Find foreclosures free — most people think this requires expensive subscriptions, insider connections, or a real estate license. It doesn’t.

There are several completely free platforms that list foreclosure and distressed properties. Knowing how to use them effectively puts you ahead of most buyers who are just scrolling Zillow hoping something good shows up.

Here’s what actually works.

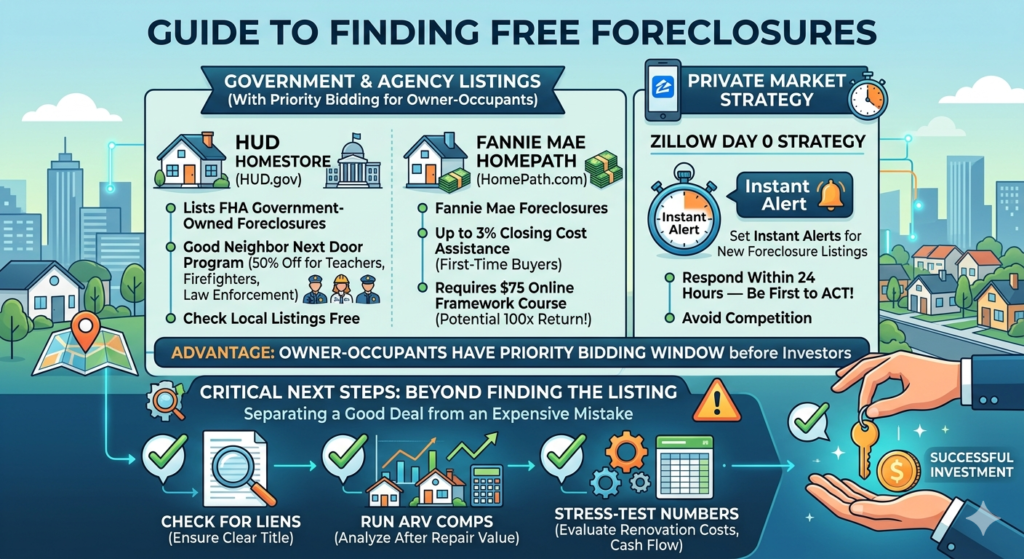

Platform 1: HUD Home Store — Find Foreclosures Free From the Government

We’ve covered HUD homes before — these are properties that came back to the government after FHA-backed loans went into default.

HUD Home Store (hudhomestore.gov) is the official listing site. It’s free, updated regularly, and searchable by state, county, and property type. One of the best places to find foreclosures free of charge.

The Good Neighbor Next Door Program

If you’re a law enforcement officer, firefighter, EMT, or teacher — this is one of the most powerful homebuying programs in existence and almost nobody talks about it.

HUD will sell you a qualifying property at 50% off the listed price. Not a small discount. Half price.

The catch: you must live in the property as your primary residence for at least three years, and the properties are in designated “revitalization areas” — neighborhoods HUD has identified as needing investment.

For a teacher or firefighter buying in Philadelphia, this could mean a $200,000 home for $100,000. The equity built from day one is extraordinary.

The $100 Down Payment Program

Also through HUD Home Store — owner-occupants using FHA financing can sometimes purchase qualifying HUD properties with just $100 down instead of the standard 3.5%.

Both programs are available directly through hudhomestore.gov. You must work with a HUD-registered real estate agent to submit offers.

Platform 2: Fannie Mae HomePath — Find Foreclosures Free From Conventional Defaults

Fannie Mae’s equivalent to HUD Home Store — properties that came back to Fannie Mae after conventional loan defaults.

HomePath (homepath.com) is free to search and updated regularly. The properties tend to be in better condition than HUD homes on average, because conventional borrowers often had more equity and the homes were maintained longer before default.

The HomePath Ready Buyer Program

First-time homebuyers who complete a required online homebuying education course can receive up to 3% of the purchase price toward closing costs on a HomePath property.

On a $250,000 home, that’s $7,500 back at closing. The course is offered through Framework (frameworkhomeownership.org) and costs $75. For $75 and a few hours of your time, you unlock $7,500 in closing cost assistance. That’s a 100x return on the course fee.

Owner-Occupant Priority Period

Like HUD, Fannie Mae gives owner-occupants a priority bidding window — typically the first 20 days a property is listed. Investors can’t submit offers during this period.

If you’re buying to live in the property, this is a significant advantage when you find foreclosures free through HomePath.

Platform 3: Zillow, Realtor.com, Redfin — The Day 0 Strategy to Find Foreclosures Free

There’s a specific strategy worth knowing that contradicts conventional wisdom about public listing sites.

The Day 0 Strategy

When a foreclosure or REO property first hits the MLS, most buyers don’t see it immediately. Alerts take time to process. The first 24 hours are actually less competitive than hour 48 or 72.

The strategy: set up alerts for your specific search criteria — including the “Foreclosure” filter — and respond the same day a qualifying property appears.

On Zillow specifically:

- Search your target area

- Filter by “Foreclosure” under listing type

- Save the search and enable instant alerts

- When something appears — move fast

This doesn’t give you the wholesale-level pricing of a pre-MLS deal. But foreclosure properties on the MLS are still often priced below market, and moving on day one means you’re competing against fewer buyers than everyone who sees it on day three.

Running the same search across Zillow, Realtor.com, and Redfin gives you the most complete picture of where you can find foreclosures free on the open market.

What to Look for When You Find Foreclosures Free

Before you get excited about a price, run through this checklist:

Winterization labels. Labels on toilets, sinks, or water heater saying “winterized” mean the property has been sitting vacant long enough that someone had to drain the pipes. Information about condition and timeline — not automatically a dealbreaker, but worth noting.

Days on market. A foreclosure sitting for 90+ days either has a problem (condition, title issues, pricing) or just hasn’t found the right buyer. Investigate why before assuming it’s a hidden gem.

Tax and lien records. Pull public records before you get emotionally attached. Philadelphia specifically has municipal liens for water bills, L&I violations, and code enforcement fines that can follow the property through a sale.

Comparable sales. What have similar properties sold for recently — after renovation? That’s your ARV. Work backward to figure out what the property is worth to you as an investment.

Making Sure the Deal Actually Works After You Find Foreclosures Free

Finding a foreclosure is the first step. Making sure it’s actually a good deal is the second — and more important — step.

For a flip: Purchase price + repair costs + holding costs + selling costs should leave enough profit to justify the risk. Total costs should be at or below 70% of ARV.

For a rental: The 1% rule gives you a quick screen — monthly rent should be approximately 1% of your total all-in cost. A property you bought and rehabbed for $150,000 should rent for around $1,500/month to cash flow reasonably.

These aren’t hard rules. They’re filters. If a deal passes both screens, it’s worth analyzing more deeply. If it fails both, move on quickly.

According to HUD.gov, the Good Neighbor Next Door program has helped thousands of public servants build equity in designated revitalization areas — but participation rates remain low because most eligible buyers simply don’t know the program exists.

The Free Foreclosure Search Stack

- HUD Home Store — government-owned FHA foreclosures, with special programs for first responders, teachers, and low-down-payment buyers

- Fannie Mae HomePath — conventional loan foreclosures, with closing cost assistance for first-time buyers

- Zillow/Realtor/Redfin with foreclosure filter + Day 0 alerts — MLS foreclosures, best accessed on day one before competition builds

None of these require a subscription. None require a license. They require time, attention, and the discipline to run the numbers before getting excited about a price.

Use the Sheriff Sale Bid Calculator to run your numbers on any foreclosure deal — plug in purchase price, repairs, and ARV to see your maximum bid before you make any offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions.