Assumable mortgage loan strategy is one of the most underutilized opportunities in today’s market — and most buyers don’t even know it exists. But before we get there, let’s talk about why there’s nothing good available in the first place.

If you’ve been watching the housing market and wondering why inventory is historically low — you’re not imagining it. And the reason has nothing to do with a housing crash or bubble.

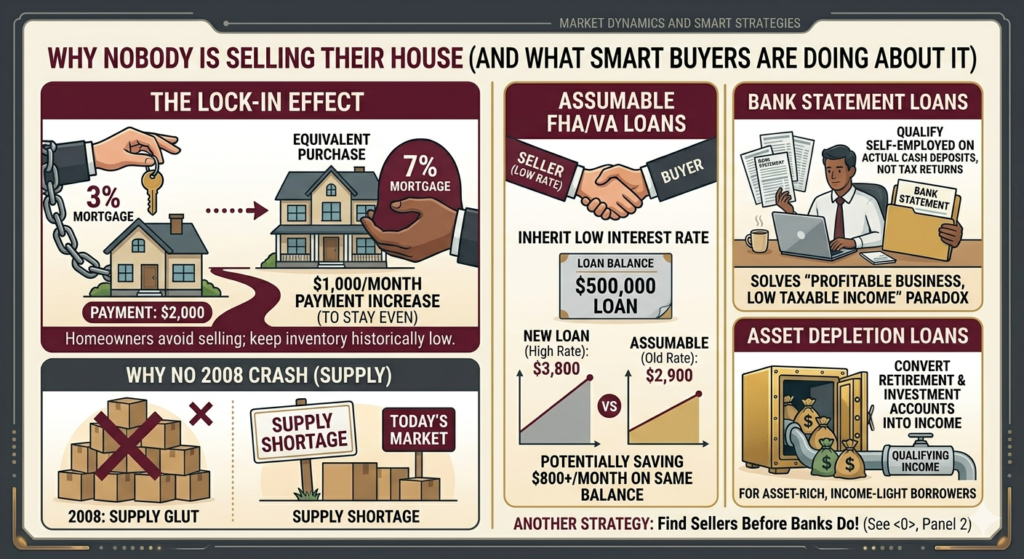

Nobody wants to give up their mortgage.

The Lock-In Effect: Why the Assumable Mortgage Loan Opportunity Exists

During the pandemic, mortgage rates dropped to historic lows. Millions of Americans locked in 30-year fixed rates at 2.5%, 3%, 3.5%.

Here’s the math that explains why those people aren’t going anywhere.

$400,000 home at 3% interest: Monthly payment ~$1,686

$400,000 home at 7% interest: Monthly payment ~$2,661

That’s nearly $1,000 more per month. For the same house. Forever.

So when someone with a 3% mortgage thinks about selling — even a lateral move, same price range — they’re looking at adding $1,000/month to their housing cost. Most people don’t do that voluntarily.

The result: people are staying put. Fewer people moving means fewer homes for sale, inventory stays low, and prices don’t drop even when rates are high. This is why 2024–2026 feels nothing like 2008.

“Just Wait for the Crash” Is Probably the Wrong Strategy

For prices to drop significantly, supply needs to increase dramatically. And supply only increases when people sell. And people only sell when they’re willing to give up their 3% mortgage — which most aren’t.

The U.S. also hasn’t built enough housing to meet demand for over a decade. That structural deficit doesn’t resolve quickly.

Waiting for a 2008-style crash in a market with fundamentally different supply dynamics might mean waiting a very long time — while paying rent, missing appreciation, and watching the window close on assumable mortgage loan opportunities.

Assumable Mortgage Loan: The Strategy Most Buyers Don’t Know Exists

Here’s one of the most underutilized opportunities in the current market.

Certain government-backed loans — FHA loans and VA loans specifically — are assumable. That means when you buy a home from someone who has one of these loans, you can take over their existing mortgage at their existing interest rate.

If a seller has an FHA loan at 3.25% and you assume it, you’re now paying 3.25% — not the current market rate of 7%+.

On a $350,000 remaining loan balance, that difference is roughly $800/month. Every month. For the life of the loan.

How the assumable mortgage loan process works:

- The seller must have an FHA or VA loan (conventional loans are generally not assumable)

- You apply to assume the loan through the seller’s lender

- The lender verifies your creditworthiness

- You pay the difference between the purchase price and the remaining loan balance in cash or through a second loan

The catch: If the home is worth $450,000 and the remaining FHA balance is $280,000, you need $170,000 to cover the gap. That’s the main barrier — and it’s why assumable mortgage loans work best when the seller hasn’t built up too much equity yet, or when you have significant capital available.

Still, in a market where locking in a 3% rate could save you $800/month, it’s worth asking every seller’s agent whether the existing loan is assumable.

Bank Statement Loans: For People Whose Tax Returns Don’t Tell the Full Story

I’ll get personal here for a second.

My LLC has been registered for nine years. But like a lot of self-employed people and small business owners, my tax returns show minimal income — because that’s how small business accounting works. You deduct everything you legally can, which reduces your taxable income, which also reduces what a conventional lender sees as your qualifying income.

Bank statement loans exist specifically for this situation. Instead of using tax returns to verify income, the lender looks at 12–24 months of bank statements — actual cash flowing into your accounts. If your business deposits $15,000/month consistently, a bank statement lender counts that as income.

Who this is for: Self-employed business owners, freelancers, independent contractors, anyone whose tax returns significantly understate their actual cash flow.

The tradeoffs: Slightly higher interest rates (0.5–1% higher than conventional) and may require larger down payments (10–20%). But for someone who genuinely earns solid income but can’t prove it on a tax return, it’s often the only path.

Asset Depletion Loans: For the Asset-Rich With Limited Income

Similar principle, different application.

If you’re retired — or simply have significant assets but limited current income — some lenders will calculate a hypothetical monthly income based on your investable assets.

Common formula: take your total eligible assets, divide by 360 months, and treat the result as monthly income for qualifying purposes.

Example: $800,000 in retirement assets ÷ 360 months = $2,222/month in “income” for qualifying purposes.

For someone who is genuinely financially secure but can’t show W-2 income, asset depletion loans open doors that conventional underwriting slams shut.

The Longer View on Housing

In 30 years, a $500,000 house today will probably be worth significantly more. That’s not a prediction — it’s a historical trend. Housing appreciates over long periods because land is finite and demand grows.

Waiting for the perfect moment to buy has a real cost. Every year of renting is a year of someone else’s mortgage getting paid instead of yours. Every year of appreciation is equity someone else is building.

None of this means buy something that doesn’t make financial sense. The numbers have to work. But “waiting for the crash” while paying rent isn’t a neutral position.

According to the Mortgage Bankers Association, assumable mortgage loan volume has increased significantly since 2022 as rate-locked sellers and rate-sensitive buyers discover the strategy — with FHA and VA assumption requests up substantially year over year.

Use the Mortgage Calculator to model the assumable mortgage loan math on any deal — plug in the seller’s existing rate vs today’s rate and see exactly what you’d save monthly before you make any offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions. Loan products and availability vary — talk to a licensed mortgage professional before making any decisions.