I’ve been watching a lot of Section 8 investing content lately. And I’ll be honest — some of it sounds incredibly compelling.

Buy a house under $100,000. Register with your local housing authority. Let the government pay you rent every month. Repeat until financially free.

Simple. Safe. Guaranteed income.

Then I found a video from a landlord who’s owned 350 properties over 22 years — 120 of them Section 8. And he had some things to say about those YouTube promises that I couldn’t ignore.

Here’s what’s actually true, what’s exaggerated, and what you need to know before you buy your first Section 8 property.

What Section 8 Actually Is

The Housing Choice Voucher Program — commonly called Section 8 — is a federal rental assistance program administered by local Public Housing Authorities (PHAs). Qualified low-income tenants receive vouchers that cover a portion of their rent. The landlord receives that portion directly from the government every month.

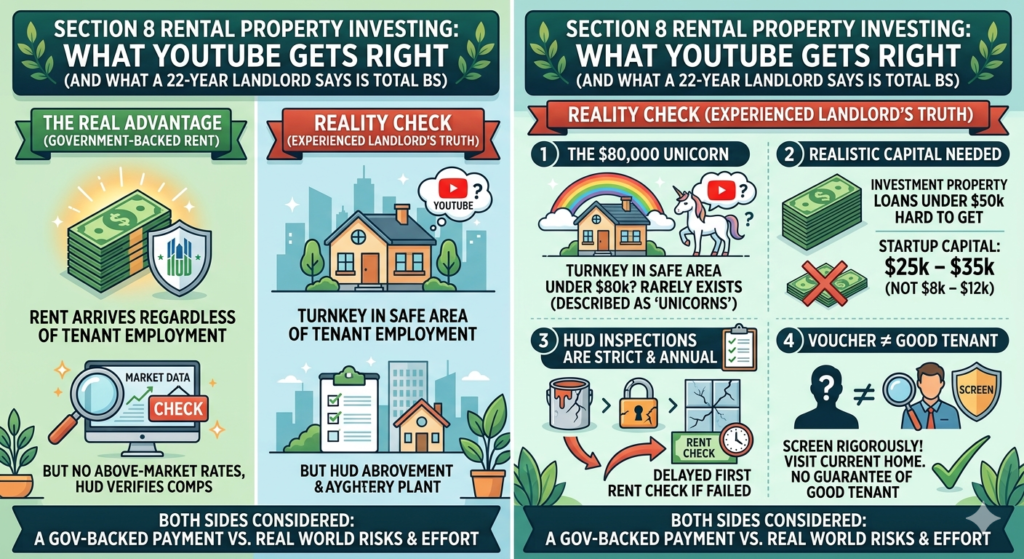

The appeal for landlords is real: government-backed rent that arrives reliably regardless of the tenant’s employment situation. If a Section 8 tenant loses their job, your check from the housing authority still comes in.

That’s a genuine advantage. The question is whether the rest of the pitch holds up.

The YouTube Version: $100K and Under

Here’s the basic strategy as it’s typically presented online:

- Search Zillow for 3-bedroom homes priced between $40,000 and $90,000

- Look for turnkey or near-turnkey condition

- Use seller financing to minimize down payment

- Register with your local housing authority

- Collect government-backed rent of $800–$1,000/month

- Cash flow $400–$600/month after expenses

- Repeat

The math looks clean. The pitch is compelling. And some of it is actually true.

What’s accurate:

- Section 8 rent does arrive reliably from the government

- Vacancy risk is genuinely lower — Section 8 waitlists are long and voucher holders want to keep their housing

- Seller financing can reduce upfront capital requirements

- Properties under $100,000 do exist in many markets

What gets glossed over: Almost everything else.

What the 22-Year Landlord Actually Says

Let’s go through the specific claims that experienced investors push back on.

“The government pays 10–30% above market rent.”

Not how it works. Housing authorities calculate Fair Market Rent (FMR) based on actual comparable rents in the area. They verify comps. If you try to charge above what the market supports, they won’t approve it. You might get market rate — which is fine — but you’re not getting a government premium just for participating.

“Turnkey homes under $80,000 exist in safe neighborhoods.”

These are described by one 22-year veteran as “unicorns.” Properties in that price range that are genuinely turnkey and in neighborhoods with acceptable crime rates are extremely rare. What actually exists at that price point in most markets are properties that need significant work — and properties built before 1978, which bring lead paint requirements that can create real problems during HUD inspections.

“Banks will finance $50,000 investment properties.”

Most conventional lenders won’t touch investment properties under $50,000. The loan amount is too small to be worth their underwriting cost. You’re looking at portfolio lenders, community banks, or seller financing — all of which are available but require more work to access than a standard mortgage application.

“You only need $8,000–$12,000 to get started.”

Investment property loans typically require 20–25% down, not 15%. On an $80,000 property, that’s $16,000–$20,000 — plus closing costs, plus any repairs needed to pass HUD inspection. The real number is closer to $25,000–$35,000 for a legitimate deal with appropriate reserves.

“Tenants stay an average of 7.5 years.”

No solid data supports this specific claim. Turnover varies enormously by market, property condition, and tenant screening quality.

The HUD Inspection Reality

This is the part that trips up the most new Section 8 landlords.

Before a voucher holder can move into your property, a HUD inspector has to approve it. The inspection covers safety, habitability, and condition standards — and it is strict.

Door locks that don’t function properly. Cracked tiles. Chipped paint (especially in pre-1978 homes where lead paint is a concern). Missing outlet covers. Window issues. Any of these can fail an inspection and delay your first rent check by weeks or months while you make repairs and schedule a reinspection.

And this isn’t a one-time hurdle. Annual inspections are required to maintain your Section 8 status. A property that passes one year can fail the next if maintenance has slipped.

The experienced landlord’s point: many property management companies refuse Section 8 properties specifically because of the inspection complexity and ongoing administrative requirements. If you’re planning to invest out of state and hire a property manager, your pool of qualified managers is smaller than you’d expect.

What Both Sides Agree On: Tenant Screening

Here’s where the YouTube optimists and the 22-year veteran actually agree.

A Section 8 voucher does not guarantee a good tenant. It guarantees a government payment — which is different.

The tenant screening process for Section 8 should be just as rigorous as for any other rental — credit check, criminal background, eviction history, references. And experienced Section 8 landlords add one more step that most beginners skip:

Visit the tenant’s current home.

If a prospective tenant keeps their current place clean — lawn maintained, interior tidy, no obvious damage — that tells you something. If you show up and the current place is trashed, that tells you something too. People treat their homes the way they treat their homes. The Section 8 voucher doesn’t change that.

The mistake is assuming the government payment eliminates tenant risk. It reduces one specific type of risk (non-payment from the tenant’s portion). It doesn’t eliminate maintenance risk, damage risk, or the complexity of managing someone who isn’t working out.

Is Section 8 Investing Worth It?

Yes — with the right expectations.

Section 8 is a legitimate strategy that experienced landlords use as part of diversified portfolios. The government-backed income is a real advantage. The low vacancy risk is real. The ability to serve tenants who are genuinely grateful for quality housing and tend to stay long-term is real.

What it isn’t is a passive income machine that runs itself with minimal capital and effort. The YouTube version of Section 8 investing — buy cheap, collect checks, repeat — omits the inspection complexity, the financing reality, the property condition requirements, and the ongoing management intensity.

For a first-time investor in Philadelphia:

Properties in the $60,000–$100,000 range do exist in North Philadelphia and parts of West Philadelphia. Section 8 is active in those markets. The Fair Market Rents for Philadelphia are publicly available on HUD’s website and are worth reviewing before you run any numbers.

But go in with your eyes open. Budget for 20–25% down plus reserves. Understand the inspection process before you buy. Screen tenants as carefully as you would for any rental. And don’t count on a property management company to handle the Section 8 paperwork without first confirming they actually do it.

The strategy works. The pitch is oversimplified