I keep seeing this claim everywhere on real estate social media.

“No money down.” “Zero out of pocket.” “You don’t need credit or cash to start investing.”

And every time I see it, part of me wants to believe it — and part of me is skeptical. So I actually looked into it. Here’s what I found.

First — What Is a Hard Money Loan?

Hard money lenders are private lenders — not banks — who loan money based on the value of the property, not your personal credit score or income history.

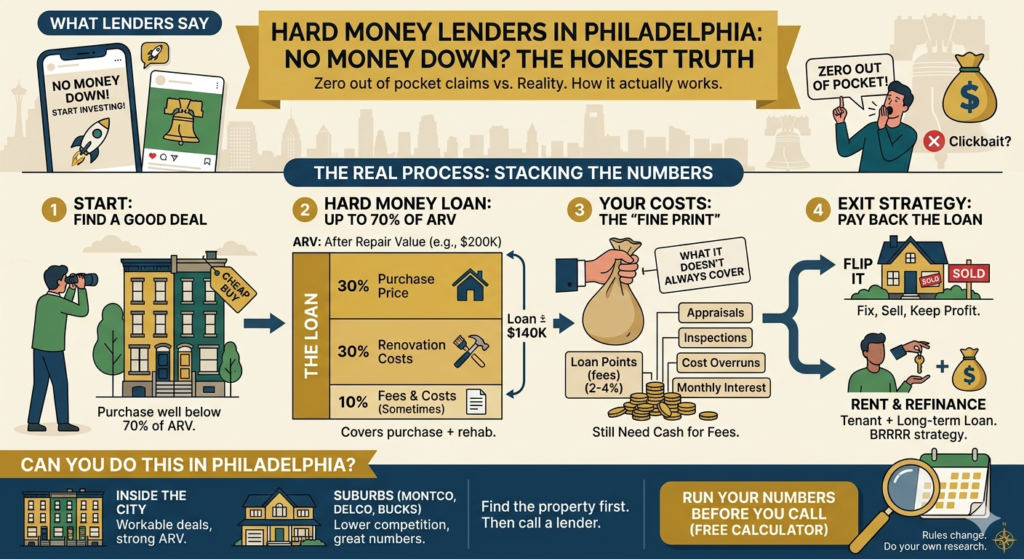

The key number they care about: ARV (After Repair Value). What will this property be worth after it’s fixed up?

Most hard money lenders will loan up to 70% of ARV. So if a house will be worth $200,000 after renovation, they’ll lend you up to $140,000 — which can cover both the purchase price and renovation costs if you bought the property cheaply enough.

That’s the foundation of the “no money down” claim.

The Two Ways Out (Exit Strategies)

Hard money loans are short term — usually 3 to 6 months, with interest rates around 10–14%. You need a plan to pay them back. Two main options:

Flip it: Fix it up, sell it, pay off the loan, keep the profit. Clean and simple — if the numbers work.

Rent it + Refinance: Get a tenant in, then refinance into a long-term conventional or DSCR loan. The long-term loan pays off the hard money loan, and now you own a rental property — potentially with little to none of your own money still in the deal.

This is basically the BRRRR strategy with hard money as the entry point.

So Is “No Money Down” Actually Real?

Kind of. Here’s the honest answer.

What hard money CAN cover:

- Purchase price (if you bought below 70% ARV)

- Renovation costs

- Sometimes closing costs

What it usually DOESN’T cover:

- Loan origination fees (points) — typically 2–4% of the loan amount

- Appraisal fees

- Inspection costs

- Cost overruns on renovation

- Monthly interest payments while you’re renovating

So “zero out of pocket” is an overstatement. But “dramatically less than a traditional mortgage”? That part is true.

Think about it this way — if a hard money lender covers a $120,000 purchase and $30,000 in renovation, and you need $5,000–$8,000 for fees and carrying costs? That’s a very different conversation than coming up with a $30,000 down payment for a conventional loan.

How to Find Hard Money Lenders in Philadelphia

This part is actually simple. Google “hard money lenders Philadelphia” and you’ll find plenty of options. There are also lenders who specifically work in Pennsylvania and the surrounding suburbs.

One important rule: find the property first.

Hard money lenders approve loans based on the deal — the property, the ARV, the renovation plan. Don’t call a lender with nothing to show them. Find a property that makes sense, run the numbers, then make contact.

What to Ask a Hard Money Lender

When you do call:

- What’s your max LTV? (Loan to value — how much of ARV will you lend?)

- Do you lend on purchase + rehab together?

- What are your points and fees?

- What’s the loan term?

- Do you require experience?

That last one matters. Some lenders won’t touch first-time investors. Others specialize in beginners. Know who you’re talking to before you start the conversation.

Philadelphia-Specific Reality Check

Inside the city, hard money deals can work — especially in neighborhoods where you can buy cheap and ARV is strong. Germantown, Kensington, parts of North Philly — there are deals if you know where to look.

In the suburbs (Montgomery County, Bucks County, Delaware County), the numbers often work even better. Lower competition, larger lots, and buyers willing to pay good prices for renovated homes.

The strategy is real. The “no money down” part is mostly real — with some fine print. And Philadelphia is one of the better markets in the Northeast to try it.

Run Your Hard Money Numbers Before You Call Anyone: