SBA 7a loan real estate financing might be the most powerful commercial real estate tool most people have never heard of. I’ll lead with something most bloggers wouldn’t admit: I looked into this loan and immediately realized I don’t qualify.

My LLC has been registered for nine years. Good standing, D&B number, solid credit history. On paper it looks like a real business.

But it’s a paper company. No revenue, no employees, no active operations. And the SBA 7a loan real estate requirement is an actual operating business — one that generates income and will physically occupy the building you’re buying.

So why am I writing about it? Because for people who do have a real operating business, this changes everything.

What Is the SBA 7a Loan Real Estate Program?

The SBA 7a is a government-backed small business loan administered through approved lenders — banks, credit unions, and specialty SBA lenders. The SBA guarantees a portion of the loan, which reduces the lender’s risk and allows them to offer better terms than a conventional commercial mortgage.

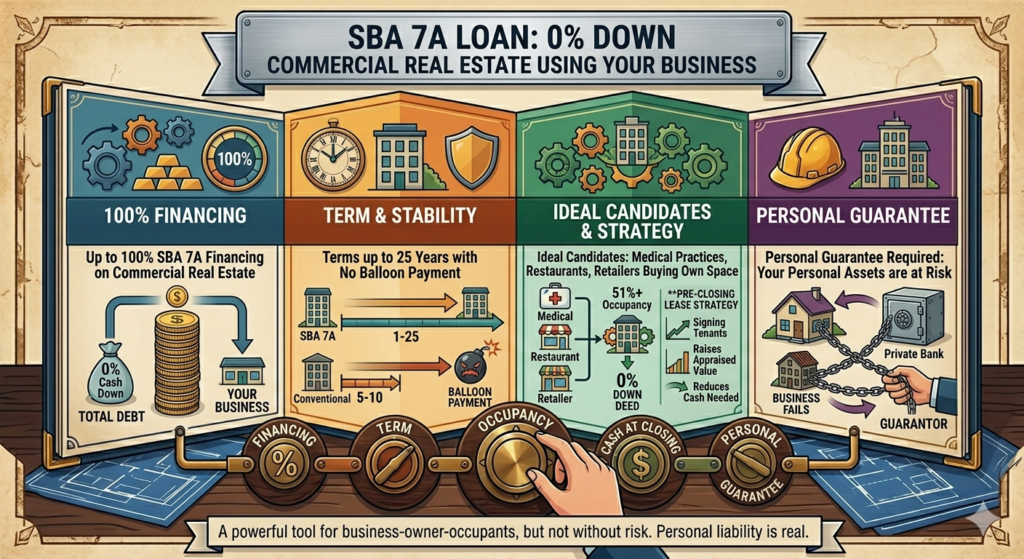

The headline feature: you can borrow up to 100% of the purchase price with no down payment required.

Zero down on a commercial property — as long as you meet the criteria.

The 51% Rule: Who Actually Qualifies for SBA 7a Loan Real Estate

Here’s the key requirement that makes or breaks SBA 7a loan real estate eligibility.

Your business must occupy at least 51% of the building you’re purchasing. The program is designed for owner-occupied commercial real estate — not pure investment properties. You’re buying a building to run your business in, not to rent out entirely to other tenants.

This opens the door for:

- A medical practice buying its own office building

- A restaurant buying the space it currently rents

- A contractor buying a building with office space and a warehouse

- A daycare buying its facility

The remaining 49% of the building can be rented to other tenants — which actually helps your cash flow significantly.

What doesn’t qualify:

- Holding companies with no active operations

- Pure real estate investment LLCs

- Businesses that don’t need physical space

- Properties where the owner won’t actually occupy the majority of the space

The SBA 7a Loan Real Estate Terms

Loan amount: Up to $5 million

Down payment: As low as 0% — though 10% is more common for standard deals. True 100% financing typically requires additional collateral or a very strong business profile.

Loan term: Up to 25 years for real estate — much longer than conventional commercial loans which are typically 5–10 year balloons.

Interest rate: Variable, tied to prime rate plus a spread. Generally more favorable than conventional commercial rates.

Personal guarantee: Required. The SBA wants a personal guarantee from anyone owning 20%+ of the business. This is the real risk — if the business fails and the loan defaults, your personal assets are on the line.

Why the 25-Year Term Changes the SBA 7a Loan Real Estate Math

Most commercial loans are structured as 5 or 10-year balloon loans — the full balance comes due at the end of that term, requiring you to refinance or sell. That creates real risk if market conditions or your financial situation changes.

SBA 7a loan real estate financing goes up to 25 years with no balloon payment. You’re amortizing the full loan over the life of the note — like a residential mortgage.

For a small business owner, that stability is huge. Your monthly payment is predictable. You’re not scrambling to refinance every five years. And you’re building equity in a property you control instead of paying rent to someone else indefinitely.

The “Leasing Before Closing” Play With SBA 7a Loan Real Estate

If you’re buying a partially vacant commercial building, you don’t have to wait until after closing to fill it. You can start leasing the vacant units before you close.

Commercial properties are valued based on income. A building with signed leases is worth more than the same building with vacancies — even if the leases haven’t started yet.

By securing tenants before closing, you increase the appraised value:

- Get the property under contract with a 60–90 day due diligence period

- During that window, market the vacant units and sign leases

- Present those signed leases to your lender at closing

- Lender appraises based on the new income picture

- LTV improves, your cash-to-close drops

The leases have to be real, the tenants have to be creditworthy, and the lender has to accept them. But it’s a legitimate strategy sophisticated commercial buyers use regularly alongside SBA 7a loan real estate financing.

According to the U.S. Small Business Administration, the SBA 7a loan is the agency’s most widely used loan program — with over $27 billion in loans guaranteed annually — making it one of the most significant sources of small business capital in the country.

Who the SBA 7a Loan Real Estate Program Is Really For

If you have an active business that generates real revenue, needs physical space to operate, and is looking to stop paying rent and start building equity — the SBA 7a loan real estate program deserves serious attention.

You’re essentially converting a rent expense into a mortgage payment — on a building you own — with the government backing the loan. The math often works out in your favor even if the mortgage payment is slightly higher than your current rent. Because rent is gone forever. Mortgage payments build equity.

My Situation — And Maybe Yours

I can’t use this. My LLC is a paper company — no active revenue, no employees, no physical operations. But if pinotnoirmom or any other venture I’m building ever generates real revenue and needs real space — this is the first loan I’m looking at.

If you’re reading this with an actual operating business, go talk to an SBA-approved lender. Not a general bank — find someone who specifically does SBA lending. The process typically takes 60–90 days and the requirements are nuanced, but the terms can be genuinely life-changing for the right business.

Use the Mortgage Affordability Calculator to model what an SBA 7a loan real estate payment would look like compared to your current rent — before you sit down with a lender.

Not financial advice — just someone doing a lot of research and asking a lot of questions. SBA loan terms change — verify current requirements with an approved SBA lender.