A real hard money deal teaches you more than any hypothetical ever will. Not “let’s say you buy a house for X” — actual numbers, actual outcomes, actual risk.

When I came across a video where a hard money lender walked through one of his client’s active flip projects with the full deal breakdown on screen, I watched it three times.

Here’s exactly what that hard money deal looked like — and what it taught me about how this financing actually works in the real world.

The Hard Money Deal Snapshot

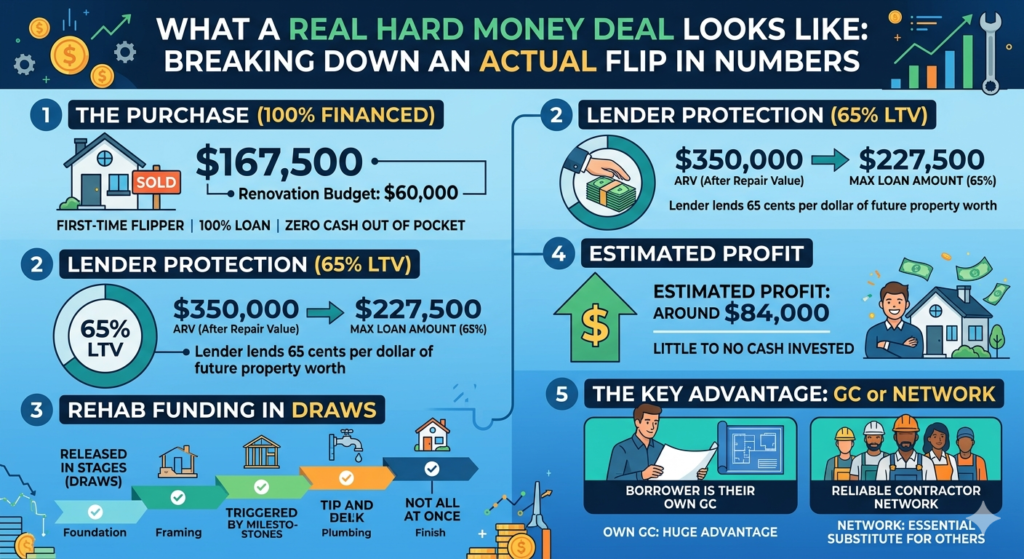

This was a first-time flipper’s project. Single family home on a dead-end street, strong resale market, good comps nearby.

| Line Item | Amount |

|---|---|

| Purchase Price | $167,500 |

| Renovation Budget | $60,000 |

| Total Loan Amount | $227,500 |

| After Repair Value (ARV) | $350,000 |

| Loan-to-Value (LTV) | 65% |

The part that gets people’s attention: 100% of both the purchase price and the renovation costs were financed through the hard money deal. The borrower didn’t bring cash to the table for either.

Wait — 100% Financed? How Does a Hard Money Deal Work Like That?

Hard money lenders don’t lend based on your credit score or income like a traditional bank. They lend based on the deal — specifically, the ARV.

In this hard money deal:

- Total loan: $227,500

- ARV: $350,000

- LTV: 65%

That 65% LTV is the key number. The lender is only lending 65 cents for every dollar the property will be worth after repairs. That’s their protection. If the borrower defaults and the lender has to take the property, they’re buying a $350K asset for $227K. They’re covered.

For the borrower, 100% financing means getting into a deal without tying up their own cash — which is exactly the kind of leverage that makes flipping accessible when you’re starting out.

What Was Actually Happening on Site

The lender visited the property for the first draw inspection — which is how hard money renovation loans work. You don’t get the full rehab budget upfront. You get it in stages called draws, released as you hit construction milestones.

At the time of this inspection:

- Demo was almost completely done

- Framing was starting in the basement

- Second floor was cleared and ready for the next phase

- Project was moving fast

The lender noted that the borrower being a GC himself was a major advantage — he knew how to manage the work, keep momentum going, and hit the milestones needed to trigger each draw.

This matters a lot. Which is why finding a reliable contractor before you start is so critical — and why the draw system in a hard money deal actually protects both sides.

The Math If This Hard Money Deal Goes to Plan

| ARV (sale price) | $350,000 |

| Total loan payoff | $227,500 |

| Hard money interest (est. 12% for 6 months) | ~$13,650 |

| Closing costs + agent fees (est. 7%) | ~$24,500 |

| Estimated profit | ~$84,000 |

Roughly $84K profit on a deal where the borrower put in little to no cash of their own.

Obviously this assumes the renovation stays on budget, the ARV holds, and the timeline doesn’t drag. All real risks. But the structure — 65% LTV, strong comps, experienced operator — gives this hard money deal a solid foundation.

What This Hard Money Deal Teaches You About Evaluation

LTV is everything. 65% or below gives both the lender and borrower breathing room. If comps soften or renovation runs over, there’s still margin. Deals at 80%+ LTV leave almost no cushion.

The draw system protects everyone. You don’t get the rehab money all at once — you earn it in stages by completing work. This keeps the project moving and keeps the lender’s risk managed.

Being a GC — or knowing one really well — is a massive advantage. This borrower was his own GC. For the rest of us, having a reliable contractor relationship before you start is the closest thing to that advantage.

Hard money is expensive — but it’s speed and access. Traditional loans take 30–60 days and require income documentation. A hard money deal can close in days and doesn’t care about your W-2. For flips where timing matters, that premium is often worth it.

According to BiggerPockets, hard money loans typically run 10–15% interest with 1–3 points — but the ability to close fast and finance 100% of a deal at the right LTV makes them the go-to tool for experienced flippers.

Applying This to Philadelphia

Philadelphia has an active hard money lending market. Local lenders know the market, understand Philly comps, and have funded deals in Germantown, Kensington, Brewerytown, and beyond.

The key is finding deals where the ARV is strong enough to support the loan structure. In Philly’s current market, that means doing your comp research carefully — knowing what renovated properties are actually selling for in that specific neighborhood, not just the zip code.

Run the numbers before you talk to a lender. Know your purchase price, your renovation estimate, and your ARV. Walk in with a deal, not a question.

Use the Hard Money Loan Calculator to model your full deal — interest costs, draw schedule, and projected profit — before you make an offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions.