I used to think getting a loan for an investment property worked the same way as getting a mortgage for your house. You know — dig up two years of tax returns, prove your income, explain every deposit in your bank account for the last 12 months, and hope the underwriter is having a good day.

Then I found out about fix & flip loans. And honestly? It changed the way I think about real estate financing entirely.

The Bank Problem Nobody Talks About

Here’s something that struck me recently. If you walk into a traditional bank and say “I have $20,000 to $30,000 and I want to buy an investment property,” they’re going to grill you. Where did that money come from? Can you prove your income? What’s your debt-to-income ratio?

But if you walk in trying to finance a $20 million commercial property with $5 million down? Suddenly everyone’s very accommodating.

It’s not a conspiracy theory — it’s just how the system is built. Traditional banks are designed for W-2 employees with steady paychecks and clean paper trails. They’re not really designed for someone who’s trying to build wealth through real estate one deal at a time.

Which is exactly why fix & flip loans exist.

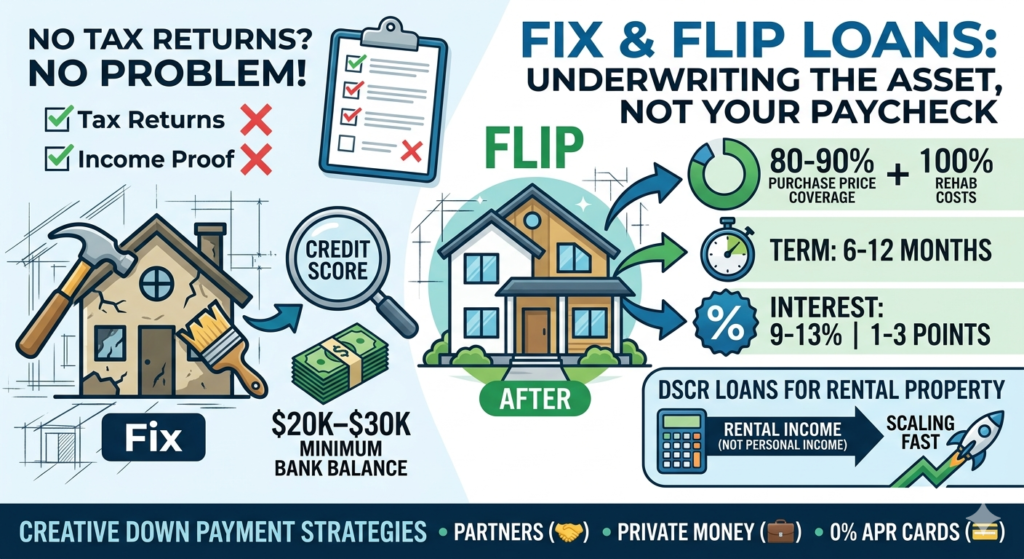

What Is a Fix & Flip Loan, Actually?

A fix & flip loan (sometimes called a hard money loan or bridge loan) is a short-term loan designed specifically for investors who are buying a property, rehabbing it, and selling it — usually within 6 to 12 months.

The biggest difference from a conventional mortgage? They don’t ask for your tax returns or proof of income.

Instead, what they care about is:

- The deal itself — specifically the ARV (after repair value)

- Your credit score (typically 650+ is workable, 680+ is better)

- How much cash you have in the bank — usually $20,000 to $30,000 minimum

- Your experience level (some lenders care more about this than others)

That’s it. They’re underwriting the asset, not your W-2.

Why Cash in the Bank Matters More Than Your Income

This part surprised me when I first learned it. Fix & flip lenders don’t need you to prove a salary — but they do want to see liquidity. The $20K to $30K in your account tells them you can cover holding costs, unexpected repairs, and loan payments while the project is running.

It’s actually a more logical way to evaluate a real estate investor when you think about it. Your tax return tells them what you made last year. Your bank balance tells them whether you can actually execute a deal right now.

For people who are self-employed, have irregular income, or structure their finances in ways that minimize taxable income (very common among small business owners), this is huge. You’re not being penalized for running your finances like an entrepreneur.

How Fix & Flip Loans Are Structured

Here’s the general structure you’ll see with most fix & flip lenders:

Loan-to-Cost (LTC): Many lenders will finance 80–90% of the purchase price plus 100% of the rehab costs, up to a certain percentage of ARV — usually 65–75% of ARV total.

Interest rates: Higher than conventional — typically 9–13% depending on the lender, your credit, and the deal.

Points: Expect 1–3 points upfront (1 point = 1% of the loan amount).

Term: Usually 6 to 12 months, sometimes up to 18.

Draws: Rehab funds are typically released in draws as work is completed, not all at once.

So yes, it costs more than a bank loan. But for a deal that’s going to close in 6 months with $40,000 in profit, paying an extra few thousand in interest is just a cost of doing business.

DSCR Loans: The Other Side of the Equation

Fix & flip loans are for short-term plays. But what if you want to hold the property as a rental? That’s where DSCR loans come in.

DSCR stands for Debt Service Coverage Ratio. Instead of looking at your personal income, these loans look at whether the rental income from the property can cover the mortgage payment.

The formula: Monthly Rent ÷ Monthly Mortgage Payment = DSCR

A DSCR of 1.0 means rent exactly covers the payment. Most lenders want to see 1.1 to 1.25. Some will go down to 0.75–0.80 for strong borrowers.

What lenders focus on with DSCR:

- Your credit score

- The property’s rental income (or market rent estimate)

- Cash reserves

- Your debt-to-income ratio? Largely irrelevant.

Big institutional investors — the kind buying hundreds of rentals at a time — have been using DSCR loans for years. It’s one of the reasons they can scale so fast. Individual investors are now using the same tool.

What About Getting the Down Payment Together?

This is where people get creative. One strategy that gets talked about — and I want to be clear this requires knowing exactly what you’re doing — is using 0% intro APR credit cards to cover short-term costs.

Some investors use business credit cards with 0% intro periods (12–18 months) to fund repairs, cover holding costs, or bridge gaps while they’re waiting on a draw. If the flip closes before the intro period ends, you’ve essentially borrowed money for free.

The risk is obvious: if the deal takes longer than expected or the market softens, you’re sitting on high-interest credit card debt with no exit. This is not a beginner move.

More commonly, investors piece together down payments through:

- Personal savings

- A partner who brings capital while you bring the deal and sweat equity

- A private money lender (usually someone you know personally who wants a return on their cash)

- Home equity from a property you already own

Who Fix & Flip Loans Are Actually For

Fix & flip financing makes the most sense when:

- You’ve identified a good deal with real equity spread

- You have $20K–$30K+ in the bank

- Your credit is in decent shape (650+)

- You can manage or oversee a rehab project

- You have a clear exit — either sell or refinance into a DSCR loan

It’s not a magic solution. The higher cost of capital means you need a deal with enough margin to absorb it. But for investors who can’t qualify for conventional financing, it opens doors that would otherwise stay shut.

I’ve been studying this for a while now, and the thing that keeps standing out to me is this: the barrier to entry isn’t really the money. It’s knowing which type of financing fits which type of deal — and then finding a lender who works with investors at your level.

There’s a fix & flip loan calculator on this site if you want to run the numbers on a specific deal before you start calling lenders.

Not financial advice — just someone doing a lot of research and asking a lot of questions.