Real estate roadmap for beginners doesn’t have to mean “quit your job and go all in.” The best framework I’ve found is realistic, step-by-step, and designed for someone who’s still working, still learning, and doesn’t have a ton of cash sitting around.

This comes from investor Pace Morby — and what I like about it is that it gives you a structured reason to stop waiting and start building.

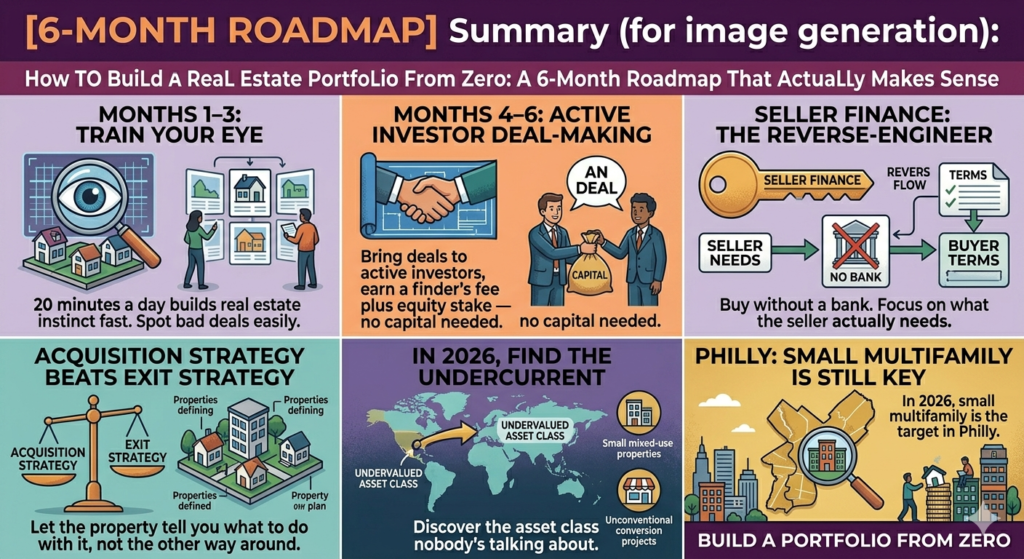

The Real Estate Roadmap for Beginners: Months 1–3

Most people who want to get into real estate spend months consuming content without doing anything. Pace’s real estate roadmap for beginners fixes that with a specific starting point.

Learn to see bad deals first.

Before you can recognize a good deal, you have to train your eye to spot bad ones. The exercise: join underwriting calls — group deal analysis sessions where investors walk through real properties and explain why something doesn’t work. Do this every week.

On top of that, spend 20 minutes a day looking at listings. Not to buy anything. Just to look. Run the numbers. Ask yourself: does this cash flow? What’s the cap rate? What would it take to make this work?

He calls this building your “real estate kung fu” — the instinct that eventually lets you look at a deal and know in 30 seconds whether it’s worth your time. You can’t rush it, but you can speed it up by being intentional about the reps.

In Philadelphia, this means getting familiar with what properties actually sell for versus what they list for, what rents look like in different neighborhoods, and what typical rehab costs are here. The Germantown and North Philly numbers are very different from Fishtown or Graduate Hospital. You need to know your market before any other part of this real estate roadmap for beginners makes sense.

The Real Estate Roadmap for Beginners: Months 4–6

This is the part that most beginner frameworks skip — and I think it’s the most valuable advice in the whole roadmap.

Attach yourself to someone already doing it.

Instead of trying to do your first deal solo, find an investor who’s already actively buying and bring them deals. In exchange, ask for two things: a finder’s fee (around $50,000 for a good deal) and a 10% equity stake in the asset.

You’re not putting in capital. You’re putting in time, research, and hustle. And in exchange, you get paid and you get a seat at the table on a real deal — with someone who already knows what they’re doing.

Deal two: negotiate 20–40% equity. Deal three: you’re doing it yourself.

That’s how this real estate roadmap for beginners takes you from zero to owning real estate without a massive down payment or years of solo grinding.

Seller Finance: The Real Estate Roadmap for Beginners Without a Bank

Seller financing means the seller acts as the bank. Instead of going to a lender, you go directly to the person who owns the property and structure a payment plan with them. No credit check. No debt-to-income ratio scrutiny. No bank committees.

Pace explains it with what he calls “reverse engineering” the deal:

Start with what you need the deal to cash flow. Let’s say you want $10,000/month in net income. Work backwards — what purchase price, interest rate, and repayment term would make that possible? Then go present those numbers to the seller.

The real example he shares: a guy named Mario who owned a 43-unit apartment building worth $3 million. Mario was missing his son’s baseball games to deal with broken toilets. Burned out and done.

Pace’s pitch wasn’t about cap rates. It was: “What if your son grew up knowing that every single month, for the rest of his life, a check for $16,000 shows up — because of you?”

Mario became the bank. He gets $16,000/month for decades. Pace structured the repayment term long enough that his net income on the deal lands around $11,000/month.

No bank. No traditional financing. Just a conversation about what the seller actually needed.

Philadelphia has a lot of tired landlords — people who’ve been managing rowhouses for 20 years and just want out. That’s a motivated seller pool that makes this part of the real estate roadmap for beginners genuinely actionable here.

Acquisition First, Exit Second: The Real Estate Roadmap for Beginners Reframe

Most people start by deciding on an exit strategy. “I want to do Airbnb.” “I want to flip.” “I want Section 8 tenants.” Then they go look for properties that fit that plan.

This real estate roadmap for beginners argues that’s backwards — and I think it’s right.

The property tells you the exit strategy. You can’t decide you’re going to Airbnb something if the HOA prohibits short-term rentals. You can’t flip if the ARV doesn’t support the numbers. The property’s conditions, location, zoning, and price are what determine what’s possible.

What you can control is your acquisition strategy — how you find deals that other people miss. Foreclosures, inherited properties, tax liens, motivated sellers, sheriff sales. These are skills you build. The more acquisition tools you have, the more flexibility you have to work with whatever deal you find.

In Philadelphia’s sheriff sale and tax sale market, properties don’t arrive with a neat bow on them. You don’t always know going in whether a property is going to be a flip, a rental, or something you wholesale. What matters is that you got it right on the acquisition — and then you let the property tell you what to do with it.

Why Asset Class Timing Matters in This Real Estate Roadmap for Beginners

Airbnb is oversaturated. Supply has flooded the market, regulations are tightening in cities including Philadelphia, and margins have compressed significantly.

The underlying principle of this real estate roadmap for beginners: look for the asset class that’s undervalued and under-competed right now, not the one that’s been on every podcast for the last three years.

In Philadelphia, that’s still multifamily. 2–4 units. Below the radar, manageable, and with seller finance opportunities if you find the right tired landlord.

Pulling the Real Estate Roadmap for Beginners Together

No money? Find deals for people who have money. No experience? Attach yourself to someone with experience. No conventional financing? Learn creative finance.

The throughline: stop waiting for perfect conditions and start building the skills. The market will always have something going on — rates, regulations, uncertainty. The investors who build portfolios anyway are the ones who develop enough tools to work with whatever’s in front of them.

The 20 minutes a day looking at deals sounds small. It adds up fast.

According to BiggerPockets, the investors who successfully execute a real estate roadmap for beginners almost universally credit consistent deal analysis — not capital — as the skill that unlocked their first acquisition, because understanding the numbers is what makes every other part of the process possible.

Use the Strategy Score Rankings to evaluate which real estate roadmap for beginners strategies fit your current situation — capital level, experience, market access — before you commit to any specific path.

Not financial advice — just someone doing a lot of research and asking a lot of questions.