Multi unit property financing is the question I kept coming back to after writing about house hacking. The strategy makes sense — buy a duplex or triplex, live in one unit, let tenants cover most of your mortgage. But where does the down payment come from?

Even 3.5% FHA down payment on a $350,000 duplex is $12,250. Plus closing costs. You’re looking at $20,000+ out of pocket before you even move in. For a lot of people — myself included — that’s not nothing.

So I kept digging. Here are two strategies that actually move the needle on the cash-to-close problem.

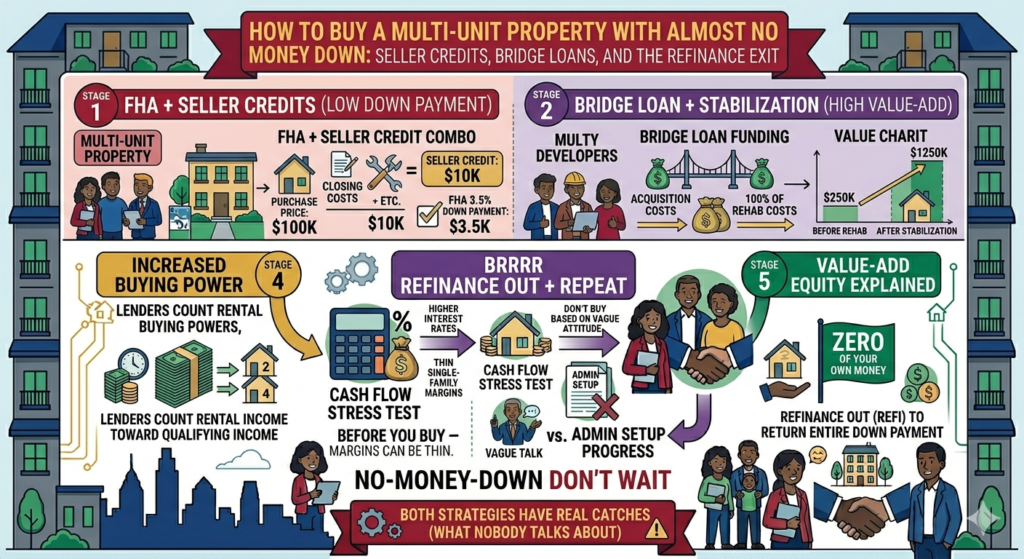

Strategy 1: FHA + Seller Credit — The “Almost Zero” Multi Unit Property Financing Combo

Most people know about FHA loans. 3.5% down, lower credit requirements, government-backed. What fewer people talk about is pairing FHA with a seller credit for multi unit property financing.

When you make an offer, you can negotiate for the seller to contribute toward your closing costs — called a seller concession. On an FHA loan, sellers can contribute up to 6% of the purchase price toward closing costs.

The math on a $350,000 duplex:

| FHA down payment (3.5%) | $12,250 |

| Closing costs (estimated 3–4%) | ~$12,000 |

| Seller credit (6%) | $21,000 |

If you negotiate a full 6% seller credit, the seller covers your closing costs entirely — and you’re left only covering the down payment.

Some buyers negotiate the seller credit and offer slightly above asking price to offset it for the seller:

- List price: $350,000

- Your offer: $360,000 with $21,600 seller credit

- Seller nets roughly the same

- Your closing costs: covered

- Out of pocket: just the $12,600 down payment

Is this always possible? No. The property has to appraise at or above your offer price — and FHA appraisals are strict. In a slower market or with a motivated seller, this is a legitimate multi unit property financing tool.

The catch: you still need the down payment. This strategy covers closing costs, not the 3.5%. For true zero out of pocket, you’d need to combine this with gift funds from a family member (FHA allows this) or a down payment assistance program — and Philadelphia has several worth looking at.

Why Multi Unit Property Financing Changes Your Loan Qualification

Before we get to bridge loans, there’s something about multifamily financing most beginners don’t realize — and it’s a huge advantage.

With a single-family home, the bank qualifies you based on your personal income alone. With a 2–4 unit property, lenders can count projected rental income as part of your qualifying income.

Example:

- Your personal income qualifies you for a $250,000 loan

- You’re buying a triplex where two units rent for $1,200/month each

- Lender counts 75% of that rental income: $1,800/month added to qualifying income

- Suddenly you qualify for a $400,000–$500,000 loan

Same person. Same job. Completely different purchasing power — just because the property generates income. This is one of the most underappreciated advantages in multi unit property financing.

Strategy 2: Bridge Loan → Stabilize → Refinance Out

This one is for investors who aren’t planning to live in the property. Pure investment play.

A bridge loan is a short-term loan — typically 12 to 24 months — designed to bridge the gap between acquisition and long-term financing. Faster and more flexible than conventional multi unit property financing, but it costs more.

Step 1: Acquire with bridge financing You find a 4-unit building that’s mismanaged — below-market rents, deferred maintenance, partially vacant. Bridge lender covers 85–90% of purchase price plus 100% of approved rehab costs. Your out of pocket: 10–15% down plus fees.

Step 2: Execute the value-add Fix deferred maintenance. Renovate units as they turn over. Bring rents to market rate. Get to full or near-full occupancy.

Step 3: Refinance into permanent financing Property is now stabilized — fully rented, market rents, clean financials. You refinance into a DSCR loan at 75–80% LTV based on the new appraised value. Cash-out proceeds pay off the bridge loan.

| At Purchase | After Stabilization | |

|---|---|---|

| Property value | $400,000 | $520,000 |

| NOI | $28,000/yr | $40,000/yr |

| Bridge loan balance | $360,000 | $360,000 |

| Refi at 75% LTV | — | $390,000 |

| Cash out after payoff | — | $30,000 |

| Your down payment in | $40,000 | Returned |

You put in $40,000. You pulled out $30,000 at refi. Net cost basis: $10,000 — for a building worth $520,000 generating $40,000 NOI annually.

The Catches Nobody Mentions About This Multi Unit Property Financing Strategy

Bridge loans are expensive. Interest rates typically run 9–12%. On a $360,000 loan, that’s $32,000–$43,000 in annual interest. If your stabilization takes longer than expected, those carrying costs eat your profit fast.

The refi only works if the value actually goes up. You’re betting on your ability to execute the value-add. If rents don’t move or rehab goes over budget, the appraisal might not support the numbers you need.

Lenders want experience. The 10% down bridge loan structure is generally available to investors with a track record. First-timers often face higher requirements or get turned down entirely.

According to the Mortgage Bankers Association, bridge loan volume for multifamily value-add deals has increased significantly over the past three years as more investors use the stabilize-and-refinance exit strategy to recycle capital into new acquisitions.

Which Multi Unit Property Financing Strategy Is Right for You?

| FHA + Seller Credit | Bridge Loan + Refi | |

|---|---|---|

| Must live there? | Yes (1 year minimum) | No |

| Down payment | 3.5% (closing costs covered) | 10–15% |

| Best for | First-time buyers, house hackers | Experienced investors |

| Biggest risk | Rent doesn’t cover mortgage | Carrying costs + execution risk |

Neither strategy is a shortcut. Both require the right deal, the right financing relationship, and a clear exit before you enter.

Use the Multi-Unit Cash Flow Calculator to model both multi unit property financing scenarios on a specific Philadelphia deal before you commit to either strategy.

Not financial advice — just someone doing a lot of research and asking a lot of questions.