Real estate portfolio strategy isn’t just about buying properties — it’s about designing a system that survives whatever the market throws at it.

Most investors who get into real estate don’t fail in year one. They fail in year seven. Year ten. Year twelve. They buy a property, it works. They buy another, it works. Then something shifts. A market turns. A tenant stops paying. A roof fails on three properties at once.

And suddenly the portfolio that looked solid starts cracking. Not all at once — slowly. One problem leads to another. Cash reserves dry up. Properties get sold at the wrong time to cover emergencies.

This isn’t bad luck. It’s bad real estate portfolio strategy.

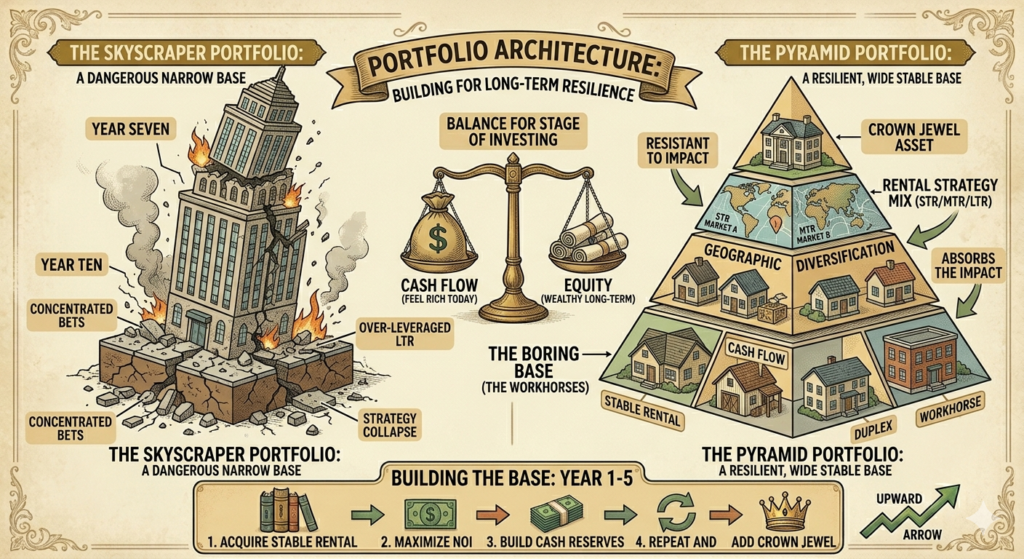

The Skyscraper Problem in Real Estate Portfolio Strategy

Imagine building a skyscraper. Tall, impressive, generating enormous returns from a small footprint. It looks great on paper.

But a skyscraper has a narrow base. One crack in the foundation and the whole structure is at risk. No redundancy. No backup. If the primary income source fails — the single market collapses, the anchor tenant leaves, the short-term rental regulations change overnight — there’s nothing holding it up.

A lot of real estate portfolios are built like skyscrapers. One strategy, one market, one property type. Everything concentrated. Everything dependent on conditions staying favorable.

When conditions change — and they always do — the skyscraper wobbles.

The Pyramid Alternative: The Right Real Estate Portfolio Strategy

The investors whose portfolios survive decade after decade tend to build differently.

Wide base first. Stable, boring, cash-flowing properties that generate reliable income regardless of market conditions. Duplexes. Affordable single-family rentals. Properties in secondary markets that don’t make headlines but pay rent every month.

Then, as the base strengthens and cash reserves accumulate, higher-risk higher-reward assets get added at the top. The vacation rental. The value-add commercial play. The development project.

The key insight of this real estate portfolio strategy: when the top-of-pyramid asset has a problem — and it will, eventually — the wide base absorbs the impact. One bad quarter on a vacation rental doesn’t threaten the whole portfolio when there are eight stable long-term rentals generating consistent cash flow underneath it.

Equity vs. Cash Flow: Your Real Estate Portfolio Strategy Needs Both

Cash flow is what makes you feel rich today. It’s the money left over after every expense is paid — mortgage, taxes, insurance, maintenance, management. It funds your next acquisition. But cash flow can disappear. A vacancy. A non-paying tenant. A regulation that changes the economics overnight. Cash flow is real and valuable — and it’s also fragile.

Equity is what makes you wealthy over time. The difference between what a property is worth and what you owe on it. It builds through appreciation, through principal paydown, and through value-add work. Equity doesn’t pay your bills today. But it’s what you’re still sitting on in thirty years when the mortgage is paid off.

The mistake: optimizing entirely for one at the expense of the other.

The real estate portfolio strategy that works: some properties optimized for cash flow (funding operations and life today), some optimized for equity growth (funding retirement and long-term wealth). The ratio depends on where you are in your investing life — earlier stage leans more equity, later stage leans more cash flow.

The “Sexy Deal” Trap in Real Estate Portfolio Strategy

Every investor has a version of this story.

They hear about someone making $8,000 a month from a single luxury vacation rental. They bypass the boring duplex they were going to buy and put everything into the high-end short-term rental instead.

For a while, it works brilliantly. Then the city passes new short-term rental regulations. Or a competitor opens nearby. Or a slow season hits harder than expected. Or all three at once.

And because they skipped the base-building phase of their real estate portfolio strategy, there’s nothing underneath to absorb the hit.

Start with the duplex. Build the foundation wide. Then, when the reserves are there and the cash flow is stable, add the crown jewel.

Geographic Diversification in Real Estate Portfolio Strategy

Markets move in cycles. Cities that were on fire three years ago are sitting on excess inventory today. Investors who concentrated everything in one hot market learned this the hard way.

The fix: own in more than one market, and make sure they don’t move in perfect correlation.

A real estate portfolio strategy that includes properties in a high-growth coastal market and properties in a stable Midwest market isn’t exciting. But when the coastal market corrects, the Midwest properties keep paying rent. The goal isn’t maximum return in any one market. It’s a portfolio that survives any market.

The Rental Strategy Mix in Your Real Estate Portfolio Strategy

Short-term rentals (STR): Highest income potential per night. Also highest management intensity, highest regulatory risk, and highest seasonality.

Medium-term rentals (MTR): Furnished rentals for 30–90 days — travel nurses, relocating professionals, corporate housing. More stable than STR, lower management burden.

Long-term rentals (LTR): Standard 12-month leases. Lowest income per unit, highest stability. The backbone of most real estate portfolio strategies.

A portfolio that mixes STR with LTR uses the stable long-term income to absorb the volatility of the short-term side. If you have a beach property that kills it June through August and struggles November through February — a couple of long-term rentals generating consistent monthly income keep your cash flow positive through the off-season.

The Chicken Leg Problem in Real Estate Portfolio Strategy

Some investors build a portfolio that looks impressive from certain angles — high-performing assets, great numbers in the good months, an exciting story to tell. But underneath, the foundation is weak. Thin cash reserves. No stable base of boring cash-flowing properties. Everything dependent on conditions staying favorable.

When something goes wrong — and in real estate, something always eventually goes wrong — there’s nothing to absorb it. The impressive top collapses because the legs underneath couldn’t hold the weight.

Big top, weak base. Chicken legs.

The investors whose portfolios are still standing after twenty years built it the other way. Wide, stable, sometimes boring base. Strong reserves. Diversification across markets and strategies. Then, on top of all that — the exciting stuff.

Architecture first. Excitement second.

According to BiggerPockets, the most common cause of real estate portfolio failure isn’t bad deals — it’s inadequate cash reserves and over-concentration in a single strategy or market that leaves investors unable to absorb the inevitable surprises that come with property ownership.

Use the Sell vs Keep Calculator to evaluate any property in your portfolio — or one you’re considering — against your overall real estate portfolio strategy before you make any acquisition or disposition decision.

Not financial advice — just someone doing a lot of research and asking a lot of questions.