Tax lien tax deed investing is a legitimate, government-administered process that’s been around for decades — and most investors have never heard of it. It involves buying properties for a fraction of their value, sometimes for as little as the unpaid tax bill.

Let me break down how both systems work — and then get specific about what’s available in Pennsylvania.

The Problem That Creates the Tax Lien Tax Deed Investing Opportunity

Every property owner pays property taxes. When they don’t — for months, sometimes years — the local government has a problem. They’re owed money needed to fund schools, roads, and public services.

The solution: sell the debt (or the property itself) to outside investors to recover the unpaid taxes quickly. In exchange, investors get either high interest returns or actual ownership of the property.

This is the entire basis of tax lien tax deed investing.

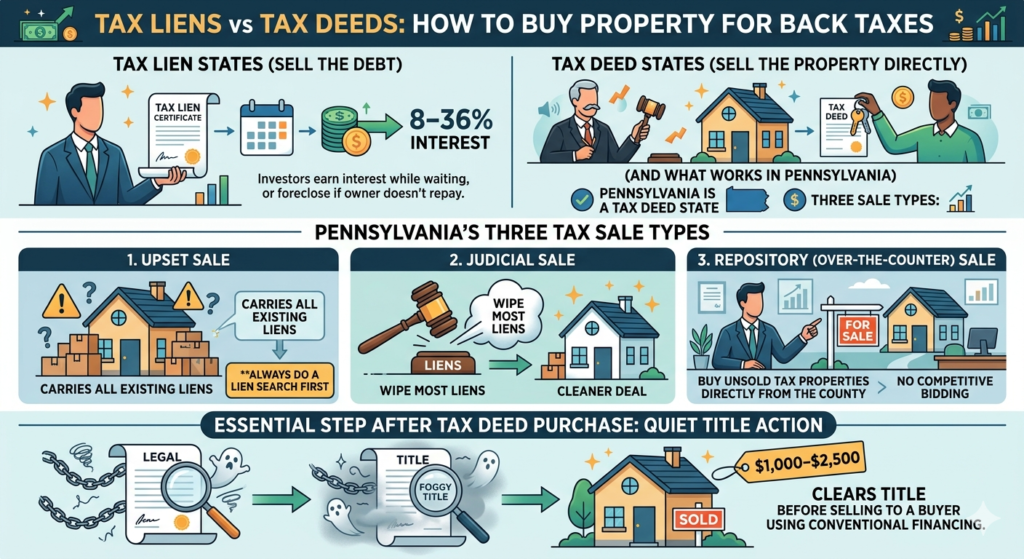

Tax Lien Investing: Buying the Debt, Not the Property

In tax lien states, the government doesn’t immediately sell the property. Instead, they sell the right to collect the debt — a tax lien certificate — to investors at auction.

A homeowner owes $6,000 in unpaid property taxes. The county sells that $6,000 debt to an investor. The investor pays the county — the county gets their money immediately. Now the homeowner owes that $6,000 to the investor instead.

The return: To get their property back, the homeowner must repay the investor the original tax amount plus interest. Depending on the state, that interest rate can range from 8% to 36% annually. Florida caps it at 18%. Illinois allows up to 36%. These are legally mandated rates — not negotiated.

What if the homeowner never pays?

After a set redemption period — typically one to three years — the investor can initiate foreclosure proceedings and take ownership of the property. For a $6,000 investment, you could end up owning a property worth significantly more.

Tax lien states include Florida, New Jersey, Illinois, Arizona, and Maryland.

Tax Deed Investing: Buying the Property Directly

In tax deed states, the government skips the debt-selling step entirely. When a property owner falls far enough behind on taxes, the government seizes the property and sells it directly at auction.

The winning bidder gets the deed — actual ownership of the property.

Bidding typically starts at the amount of unpaid taxes plus fees and costs. In areas with low competition, properties can sell for dramatically below market value.

The key advantage of tax deed investing: You’re buying property, not a debt instrument. No waiting for a redemption period. No wondering if the owner will pay you back.

Tax deed states include Pennsylvania, California, Michigan, and Texas.

Pennsylvania’s Tax Lien Tax Deed Investing System: Three Types of Tax Sales

Pennsylvania is a tax deed state — but with a more complex structure than most. There are three distinct types of tax sales.

1. Upset Sale

The first sale attempted when a property has delinquent taxes. Bidding starts at the total amount of delinquent taxes, municipal liens, and costs.

The critical catch: all existing liens survive the Upset Sale. If the property has a mortgage, HOA liens, city water bills, or code violation fines — those all transfer to the new owner. Always do a thorough lien search before bidding at an Upset Sale.

2. Judicial Sale

Properties that didn’t sell at Upset Sale move to Judicial Sale. This is where tax lien tax deed investing gets interesting in Pennsylvania.

Judicial Sales are court-ordered — and they wipe out most liens. The property transfers with a cleaner title than an Upset Sale. This is generally the better entry point for investors who want a cleaner deal.

3. Repository Sale (Over-the-Counter)

Properties that didn’t sell at either Upset or Judicial Sale end up in the Repository — a list maintained by the county of unsold tax sale properties.

Repository properties can be purchased directly from the county without competitive bidding. You negotiate a price with the county. This is where the $50 land stories come from — and where occasional genuine opportunities are buried in the list.

Every Pennsylvania county maintains its own Repository list. Philadelphia’s is managed through the Philadelphia Land Bank and the Sheriff’s Office.

The Philadelphia Wrinkle in Tax Lien Tax Deed Investing

In most Pennsylvania counties, there’s no redemption period after a tax sale — once you buy it, it’s yours. Philadelphia is an exception: if the property was owner-occupied within 90 days before the sale, the original owner may have a right of redemption.

Philadelphia also has the Philadelphia Land Bank — a city-run entity that acquires tax-delinquent properties and sells them through a separate application process, often at below-market prices to buyers who commit to rehabilitating them.

Quiet Title: Cleaning Up the Title After Tax Lien Tax Deed Investing

When you buy a property at a tax sale, you get a deed. But some title insurance companies are reluctant to insure tax deed properties because there can be questions about whether the proper legal notices were sent to the previous owner.

The solution: a Quiet Title action. This is a court proceeding that legally confirms your ownership and clears any competing claims. Once a court grants a Quiet Title judgment, title insurance becomes straightforward.

Cost: typically $1,000–$2,500 in attorney fees. Timeline: several months. If you plan to sell the property to a buyer using conventional financing, budget for Quiet Title from the start.

What Tax Lien Tax Deed Investing Looks Like in Practice

Research before every auction. Pull the parcel ID, check the address, research the neighborhood, estimate repair costs, understand your exit strategy. Doing this on 20 properties to find 2 worth bidding on is normal.

Lien searches before Upset Sales. At minimum, check Philadelphia’s public records for water/sewer liens, L&I violations, and any other municipal charges. These survive Upset Sales.

Judicial or Repository for cleaner deals. If you want to minimize lien risk, focus on Judicial Sales and Repository properties rather than Upset Sales.

Consistent participation. Investors who do well in tax lien tax deed investing show up consistently, build pattern recognition, and develop relationships with county officials.

A clear exit strategy. Flip it? Rent it? Wholesale? Know before you bid.

According to HUD.gov, tax-delinquent properties represent one of the most significant sources of affordable housing inventory in older urban markets — making tax lien tax deed investing particularly relevant in cities like Philadelphia with large stocks of aging, distressed housing.

Use the Philadelphia Deal Finder to cross-reference tax delinquent properties in your target Philadelphia neighborhoods before you attend any auction — knowing the neighborhood comps cold is what separates profitable bids from expensive mistakes.

Not financial advice — just someone doing a lot of research and asking a lot of questions. Tax sale rules vary by county and change over time — verify current procedures with the relevant county tax claim bureau or a Pennsylvania real estate attorney.