Wraparound mortgage. Subject To. Owner financing. I kept seeing these terms on TikTok and YouTube and had absolutely no idea what they actually meant.

A wraparound mortgage sounds complicated — and honestly, parts of it are. But once you understand the basic structure, it changes how you look at every conversation with a motivated seller.

Here’s the guide I wish I had when I first started. No jargon. No hype. Just honest explanations — including the parts that made me go “wait, but what if the seller just disappears?”

Why Wraparound Mortgages and Creative Financing Exist

Traditional financing has a real problem right now.

Interest rates are around 6.5–7%. A lot of buyers can’t qualify for a bank loan. A lot of sellers are stuck with properties they can’t easily move. Creative financing — including wraparound mortgages and Subject To deals — exists to solve these problems by cutting the bank out of the equation entirely and letting buyers and sellers make their own deals.

That sounds great in theory. Here’s how it actually works.

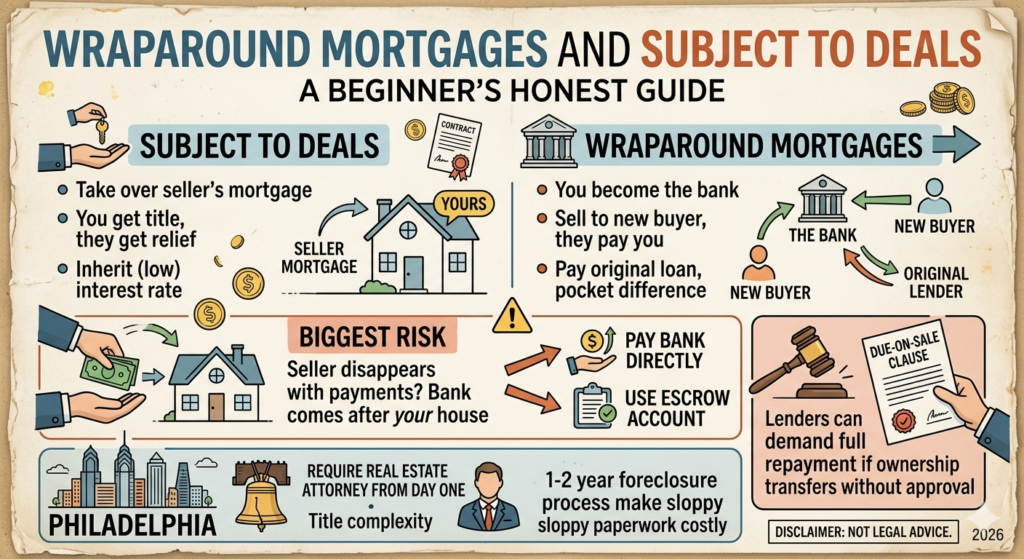

Subject To: You Take Over Someone Else’s Mortgage

Imagine a seller who’s in trouble. They’ve missed six months of mortgage payments, foreclosure is coming, and their credit is about to get destroyed.

They owe $225,000 on the house. The mortgage rate is 2.99% — locked in from when rates were low. Monthly payment: $1,500.

You come along and offer them $10,000 cash. In exchange, you take over their mortgage payments. The loan stays in their name, but the house title transfers to you. You make the $1,500 payment every month going forward.

That’s a Subject To deal.

Why would a seller agree to this? Because they’re desperate. They’re getting relief from a debt that’s about to destroy their credit. For someone in that situation, $10,000 and someone taking over their payments can feel like a lifeline.

Why is this attractive to a buyer? That 2.99% mortgage. You can’t get anywhere near that rate today. By taking over this loan, you’re inheriting a financing structure that no longer exists in the market.

Wraparound Mortgage: When You Become the Bank

Now here’s where it gets interesting — and where I had the most questions.

Let’s say you did that Subject To deal. You’re now making payments on a house worth $225,000. Instead of just holding it, you want to sell it. But instead of a normal sale, you create a wraparound mortgage.

You sell the house to a new buyer for $275,000. They can’t get a bank loan — maybe their credit isn’t great, or they’re self-employed and can’t prove income. So you offer to finance it yourself. They pay you $2,500/month directly.

Here’s the money flow in a wraparound mortgage:

| New buyer pays you | $2,500/month |

| You pay original bank | $1,500/month |

| Your monthly profit | $1,000/month |

The original loan is the “inner” loan. Your new loan to the buyer is the “outer” loan — it wraps around the original one. That’s why it’s called a wraparound mortgage.

The Questions I Actually Had About Wraparound Mortgages

“What if the seller takes my money and doesn’t pay the bank?”

This was my first question. And it’s a real risk. If you’re paying the seller and they pocket everything and disappear, the bank comes after the house — your house — even if you’ve been paying on time.

The solution: pay the bank directly. With the seller’s written permission, you set up payments straight to the bank — bypassing the seller entirely.

“How do you protect everyone?”

An escrow account. A neutral third party — a lawyer or escrow company — sits in the middle, receives your payment, automatically pays the bank, and sends the seller their cut. Everyone gets what they’re owed. Nobody can run off with the money. It costs extra, but it’s worth it on any wraparound mortgage deal.

“Is this even legal?”

Yes — but there’s a legal landmine called the due-on-sale clause. Most mortgages say: if you sell or transfer the property, the lender can demand the entire loan balance immediately. In a Subject To or wraparound mortgage deal, you’re technically transferring ownership without paying off the loan — which could trigger this clause.

In practice, lenders usually don’t enforce it as long as payments keep coming in. But “usually don’t” is not the same as “can’t.” It’s a real risk you need to understand before you do this. According to the Consumer Financial Protection Bureau, due-on-sale clauses are standard in most conventional mortgages and are legally enforceable — even if rarely triggered.

Who Actually Does Wraparound Mortgage Deals?

On the buyer side — investors who understand creative financing and can find motivated sellers.

On the seller side — people in genuine distress. Facing foreclosure. Going through divorce. Inherited a property they don’t want. Behind on taxes. They need out more than they need full market value.

On the new buyer side — people who want to own a home but can’t get traditional financing. Self-employed buyers, people rebuilding credit, people who need flexibility that banks won’t give them.

When all three pieces align, a wraparound mortgage deal makes sense. When they don’t — when you’re trying to force the structure on a situation that doesn’t fit — it gets messy fast.

Wraparound Mortgage Strategy in Philadelphia

Philadelphia has motivated sellers. Estate sales, tax-delinquent properties, inherited rowhouses that out-of-state heirs just want gone. The ingredients exist here.

But Philadelphia also has complicated title histories. And the foreclosure process in Pennsylvania takes 1–2 years if a buyer stops paying you. That’s 1–2 years of carrying costs while you fight to get your property back.

If you’re going to try a wraparound mortgage or Subject To deal in Philly — and I’m not saying don’t — you need a real estate attorney from day one. Not optional. The paperwork has to be airtight.

Use the Subject To Calculator to model your monthly cash flow before you structure any deal — so you know exactly what the numbers look like before anyone signs anything.

Not financial advice — just someone doing a lot of research and asking a lot of questions.