Creative finance multifamily investing sounds like something only seasoned investors with connections can pull off. This case study proves otherwise.

A 24-unit townhome complex in Nebraska. Purchase price $1.7 million. Money out of pocket from the buyers: zero dollars. One year later, the property appraised at $3.4 million — double the purchase price — and the investors pulled out $150,000 in cash at refinance after paying off every loan.

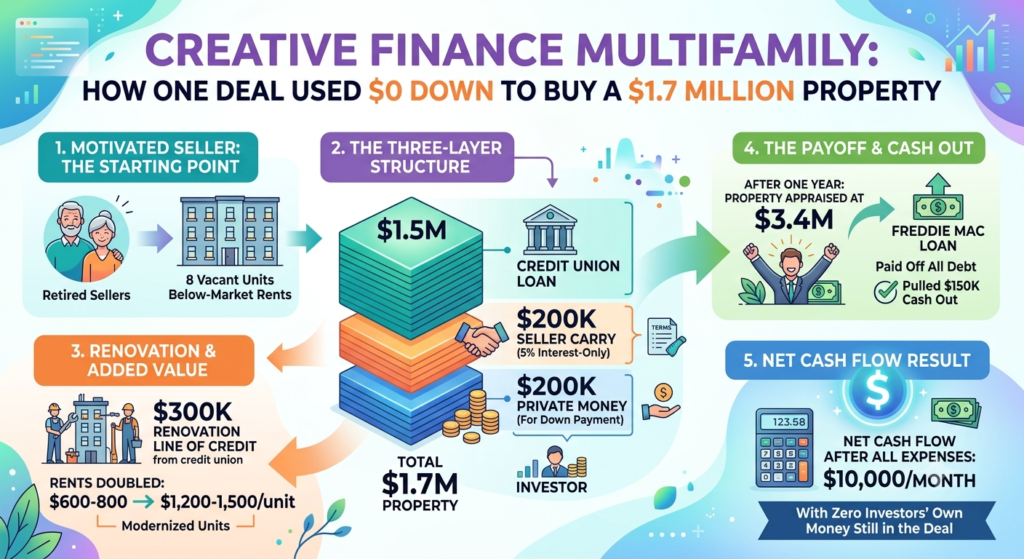

Here’s exactly how they did it.

Why Creative Finance Multifamily Deals Start With the Seller’s Problem

The deal worked because the buyers weren’t just looking for a property. They were looking for a seller with a problem they could solve.

In this case, the sellers were a retired couple who had owned the complex for years. Eight units were vacant. Some had water damage. Rents were running $600 to $800 per unit — well below market. The sellers were tired, overwhelmed, and ready to move on. They didn’t need all their money at once. They needed someone to take the problem off their hands.

That’s the foundation of creative finance multifamily investing. You’re not just buying a building. You’re solving a problem for a seller who has something to gain from a flexible structure.

The Three-Layer Creative Finance Multifamily Structure

The buyers put together three financing layers that stacked on top of each other to cover the full $1.7 million purchase price.

Layer 1 — Conventional loan from a credit union: $1.5 million A local credit union provided the primary mortgage. Credit unions are often more flexible than large banks on commercial deals, especially when the borrower can demonstrate a clear value-add plan.

Layer 2 — Seller carry: $200,000 The sellers agreed to carry $200,000 of the purchase price themselves. Instead of receiving that money at closing, they would receive interest-only payments at 5% for three years, with the balance paid off at refinance. For the sellers, this created a reliable income stream at a better rate than they’d get from a bank CD. For the buyers, it covered the gap without touching their own capital.

Layer 3 — Private money for the down payment: $200,000 The credit union required a down payment. The buyers sourced that from a private lender — an individual investor who provided the funds in exchange for a return. The down payment was covered. Total out-of-pocket for the buyers: zero.

This is what creative finance multifamily structure looks like in practice — not one creative move, but three layers working together.

How They Added $1.7 Million in Value in One Year

Buying the deal was step one. Creating the value was where the real work happened.

The credit union also extended a $300,000 line of credit for renovations — again, not the buyers’ money. Those funds went into the units: kitchen updates, bathroom repairs, fixing the water damage, and bringing everything up to a standard that justified market-rate rents.

The result: rents went from $600 to $800 per unit to $1,200 to $1,500 per unit. With 24 units, that rent increase transformed the NOI and, by extension, the appraised value.

This is the core mechanic of creative finance multifamily value-add investing. Commercial properties are valued on income, not comps. Raise the NOI, raise the value. The math is direct.

Run your numbers through the Multi-Unit Cash Flow Calculator before you commit to a renovation budget. Know exactly what NOI you need to hit your target appraised value at refinance.

The Refinance That Paid Everyone Back

One year after closing, the property appraised at $3.4 million.

The buyers refinanced into a Freddie Mac agency loan at a lower interest rate. The new loan paid off the credit union mortgage, the seller carry balance, and the private money loan — in full. After clearing every debt, they had $150,000 in cash left over from the refinance proceeds.

According to the Federal Housing Finance Agency, Freddie Mac multifamily loans are among the most competitive long-term financing options available for stabilized apartment properties — which is exactly why the refinance into agency debt was the target from day one.

Zero dollars in. Every debt paid off. $150,000 cash out. Monthly net cash flow of approximately $10,000 after all expenses.

What Creative Finance Multifamily Actually Requires

This deal didn’t happen because the buyers got lucky. It happened because they understood a few things clearly.

Motivated sellers are the starting point. A seller who needs all cash at closing on day one can’t do a creative deal. You’re looking for sellers who are tired, retiring, dealing with deferred maintenance, or facing vacancy problems they don’t want to solve. Their situation creates the flexibility.

Your plan has to be credible. The credit union, the seller, and the private lender all said yes because the buyers could demonstrate a clear path from distressed property to stabilized asset. Lenders and sellers both need to believe the value-add plan is real.

The structure has to work for everyone. The seller got income-only payments at 5% for three years — better than a CD. The private lender got a return on capital. The credit union got a performing commercial loan. Creative finance multifamily isn’t about squeezing sellers. It’s about finding structures where everyone wins.

Not financial advice — just someone doing a lot of research and asking a lot of questions.