Let me say something that took me a while to fully accept.

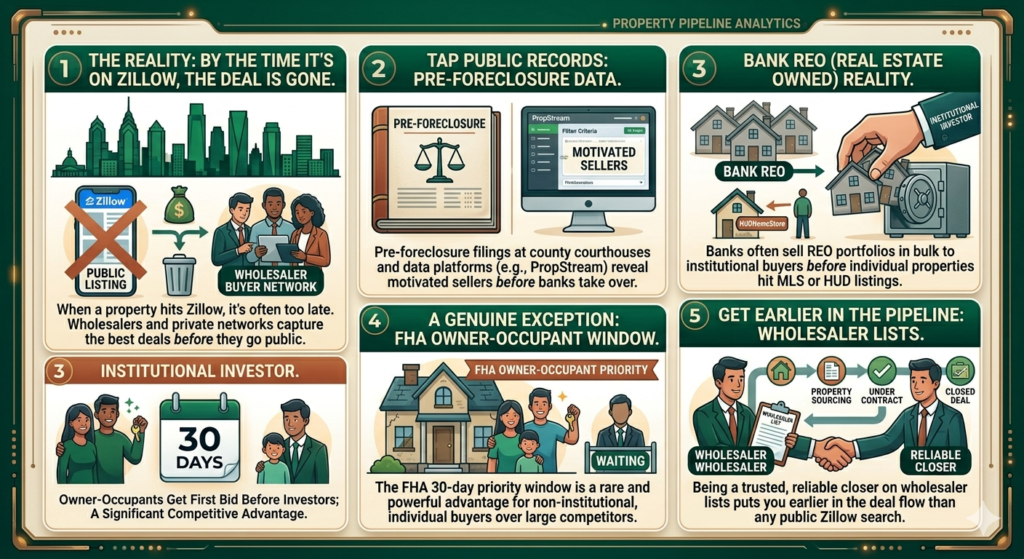

If you’re scrolling Zillow looking for your next investment property, you’re already too late.

Not always. Not for every deal. But for the genuinely underpriced properties — the ones with real margin, the ones that make the math work — by the time they hit Zillow or Realtor.com, someone else has already looked at them, run the numbers, and decided whether to move.

That someone is usually a wholesaler.

How the Pipeline Actually Works

Here’s what the deal flow looks like before a property ever reaches a public listing site:

Stage 1: Off-market A motivated seller — tired landlord, estate sale, pre-foreclosure, financial distress — decides they need to sell. They haven’t listed anywhere yet. A wholesaler with the right systems finds them first through direct mail, cold calling, driving for dollars, or referral networks. The wholesaler locks up the property under contract.

Stage 2: Wholesale network The wholesaler shops the contract to their buyer list — investors who’ve built relationships with them. These buyers get first look. The best deals get snapped up here, often within 48 hours.

Stage 3: MLS / Zillow Whatever doesn’t sell through the wholesale network eventually hits the MLS. By this point, the property either has no margin left (the wholesaler priced it too high) or it has problems the wholesale buyers passed on.

This is what most beginner investors are shopping. The leftovers.

Pre-Foreclosure: Another Layer Before Zillow

Foreclosures follow a similar pattern. Before a bank can sell a property, there’s a legal process — and that process is public record.

Pre-foreclosure is the period between when a homeowner defaults and when the bank actually takes possession. During this window, the homeowner can still sell — and motivated sellers in pre-foreclosure often accept below-market offers because they need out fast.

You can find pre-foreclosure listings through:

- County courthouse records — foreclosure filings are public. In Philadelphia, these are filed through the Philadelphia Court of Common Pleas

- PACER (federal court records for bankruptcy filings)

- Paid services like PropStream, ATTOM, or similar data platforms that aggregate this information

This requires more legwork than browsing Zillow. Which is exactly the point — the extra work is what creates the opportunity.

Bank REO: After Foreclosure

Once the bank takes possession, the property becomes REO (Real Estate Owned). Banks don’t want to hold REO — they’re not in the property management business. They want to sell.

But even here, the timeline matters. Banks often sell REO in bulk to large investors before individual properties ever hit HUDHomeStore or the MLS. The retail listings you see are what’s left after institutional buyers have already picked through the inventory.

The exception: the FHA owner-occupant priority window we covered in the last post. That 30-day window where only owner-occupants can bid is a genuine advantage — use it.

The Bottom Line: Build the Relationships First

The investors who consistently find good deals aren’t better at searching Zillow. They’ve built the relationships that put them earlier in the pipeline.

Wholesalers are the most direct path. Get on their buyer lists. Tell them exactly what you’re looking for. Close when you say you will. That last part — being a reliable buyer — is what gets you the first call when a good deal comes in.

Direct mail and driving for dollars puts you at Stage 1 — finding motivated sellers before anyone else does. More work, but maximum margin.

County courthouse gets you into pre-foreclosure before the bank takes over — and before the property hits any listing site.

None of this is passive. It requires showing up, building relationships, and doing the unglamorous work that most people scrolling Zillow on their couch won’t do.

That gap between what most people do and what actually works — that’s where the deals live.

Not financial advice — just someone doing a lot of research and asking a lot of questions.