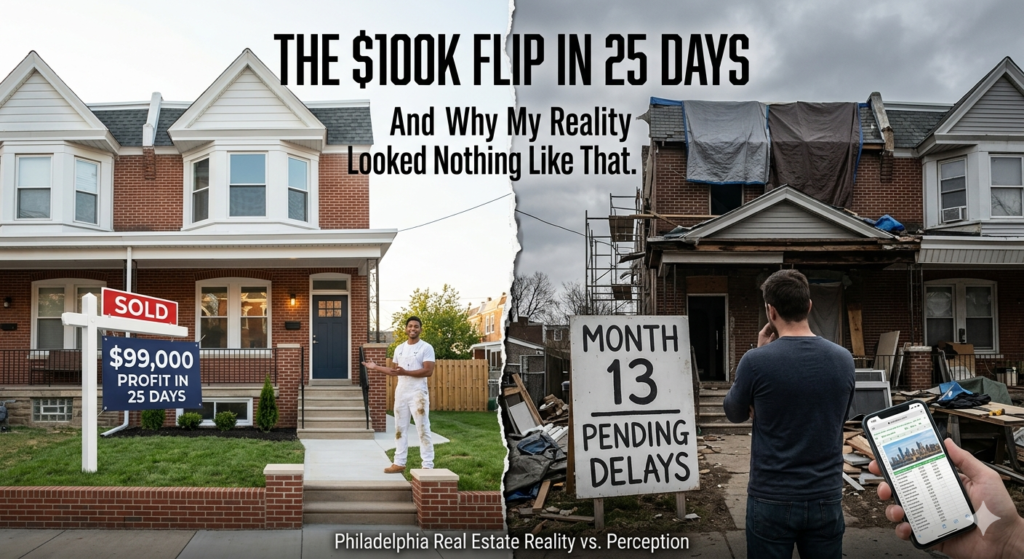

Cash out refinance investment property strategies look clean on video. The reality? A lot messier — and I learned that the hard way.

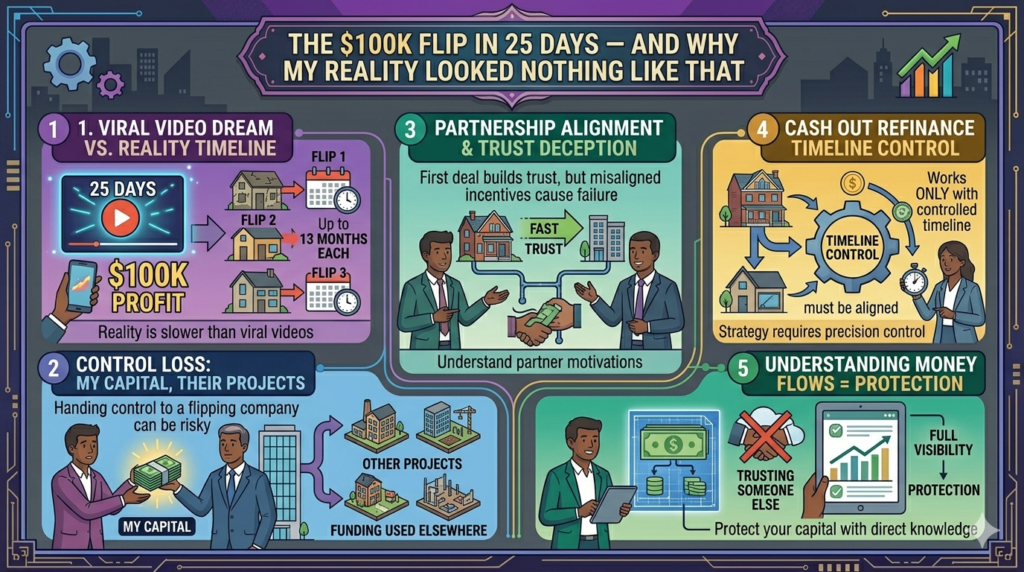

I came across a video recently of two guys standing in front of a house, walking through a flip they just finished.

The numbers? Clean.

- Purchase price: $100,000

- Renovation: $26,000

- Appraisal: $225,000

- Profit: almost $100,000

- Timeline: 25 days

Updated the exterior paint, fixed the front, rearranged a few things inside. Both guys smiling at the end. It looked effortless.

And honestly? It made me think about my own flipping experience — because mine looked nothing like that.

When I Handed Everything Over

When I first got into flipping, I didn’t know construction. So I did what felt logical at the time — I found a flipping company and trusted them with the whole process.

I showed up to site visits. Helped where I could. But the real decisions? I left those to them.

They told me: “We’ll finish in 4 months. If you give us the down payment, you can get three flips done in one year.”

It sounded good. And at first, they kept their word.

- First flip: Done in about 4 months. Right on time.

- Second flip: Took around 8 months. Profit: about $20,000.

- Third flip: More than 12–13 months. Profit: around $19,000.

What I Didn’t See Coming

As the company grew, I started to notice a pattern.

The first flip was fast — because they needed to build trust. After that, things started slipping. Timelines stretched. Delays stacked up.

What I didn’t realize at the time: they were collecting down payments from new investors and using that money to fund other projects. My capital just sat there, waiting — longer and longer each time.

By the third flip, my down payment was around $130,000. I was lucky I didn’t lose everything. The profit was still better than leaving that money in a bank — so I didn’t feel completely robbed. But I felt something worse: I felt like I hadn’t been paying attention.

According to BiggerPockets, partnership deals gone wrong are one of the most common ways new investors lose money — not because of the market, but because of misaligned incentives.

What This Has to Do With Cash Out Refinance Investment Property Strategy

Here’s the connection I didn’t make back then.

A cash out refinance investment property approach — where you force equity through renovation and pull it back out through refinancing — only works if you control the timeline. If someone else is managing your project and dragging their feet, your carrying costs eat your returns. And if they’re using your down payment to fund other deals, you’ve essentially given them an interest-free loan.

Understanding the cash out refinance investment property structure is what protects you. Because when you know how the money flows — acquisition, rehab, appraisal, refi — you know exactly where delays cost you. And you stop handing that control to someone else.

Want to see how the numbers actually stack up on a cash out refi deal? The Cash Out Refi Calculator will show you exactly where you stand before you commit.

What It Taught Me

The video makes flipping look clean. 25 days. $100K profit. Two guys smiling at the camera.

Real life — especially when you hand everything over to someone else — is messier.

A good partner or professional company can genuinely help. But understanding the process yourself? That’s what actually protects you. After my third flip, I made a decision: learn this myself. Less “trust the company.” More “understand the numbers and the construction.”

That’s why I’m here, writing this.

Not financial advice — just someone doing a lot of research and asking a lot of questions.