I have a confession. When I drive past a beat-up motel on the side of the highway — peeling paint, half the sign letters missing, parking lot cracked — I don’t see an eyesore. I see a deal.

This probably says something about me. But the more I study commercial real estate, the more I think that reaction is actually correct.

Here’s why old motels and extended stay hotels might be one of the most underrated investment opportunities sitting in plain sight along American highways.

The Extended Stay Model: What It Is and Why It Works

An extended stay property is somewhere between a hotel and an apartment. Guests typically rent by the week or month rather than by the night. Rooms usually include a small kitchen or kitchenette. And the target tenant is someone who needs temporary housing — a traveling worker, someone between apartments, a family in transition.

In Korea, there’s a concept called “daesilbang” — short-term rental spaces that serve multiple purposes throughout the day, maximizing revenue per square foot. The extended stay model in the U.S. has some of that same logic: one physical space, multiple revenue streams, higher utilization than a traditional apartment.

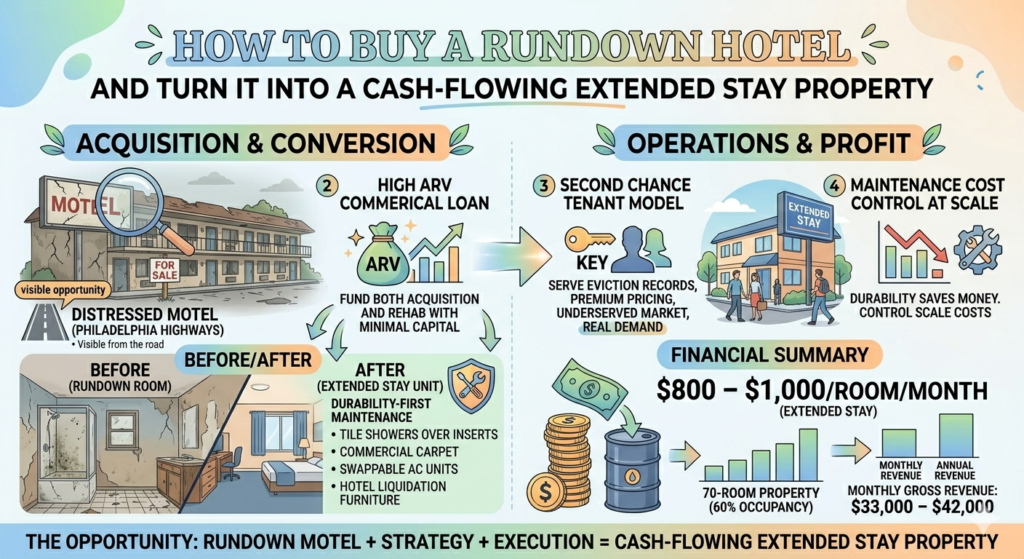

The numbers work differently than single-family rentals. A 70-room property generating $800–$1,000 per room per month is $56,000–$70,000 in gross monthly revenue. Even at 60% occupancy, that’s $33,000–$42,000/month coming in. From one property.

The Hotel Flip: How One Investor Bought a 70-Room Disaster and Made It Work

Let me walk through a real deal that illustrates exactly how this strategy works in practice.

A 70-room motel — one of the worst-condition properties you’d ever want to walk through — was acquired for $1.2 million. That’s roughly $17,000 per room. The renovation budget was $1 million. Total all-in cost: approximately $2.2 million.

The financing: The entire acquisition and renovation was funded through a hard money lender. The investor brought essentially nothing but closing costs to the table. How? Because the commercial appraisal — based on projected income after renovation — supported a loan large enough to cover both purchase and rehab.

This is the key difference between commercial and residential financing. Residential loans are based on comparable sales. Commercial loans are based on income. If your post-renovation income projections support a high enough value, the loan follows.

The projected outcome: Post-renovation, the property is expected to appraise at $3.5 to $4.5 million — based on projected income at stabilized occupancy. That’s a per-room value of $50,000 to $65,000, compared to the $17,000 acquisition cost.

The investor put in essentially none of their own money and created $1.3 to $2.3 million in equity.

The “Second Chance” Tenant Model

Here’s the part of this strategy that I find both clever and genuinely useful.

The target tenant for this property is someone with an eviction record. Someone who can’t get approved for a standard apartment because of their rental history — but who has income, wants stable housing, and is willing to pay a premium for access to it.

This is a real and underserved market. The standard apartment screening process excludes a significant portion of working adults who had one bad situation years ago. Extended stay properties can serve that population at rates below comparable apartments — and still generate strong cash flow because of the volume.

The legal structure: By structuring occupants as “guests” rather than “tenants” — through week-to-week or month-to-month hotel-style agreements — the property operates under hospitality law rather than landlord-tenant law. In most states, this significantly simplifies the removal process if a guest creates problems.

This isn’t a loophole or a way to exploit people. It’s a legitimate legal structure that hotels and extended stay properties use industry-wide. But it does require proper setup — the right licensing, the right contracts, and ideally a real estate attorney familiar with hospitality law in your state.

The Maintenance Cost Strategy That Actually Makes This Profitable

Most people who hear “70-room property” think “70 times the maintenance headaches.” And if you run it like a standard hotel, they’re right.

The investors who make extended stay work use a completely different approach to maintenance — one built around durability, replaceability, and speed.

Prioritize systems over aesthetics. Before anything cosmetic gets touched, the plumbing and electrical need to be right. Specifically — upgrading drain lines to handle high-volume simultaneous use. A 4-inch sewer line that works fine for a single-family home is a liability when 70 people are using it at the same time.

Choose materials that don’t break. Standard insert shower units crack and discolor. Tile holds up. Standard carpet stains and wears. Commercial-grade carpet is designed for exactly this kind of use. The upfront cost difference is modest. The maintenance cost difference over five years is enormous.

Build a replacement system, not a repair system. Wall unit air conditioners cost $300–$400 each. When one fails, don’t call a repair technician and wait three days — have a staff member swap it out in 20 minutes and send the broken unit for repair later. Speed of response matters more than unit cost at this scale.

Source furniture from hotel liquidations. When major hotel chains renovate, they liquidate their existing furniture — beds, dressers, microwaves, refrigerators — at a fraction of replacement cost. These are commercial-grade items built for exactly the use case you need. Buying 70 sets of furniture at liquidation prices versus retail is a significant cost difference.

What This Looks Like Near Philadelphia

If you’ve driven I-95 through Delaware County, or Route 1 through Montgomery County, or really any major highway corridor in the Philadelphia metro — you’ve seen the properties I’m talking about.

Older motels built in the 1960s and 70s. Some still operating at low occupancy. Some partially vacant. Some with ownership that’s been managing the same asset for 30 years and is ready to exit.

These properties trade at prices that would never work for a Class A hotel brand — but work very well for an extended stay conversion targeting the working-class market.

What to look for:

- Properties with strong bones (structural integrity, functional plumbing and electrical systems)

- Locations near employment centers — hospitals, warehouses, manufacturing, construction sites

- Markets with housing affordability pressure (extended stay demand correlates strongly with high housing costs)

- Properties with ownership that’s been in place for 10+ years and might be motivated to exit

The commercial real estate data platforms — CoStar, LoopNet, and even Crexi — list hospitality properties. Filtering for older, lower-rated properties in the Philadelphia metro gives you a starting list worth analyzing.

The Honest Risks

This is not a strategy for someone who wants passive income and minimal involvement. Let’s be clear about that.

Management intensity is real. A 70-room extended stay property with working-class guests is not a luxury short-term rental. There will be disputes. There will be guests who need to be removed. There will be maintenance calls at inconvenient hours. On-site staff is not optional — it’s essential.

Insurance and property taxes are rising. In many markets, commercial property insurance premiums have increased dramatically over the last few years. Property taxes on commercial assets are reassessed frequently. Both of these costs directly reduce cash flow and need to be modeled carefully before acquisition.

Licensing requirements vary. Operating as a hotel, motel, or extended stay facility requires hospitality licensing that varies significantly by state and municipality. Pennsylvania has its own hotel licensing requirements. Philadelphia has additional layers. Get clear on what’s required before you buy, not after.

The learning curve is steep. This is a commercial real estate investment that also functions as an operating business. You’re not just a landlord — you’re running a hospitality operation. The investors who do this well either have hospitality experience or partner with someone who does.

Why I Keep Coming Back to This Idea

I’ll be honest about where I am with this. I’m not buying a 70-room motel tomorrow. My current path runs through single-family flips, then small multifamily, then larger commercial.

But the extended stay model keeps pulling at me because the math is compelling in a way that residential real estate often isn’t. The per-unit revenue is higher. The commercial valuation methodology rewards operational improvement directly. And the supply of distressed hospitality assets along American highway corridors is real and visible.

The motel sitting half-empty on Route 1 isn’t just a sad building. It’s a capitalization rate problem waiting for someone with the right knowledge and the right team to solve it.

That’s the opportunity.

Not financial advice — just someone doing a lot of research and asking a lot of questions.