I’ll be honest with you. I stumbled across a Philadelphia Sheriff Sale listing recently and I haven’t been able to stop thinking about it.

A 3-bedroom row home. Decent neighborhood. Listed at a price that made me do a double-take and check if I was reading it right.

That’s the thing about Sheriff Sales — the prices are genuinely eye-catching. And once you see one, it’s hard to look away.

But before I get too excited, I’ve been doing my homework. Because the gap between “amazing deal” and “expensive mistake” in Sheriff Sale investing is almost entirely determined by what you know going in.

Here’s everything I’ve learned.

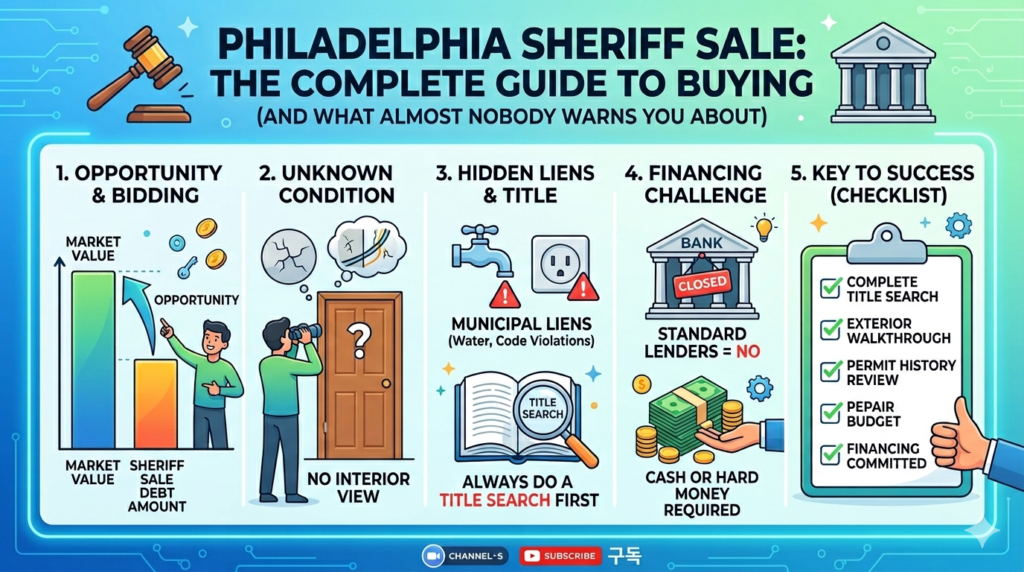

What Is a Philadelphia Sheriff Sale?

A Sheriff Sale happens when a property owner can’t pay what they owe — either their mortgage or property taxes — and the court steps in to force a sale.

In Philadelphia, there are two main types:

Mortgage foreclosure sales: The lender (bank) has gone through the foreclosure process and the court is now selling the property to recover the unpaid loan balance.

Tax lien sales: The owner hasn’t paid property taxes. The City of Philadelphia has placed a lien on the property, and eventually forces a sale to collect what’s owed.

Both are conducted as public auctions — anyone can bid. The winning bidder gets the property.

Philadelphia holds Sheriff Sales regularly — typically multiple times per month. You can find the schedule and listings on the Philadelphia Sheriff’s Office website (phillysheriff.com) and through the Philadelphia Court of Common Pleas.

Why the Prices Are So Attractive

Sheriff Sales start bidding at the upset price — the minimum amount needed to cover the outstanding debt (mortgage balance or tax lien) plus costs.

If a property has an outstanding mortgage of $45,000 and the home is worth $180,000 on the open market — bidding starts at $45,000. Sometimes it sells close to that. Sometimes competitive bidding drives it up. But the floor is the debt, not the market value.

This is why you see properties selling for prices that seem impossible. They’re not impossible — they’re just priced to recover a debt, not to reflect market value.

That gap between debt and market value? That’s the opportunity.

The Part That Should Make You Nervous

Here’s where I pump the brakes on my own excitement.

You cannot see inside the property before you bid.

Read that again. You are bidding — potentially tens of thousands of dollars — on a property you have never walked through. The interior could be pristine. It could have a collapsed ceiling, black mold, and a flooded basement. You don’t know.

Even appraisers often can’t get inside. You’re working from exterior observation, public records, and whatever information you can piece together.

One investor I read about bought a property at Sheriff Sale that looked solid from the outside. After winning the bid, they discovered the basement had chronic flooding issues and there were several large trees with root systems threatening the foundation. Emergency remediation alone cost $25,000 — on top of the purchase price.

That’s not unusual. It’s the risk you accept when you bid.

The Lien Problem: What Nobody Warns You About

This is the one that trips up the most people — including experienced investors.

When you buy a property at Sheriff Sale, you might assume all the debts attached to it disappear. Sometimes they do. But not always.

Here’s what can follow you home:

IRS tax liens: If the previous owner owed federal taxes and the IRS had filed a lien against the property, that lien may survive the Sheriff Sale. The IRS has specific redemption rights that can supersede the sale.

City of Philadelphia liens: Philadelphia is aggressive about filing liens for unpaid water bills, trash collection fees, L&I (Licenses & Inspections) violations, and code enforcement fines. These municipal liens can survive the sale and become your problem.

HOA liens: If the property is in a community with a homeowners association, unpaid HOA dues may carry over.

The terrifying part: these liens can sometimes exceed the purchase price. You could buy a property for $30,000 and discover $45,000 in municipal liens attached to it.

This is why a title search before you bid is non-negotiable.

Philadelphia’s lien information is public record. Before you bid on any property, you need to search:

- Philadelphia Court of Common Pleas records

- City of Philadelphia Department of Revenue (water/tax liens)

- L&I violation records

- IRS PACER system for federal tax liens

This takes time and ideally involves a title company or real estate attorney familiar with Philadelphia Sheriff Sales. It is not optional.

The Financing Problem

Here’s another thing most guides skip over.

If you’re planning to finance your Sheriff Sale purchase — not pay cash — you have a serious timing problem.

Sheriff Sales typically require you to pay a deposit (usually 10%) on the day of the sale, with the full balance due within 30 days.

Most lenders won’t finance a property in unknown condition. If the home is in bad shape, conventional lenders will refuse the loan outright. FHA has minimum property condition requirements that many Sheriff Sale properties won’t meet.

Your realistic financing options:

- Cash (obviously)

- Hard money loan (fast, doesn’t care about condition, but expensive)

- Private lender (if you have that relationship)

Going in without a financing plan — and without the cash to close if financing falls through — means you risk losing your deposit. That’s real money gone.

What a Good Sheriff Sale Deal Actually Looks Like

Despite all the warnings, good deals exist. Here’s what separates a smart bid from a gamble:

You’ve done the title search. You know exactly what liens exist and what you’d be taking on. No surprises.

You’ve walked the exterior thoroughly. Roof condition, foundation, windows, visible water damage signs, general structural appearance. You’re not flying blind.

You’ve pulled the permit history. L&I records show what work has been done (and what violations exist) on the property. Public record, free to access.

You’ve checked the neighborhood. What are similar properties selling for after renovation? What do rentals go for? What’s the buyer pool if you flip?

Your numbers work with a significant contingency. If you’re estimating $40,000 in repairs, make sure the deal works at $65,000. Because it will probably be $65,000.

You have your financing ready. Cash or committed hard money before you bid — not after.

What a Real Sheriff Sale Deal Actually Returns

I want to share a real example — not a success story, but an honest one.

An investor purchased a property at Sheriff Sale for $331,000, with fees and taxes bringing the total all-in cost to $335,000. He’d never seen the inside.

When he finally walked through, there was good news and bad news.

Good news: the previous owner had partially renovated — new flooring, modern bathroom tile work already in progress. Better than expected.

Bad news: the basement was completely destroyed. Three months without electricity meant water damage, mold, and a full gut job on the lower level.

Repair budget: $35,000.

Original target sale price: $450,000. Revised down to $435,000 after accounting for a softening market.

After repairs, agent commissions, taxes, and closing costs — net profit: $23,000. A 6.3% cash-on-cash return.

He called it a “single, not a home run.” And here’s the part worth paying attention to: he had originally planned to use financing. When he ran the numbers and realized the margins were too thin to absorb interest costs, he switched to all-cash and prioritized a fast sale over maximum profit.

That’s the reality of Sheriff Sale investing in a tighter market. Not every deal is a windfall. Some are just okay — and okay is fine, as long as you go in knowing that’s the realistic range.

The deals that go wrong are the ones where the investor needed a home run and got a single instead — and didn’t have the cash reserves to absorb the difference.

Who This Is Actually For

I want to be honest about something.

Sheriff Sale investing is most appropriate for:

- Experienced investors with contractor relationships who can accurately estimate repair costs

- People with cash or committed hard money financing

- Investors who understand Philadelphia’s lien landscape and have done thorough due diligence

It is not ideal for:

- First-time buyers using conventional financing

- Anyone who hasn’t done a title search

- People whose entire budget is the purchase price with nothing left for repairs

This doesn’t mean beginners should never pursue Sheriff Sales. It means beginners should understand exactly what they’re getting into — and ideally partner with someone experienced on their first deal.

I’m in the research phase on this myself. The prices are genuinely compelling. But I’m not bidding on anything until I understand the title search process cold and have financing lined up.

The deal that looks too good to be true sometimes is. And sometimes it’s the best opportunity in the room. The difference is almost always what you knew before you raised your hand.

Not financial advice — just someone doing a lot of research and asking a lot of questions. Consult a real estate attorney familiar with Philadelphia Sheriff Sales before bidding on any property.