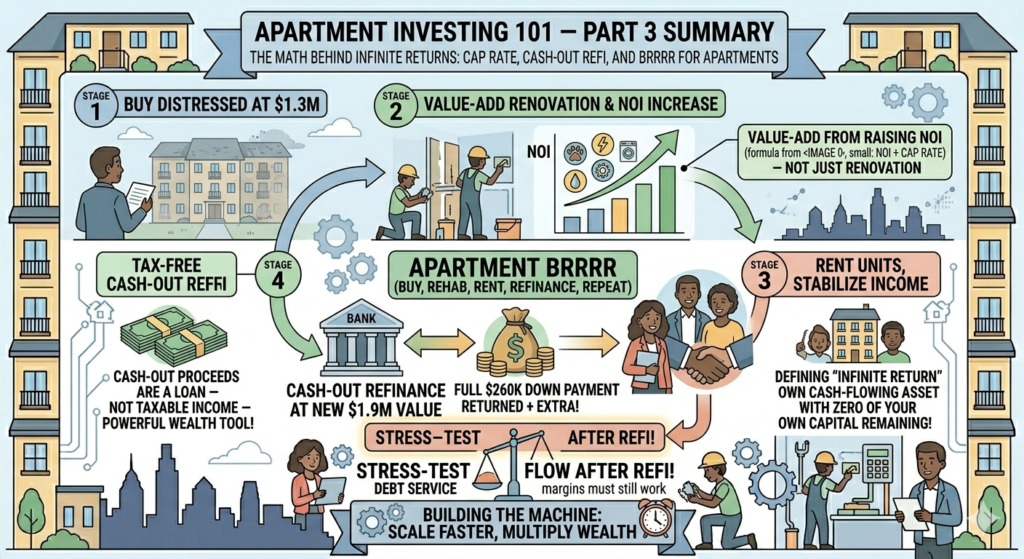

BRRRR Apartment Investing: How It’s Different From Single-Family

You’ve probably heard of BRRRR for single-family homes — Buy, Rehab, Rent, Refinance, Repeat. The same framework applies to multifamily, but the value-add piece works differently.

With a house, you’re rehabbing to match comps. With BRRRR apartment investing, you’re rehabbing and optimizing operations to raise NOI. Both matter — and together, they create a bigger value jump than either would alone.

The Numbers: A Real BRRRR Apartment Investing Example

You find a 16-unit building listed at $1,300,000. It’s been mismanaged — deferred maintenance, below-market rents, no pet fees, owner paying all utilities.

At acquisition:

- Current NOI: $87,750/year

- Cap rate in the area: 6.75%

- Implied value: $87,750 ÷ 0.0675 = $1,300,000 ✓

You put down 20% plus closing costs — roughly $260,000 out of pocket.

Year One: The BRRRR Apartment Investing Value-Add Work

Over the next 12 months you fix deferred maintenance, bring rents to market rate gradually, add pet fees, implement RUBS, enforce a late fee policy, and renegotiate vendor contracts.

New NOI: $128,250/year

New value: $128,250 ÷ 0.0675 = $1,900,000

You just created $600,000 in equity through operations. Not luck. Not a hot market. Math.

The Refinance: Getting Your Money Back in BRRRR Apartment Investing

Now you refinance based on the new appraised value of $1,900,000.

Most commercial lenders will lend up to 75% LTV on a stabilized multifamily:

$1,900,000 × 0.75 = $1,425,000 loan

Your original loan was roughly $1,040,000 (80% of $1,300,000).

Cash out: $1,425,000 − $1,040,000 = $385,000 back in your pocket

You put in $260,000. You pulled out $385,000. Your original capital is fully returned — plus some.

And here’s the key: that $385,000 is a loan, not income. No tax event.

What “Infinite Return” Actually Means in BRRRR Apartment Investing

Return on investment is calculated as: ROI = Annual Profit ÷ Capital Invested

After the refinance, your capital invested is effectively zero — you pulled it all back out. But you still own the building. The tenants are still paying down your mortgage every month. The cash flow is still coming in.

Any return on zero investment is mathematically infinite.

Is this realistic for everyone on day one? No. You need the deal, the financing, the operational skills, and ideally some experience first. But the math is real. The strategy is real. Understanding it changes how you look at every property you evaluate from here on out.

The Part Nobody Talks About in BRRRR Apartment Investing

After you cash out refi, your new loan is bigger. Which means your monthly mortgage payment is higher. Which means your cash flow drops.

You need to make sure the property still cash flows after the refinance. This is where a lot of people get caught — they execute the BRRRR perfectly but end up with a building that barely breaks even because the new debt service ate everything.

Run the numbers before you buy. Know what NOI you need to hit to still cash flow at 75% LTV on the post-refi value. That’s your target from day one in BRRRR apartment investing.

According to BiggerPockets, the most common mistake in BRRRR apartment investing is underestimating the post-refinance debt service — investors who don’t model the new payment before acquisition often find themselves trapped in a break-even deal with no path to the next acquisition.

Putting the Whole BRRRR Apartment Investing Framework Together

Part 1: Apartments are valued by income, not comps. NOI ÷ Cap Rate = Value. Every $1 in annual NOI = ~$14.80 in value at a 6.75% cap rate.

Part 2: You control NOI through income diversification (pet fees, RUBS, late fees) and expense reduction (vendor renegotiation, in-house maintenance). Small changes compound into serious equity.

Part 3: Once you’ve raised NOI and increased the appraised value, a cash-out refinance lets you pull your original capital back out — tax-free — and redeploy it into the next deal. That’s how the BRRRR apartment investing cycle repeats.

This is the framework behind every serious multifamily investor’s portfolio growth. It’s not magic. It’s not a guru secret. It’s just understanding how commercial real estate is valued — and using that knowledge intentionally.

Use the BRRRR Calculator to model your own BRRRR apartment investing deal — plug in acquisition price, value-add NOI improvement, cap rate, and refinance LTV to see exactly when and how much capital you can pull back out.

Not financial advice — just someone doing a lot of research and asking a lot of questions.