Let me tell you about the loan that changed the way I think about real estate investing.

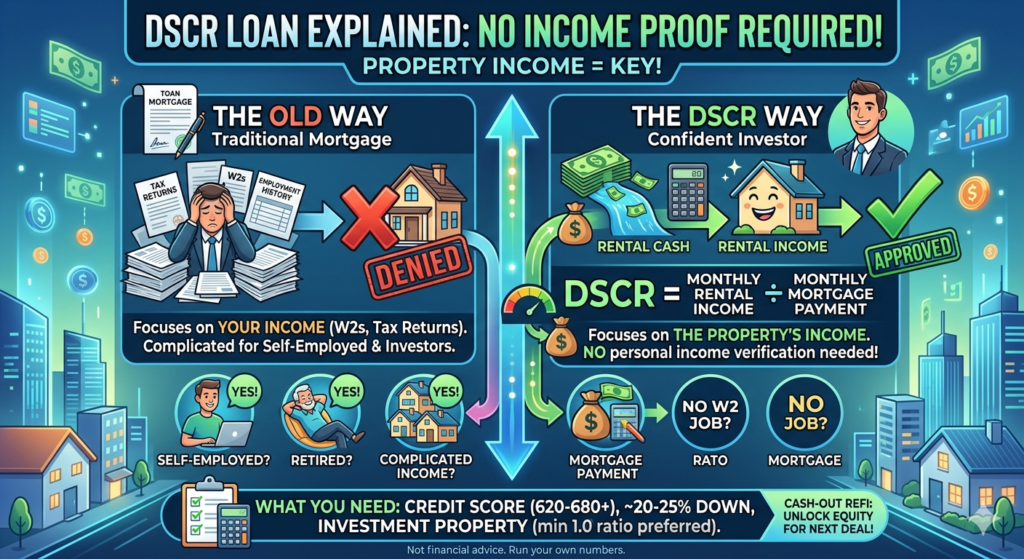

I used to assume that getting a mortgage meant proving you had a steady paycheck. W2s, tax returns, two years of employment history — the whole traditional package. And if you didn’t have that? No loan.

Then I learned about DSCR loans. And everything I thought I knew went out the window.

What Is a DSCR Loan?

DSCR stands for Debt Service Coverage Ratio. It’s a number that measures one simple thing: can this property pay for itself?

The formula:

DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment

That’s it. The lender isn’t looking at your income. They’re looking at the property’s income.

What the Numbers Mean

DSCR of 1.0: Rental income exactly covers the mortgage. Break even. The property pays for itself — nothing more, nothing less.

DSCR above 1.0 (1.2, 1.5, etc.): Rental income exceeds the mortgage payment. Positive cash flow. The higher the DSCR, the stronger your loan terms — lower rates, better conditions, happier lenders.

DSCR below 1.0 (0.8, 0.9): Rental income doesn’t fully cover the mortgage. You’d need to cover the gap out of pocket. Most lenders want at least 1.0, though some will go as low as 0.8.

Why This Changes Everything

The traditional mortgage process is built around you — your job, your income, your tax returns.

DSCR loans are built around the property.

That means:

- Self-employed? Doesn’t matter.

- Retired? Doesn’t matter.

- Multiple investment properties with complicated income? Doesn’t matter.

- No traditional W2 income? Doesn’t matter.

What matters is whether the rent covers the mortgage. If it does, you have a case for a loan.

For anyone whose financial life doesn’t fit neatly into a W2 box — which is a lot of investors — this is a completely different door into real estate.

DSCR + Cash-Out Refinance: Why Right Now Is Interesting

Here’s where it gets really useful.

If you already own a rental property, rising rents have quietly been improving your DSCR over time — even if your mortgage payment stayed the same.

Say your mortgage is $2,500/month and your rent was $2,500 when you bought. DSCR of 1.0 — break even.

Now rents have gone up. Your tenant is paying $4,000/month. If you refinance and your new mortgage is $3,000/month — your DSCR is now 1.33. That’s positive cash flow, and the lender sees much lower risk.

Lower risk to the lender = better rates for you.

And because you’ve built equity in the property, a cash-out refinance lets you pull that equity out as cash — to invest in your next deal.

This is the engine behind the BRRRR strategy. And DSCR loans are what make it work for investors who don’t have traditional income.

DSCR Loans in Philadelphia

Philadelphia’s rental market has been strong — and rising rents mean DSCR numbers are looking better across the board for existing landlords.

For new investors, DSCR loans open up a path that conventional financing closes off. Buy a property that generates enough rent to cover the mortgage, and you can qualify — regardless of what your tax return looks like.

The suburbs around Philadelphia (Montgomery County, Bucks County, Delaware County) also work well for DSCR — lower purchase prices relative to rent potential means the ratios often work in your favor.

What You Need to Qualify

Every lender is different, but typical DSCR loan requirements:

- Credit score: usually 620–680 minimum (higher = better terms)

- DSCR: 1.0 or above (some go to 0.8)

- Down payment: typically 20–25%

- Property type: investment properties only — not your primary residence

- Loan amounts: vary by lender

No income verification. No employment history. No tax returns required.

Check Your DSCR Before You Apply:

Not financial advice — just someone doing a lot of research and asking a lot of questions.