Fannie Mae Freddie Mac explained simply — these names pop up constantly in mortgage research and most people nod along like they understand, then quietly Google it later.

I was one of those people for a long time. So let me explain it the way I wish someone had explained it to me.

Why These Organizations Exist: The Problem Before Fannie Mae Freddie Mac

To understand Fannie, Freddie, and Ginnie, you need to understand a problem that almost killed American homeownership in the 1930s.

During the Great Depression, banks were terrified to lend money. If they made a 30-year mortgage loan, that money was tied up for three decades. Banks needed liquidity — cash on hand to keep operating. So they either stopped lending entirely or only offered short-term loans with huge balloon payments that most people couldn’t afford.

The result: homeownership collapsed. The housing market froze.

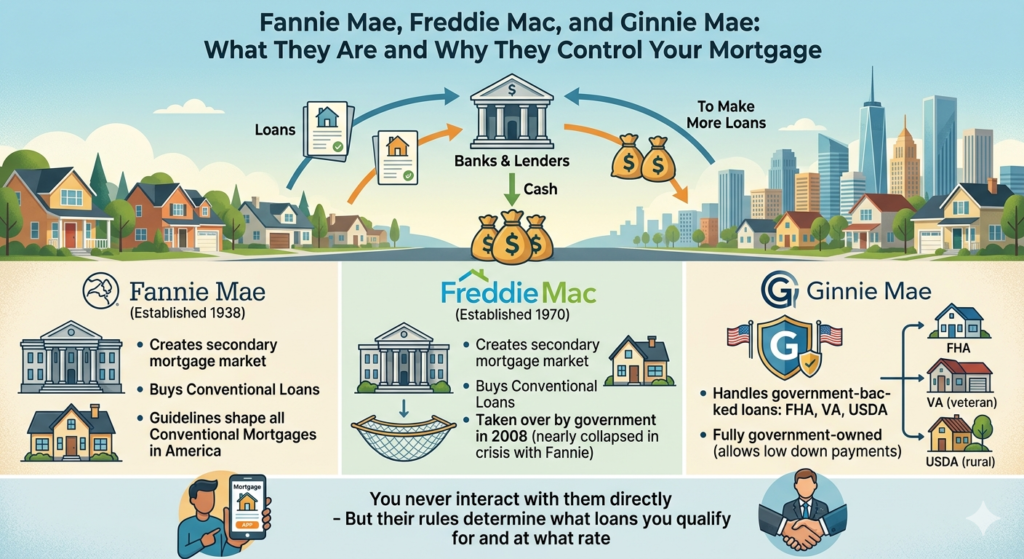

The government’s solution was to create a secondary mortgage market. Instead of banks holding loans for 30 years, they could sell those loans to a government-backed entity — get their cash back immediately — and then turn around and make more loans.

That’s the entire reason these organizations exist. They’re the buyers of last resort in the mortgage market. They keep money flowing so banks keep lending.

Fannie Mae Freddie Mac Explained: Fannie Mae First

Founded: 1938, by Franklin D. Roosevelt as part of the New Deal

Full name: Federal National Mortgage Association

Fannie Mae buys conventional mortgages from lenders — banks, credit unions, mortgage companies — packages them into mortgage-backed securities, and sells those securities to investors on Wall Street.

Here’s the flow:

- You get a mortgage from your local bank

- Your bank sells that mortgage to Fannie Mae

- Your bank gets cash back and makes more loans

- Fannie Mae bundles your mortgage with thousands of others

- Investors buy those bundles as securities

You still make your payment to your bank. But behind the scenes, Fannie Mae owns the loan.

Why Fannie Mae’s rules matter to you: Fannie Mae only buys loans that meet its standards — credit score minimums, debt-to-income limits, loan size limits, property requirements. When lenders know Fannie Mae will buy a loan, they’ll make it. When they know Fannie won’t touch it, they often won’t make it either.

So when Fannie Mae changes its standards — like allowing 5% down on multifamily properties — banks across the country adjust their products accordingly. Fannie Mae doesn’t lend to you directly. But it shapes almost every conventional loan you’ll ever apply for.

Fannie Mae Freddie Mac Explained: Freddie Mac

Founded: 1970, by Congress

Full name: Federal Home Loan Mortgage Corporation

Essentially the same thing as Fannie Mae. Buys mortgages, packages them, sells them to investors.

So why does it exist? By 1970, Fannie Mae had grown enormous. Congress got nervous about one entity controlling the entire secondary mortgage market. So they created Freddie Mac as a competitor — to provide checks and balances and keep the market from being monopolized.

In practice, Fannie and Freddie operate very similarly. They have slightly different loan products and guidelines, but for most borrowers the difference is invisible. Your lender might sell your loan to either one.

The 2008 moment: Both Fannie Mae and Freddie Mac took on massive risk during the housing bubble by buying up subprime mortgage-backed securities. When the market collapsed in 2008, both were on the verge of failure. The federal government placed both into conservatorship — essentially a government takeover. They’ve been under federal control ever since.

Ginnie Mae: The Actually Government-Owned One

Founded: 1968, spun off from Fannie Mae

Full name: Government National Mortgage Association

Same general concept — securitizes mortgages and sells them to investors. But with one crucial difference.

Ginnie Mae only deals with government-backed loans: FHA loans, VA loans, USDA loans. Not conventional mortgages.

And unlike Fannie Mae Freddie Mac, Ginnie Mae is a fully government-owned corporation — part of HUD. The securities it issues carry an explicit U.S. government guarantee. If the underlying loans default, the government covers investors.

This is why FHA and VA loans can be offered with low down payments and relaxed credit requirements — Ginnie Mae’s government guarantee reduces the risk enough that investors will buy those securities even when the underlying loans are riskier.

Fannie Mae Freddie Mac Explained: Side by Side

| Fannie Mae | Freddie Mac | Ginnie Mae | |

|---|---|---|---|

| Founded | 1938 | 1970 | 1968 |

| Loan type | Conventional | Conventional | FHA, VA, USDA |

| Government owned? | No (conservatorship) | No (conservatorship) | Yes (fully) |

| Direct lending? | No | No | No |

What This Means for You as a Borrower

You will probably never interact with any of these organizations directly. But their rules determine what loans are available to you.

Conventional loan — Fannie Mae or Freddie Mac guidelines apply. Credit score, debt-to-income ratio, loan limits, property standards — all shaped by these two.

FHA or VA loan — Ginnie Mae is in the background. The more flexible credit requirements and low down payments are possible because of the government guarantee Ginnie Mae provides.

Loan limits: Both Fannie and Freddie set conforming loan limits — the maximum loan size they’ll purchase. In 2026, the conforming limit for a single-family home in most areas is around $766,550. Loans above these limits are called jumbo loans — they follow different rules entirely because Fannie Mae Freddie Mac won’t buy them.

According to HUD.gov, the secondary mortgage market created by Fannie Mae, Freddie Mac, and Ginnie Mae funds the vast majority of American home loans — making these organizations the invisible backbone of homeownership in the United States.

The Part I Find Most Interesting About Fannie Mae Freddie Mac

You walk into a bank, you get a mortgage, you make payments. You never think about Fannie Mae. But Fannie Mae’s guidelines determined whether you qualified. Fannie Mae’s appetite for risk shaped the interest rate you got. And within weeks of closing, Fannie Mae probably owns your loan — even though your bank is still collecting your payment.

The secondary mortgage market is the plumbing of American homeownership. Most people never see it. But when it breaks — like it did in 2008 — everything breaks with it.

Understanding who these organizations are and what they do makes you a more informed borrower. And when one of them changes a policy — like Fannie Mae’s recent move to allow 5% down on multifamily properties — you understand why it matters and how to use it.

Use the Mortgage Calculator to model your loan options — conventional (Fannie/Freddie) vs FHA (Ginnie) — and see exactly how the down payment and rate differences affect your monthly payment.

Not financial advice — just someone doing a lot of research and asking a lot of questions.