Real estate depreciation tax benefits are why serious investors don’t just buy rentals for cash flow. I used to think people bought rental properties for the monthly income. But the more I study how wealthy investors actually think about real estate, the more I realize: for a lot of them, the cash flow is almost secondary. The real prize is what happens at tax time.

Let me break this down the way I wish someone had explained it to me.

What Is Real Estate Depreciation Tax Deduction?

The IRS assumes buildings wear out over time. So they allow real estate investors to deduct a portion of the building’s value every year — even if the property is actually appreciating in the real world.

For residential rental properties, you depreciate the building (not the land) over 27.5 years.

Simple example:

- You buy a duplex for $300,000

- Land value: $50,000

- Building value: $250,000

- Annual real estate depreciation tax deduction: $250,000 ÷ 27.5 = $9,090/year

That $9,090 comes off your taxable income every single year — without spending a dime. The property might be going up in value. You might be cash flowing. And you’re still getting a paper loss that reduces your tax bill.

This is why real estate is one of the few investments where you can make money and show a loss at the same time.

Now Scale the Real Estate Depreciation Tax Math Up

A $15 million apartment complex has a building value of maybe $12 million after land. Standard real estate depreciation tax deduction over 27.5 years:

$12,000,000 ÷ 27.5 = $436,000/year in deductions

For someone in a 37% tax bracket, that’s roughly $161,000 in actual tax savings every year — just from depreciation alone.

No wonder wealthy investors love this asset class.

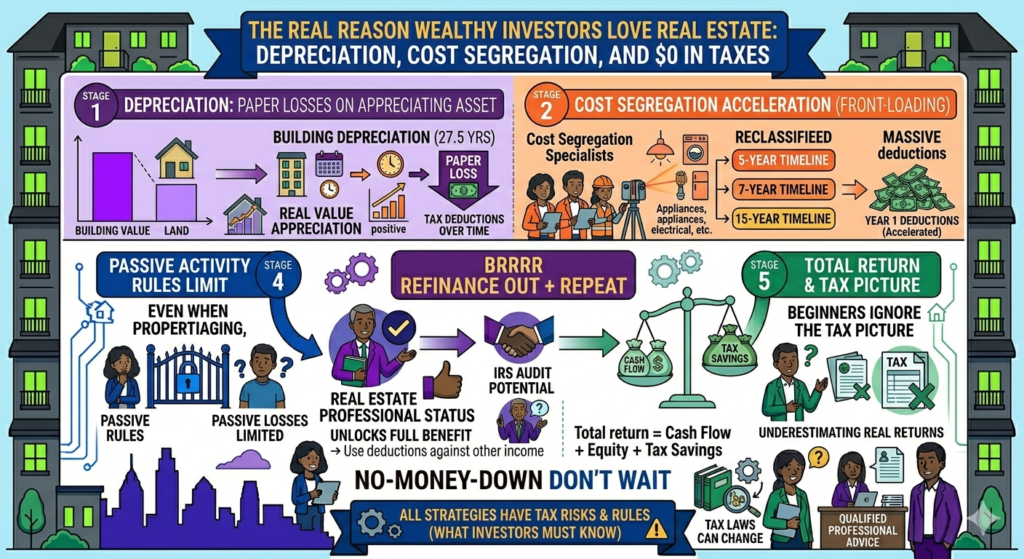

Cost Segregation: Accelerating the Real Estate Depreciation Tax Timeline

Standard depreciation is good. Cost segregation is better.

A cost segregation study is an engineering analysis that breaks a property down into individual components and reclassifies certain parts for faster depreciation:

- Appliances, carpeting, fixtures → 5 years

- Land improvements (parking lots, landscaping, fencing) → 15 years

- Certain building components → 7 years

By front-loading real estate depreciation tax deductions into the early years of ownership, investors take massive write-offs right after acquisition — instead of spreading them evenly over 27.5 years.

On a $15 million acquisition, a cost segregation study might identify $4–5 million in assets eligible for accelerated depreciation. In the first year alone.

Bonus Depreciation: The Accelerator

For several years, the IRS allowed 100% bonus depreciation — write off the entire cost of eligible short-life assets in year one.

As of 2026, bonus depreciation has stepped down to 40% (phasing out since 2023). Still significant — but verify current rules with a CPA since this changes frequently.

Between standard real estate depreciation tax deductions, cost segregation, and bonus depreciation, a large real estate acquisition can generate paper losses that dwarf the actual cash invested — at least in the early years.

What Real Estate Depreciation Tax Benefits Look Like in Real Life

You’re a high-income professional making $500,000 a year, writing a massive check to the IRS every April.

You buy a $3 million apartment building. Cost segregation identifies $800,000 in year-one accelerated depreciation. At 40% bonus depreciation, you take $320,000 as an immediate deduction. Plus standard depreciation on the rest.

Taxable income drops significantly. The tax savings alone — potentially $100,000+ in year one — effectively subsidize a huge chunk of your down payment.

This is why wealthy investors aren’t just buying real estate for cash flow. They’re buying it because the tax code is genuinely structured to reward real property ownership at scale.

The Catch: Passive Activity Rules

Rental income and losses are classified as passive activity. Passive losses can generally only offset passive income — not your W-2 salary or business income.

Two key exceptions:

Real Estate Professional status — If you spend more than 750 hours per year in real estate activities and it’s your primary occupation, your rental losses become active and can offset any income. This is how full-time investors eliminate their tax bill entirely.

$25,000 allowance — If your income is under $100,000, you can deduct up to $25,000 in rental losses against ordinary income. This phases out completely at $150,000.

For most beginners, the full real estate depreciation tax benefit picture doesn’t unlock until real estate becomes your primary focus — or until you have enough passive income from other investments to offset the passive losses.

According to IRS.gov, the passive activity loss rules under Section 469 are one of the most misunderstood areas of real estate taxation — and one of the most important to understand before assuming depreciation will offset your W-2 income.

Why Real Estate Depreciation Tax Benefits Change How You Evaluate Deals

A property that cash flows $500/month — $6,000/year — might look modest. But if it’s also generating $15,000 in annual real estate depreciation tax deductions and you’re in a 35% tax bracket, that’s $5,250 in actual tax savings on top of the cash flow.

Real return: $6,000 + $5,250 = $11,250/year — almost double what the cash flow number suggests.

This is why comparing real estate returns to stock market returns using cash flow alone is apples-to-oranges. The tax advantage is a real return. It just shows up in what you don’t send to the IRS.

What Beginners Should Take Away

You don’t need a $15 million apartment complex to benefit from real estate depreciation tax deductions. Depreciation works on a $300,000 duplex too. The math scales down, but the principle is the same.

What you do need: a CPA who understands real estate investing (not just taxes in general), to run the numbers including depreciation when evaluating deals, and to understand whether you qualify for passive loss deductions given your income level.

Use the Depreciation Calculator to model your own real estate depreciation tax scenario — plug in purchase price, land value, and building value to see your annual deduction before you talk to a CPA.

Not financial advice or tax advice — just someone doing a lot of research and asking a lot of questions. Tax rules change — talk to a CPA before making any decisions based on this.