I hear it constantly. “The market’s too expensive.” “Interest rates killed the deals.” “There’s no way to make money in real estate right now.”

And honestly? For a traditional buyer trying to finance a home with a conventional mortgage based on their W-2 income — yeah, they’re not wrong. That math is brutal right now.

But not everyone buys the same way. And that changes everything.

A Deal I’ve Been Studying

I came across a video recently where an investor walked through a duplex deal that stopped me in my tracks.

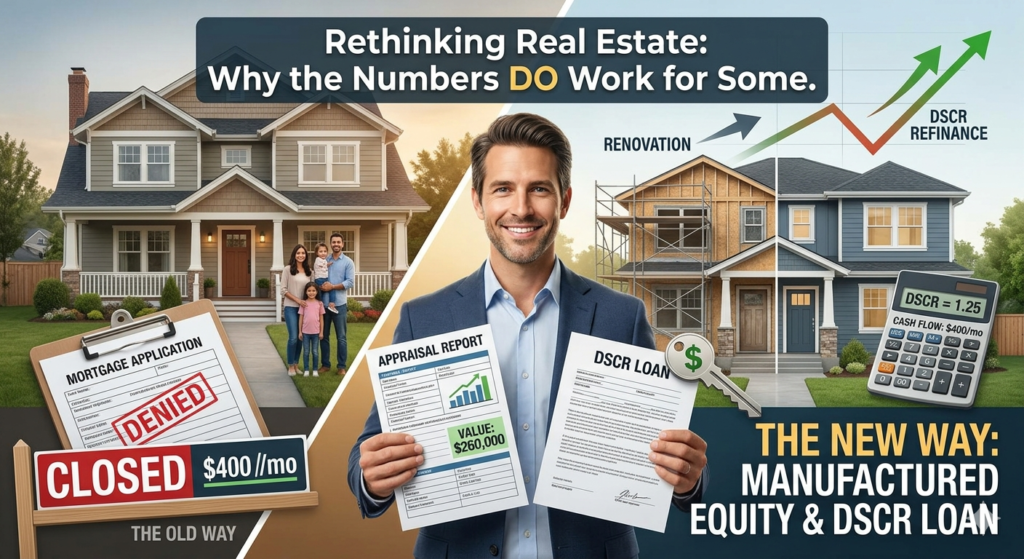

He picked it up for $110,000. Put $70,000 into a full rehab — both units, top to bottom. Total in: $180,000.

After the renovation, the property appraised around $260,000.

That’s $80,000 of manufactured equity. Value that didn’t exist before — built through the work, not handed over by the market.

Once both units were rented and cash flowing, he refinanced using a DSCR loan. That’s where things get interesting.

What is a DSCR loan, and why does it matter?

DSCR stands for Debt Service Coverage Ratio. It’s a type of loan designed specifically for investors — and the way it works is completely different from a conventional mortgage.

With a normal loan, the bank wants to see your personal income. Your tax returns, your pay stubs, your debt-to-income ratio. If you’re self-employed, own multiple properties, or just don’t show a lot of income on paper, getting approved gets complicated fast.

A DSCR loan doesn’t care about any of that.

Instead, lenders look at one simple question: does the property make enough money to cover its own mortgage?

The formula is straightforward:

DSCR = Monthly Rental Income ÷ Monthly Debt Service (mortgage payment)

Most lenders want to see a DSCR of 1.25 or higher. That means your property is bringing in 25% more than it costs to finance — which gives the lender confidence that even with a vacancy or a slow month, you can still make the payment.

In this duplex example, once both units are rented, the projected gross rent comes in around $2,200/month. After refinancing into a DSCR loan at current rates, the debt service comes out comfortably under that. The property essentially qualifies itself.

That’s the power of this structure. Personal income is irrelevant. The deal either works or it doesn’t — and you know before you close.

Why this matters more than people realize

The reason most investors hit a ceiling is because conventional financing eventually stops working. Banks get nervous about your debt load. Your DTI gets too high. Approvals slow down or stop.

DSCR loans sidestep that entirely. Each property stands on its own merits. As long as the numbers work, you can keep going.

The investor in that video started this year with 19 units. He’s at 33 now. That kind of growth doesn’t happen by waiting for rates to drop or hoping the market softens. It happens by understanding how the tools work and using the right one for the job.

The market isn’t the problem

Deals exist. They always have. The question is whether you know where to look and whether you know how to run the numbers.

The market doesn’t filter for strategy. It just exists. It’s your job to come in with the right framework — and right now, for investors buying distressed properties and forcing equity through rehab, DSCR financing is one of the most powerful tools available.

The numbers work. Just not for everyone.