I’ll be honest — the first time I heard someone say they bought a $1.2 million property without spending a single dollar of their own money, I thought it was one of those things people say to sell courses.

Then I heard the full story. And I couldn’t stop thinking about it.

The Deal

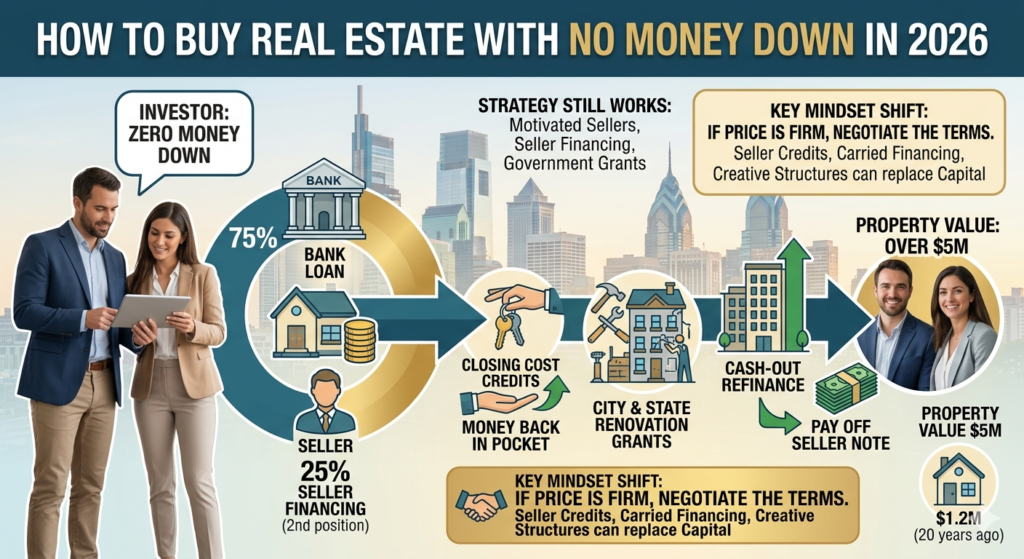

About 20 years ago, a real estate investor purchased a $1.2 million property with zero of his own capital. Not a small rental. Not a fixer-upper in a cheap market. A $1.2 million asset.

That property is now worth over $5 million.

Here’s exactly how he structured it.

The Financing Stack

He didn’t find some secret loophole. He stacked three things that already existed:

1. Bank Loan — 75%

A conventional commercial lender covered 75% of the purchase price. This is standard. Banks do this every day.

The problem was the remaining 25% — roughly $300,000 — that he didn’t have.

2. Seller Second Position Note — 25%

Instead of coming to the table with $300,000 cash, he negotiated with the seller directly.

He asked the seller to carry the remaining 25% as a second position note — essentially, the seller became his lender for that portion. The seller would get paid back over time, with interest, rather than receiving all cash at closing.

Why would a seller agree to this? A few reasons:

- Tax advantages (spreading capital gains over time via installment sale)

- Steady interest income

- Motivated sellers who need to move the property more than they need all cash now

3. Closing Cost Credits

Here’s the part that still gets me — he actually walked away from the closing table with a check.

By negotiating seller credits toward closing costs, the seller essentially covered those expenses. Instead of paying to close, he received money.

Net cash out of his pocket on a $1.2 million deal: zero.

What He Did After Closing

Buying the property was just the beginning. The real strategy happened in the 18 months that followed.

Government Grants for Renovation

He applied for city and state renovation grants — the kind that exist specifically to improve aging properties and neighborhoods. These covered a significant portion of his rehab costs.

Philadelphia investors take note: these programs exist here too. PHDC, neighborhood preservation grants, historic tax credits — there are multiple ways to offset renovation costs with public money if you know where to look.

Cash-Out Refinance

Once the property was renovated and stabilized, its value had increased substantially. He went back to the bank with a newly appraised, improved asset and refinanced.

The new loan paid off both the original bank loan AND the seller’s second position note. He extracted equity, eliminated the seller financing, and restructured into a single clean loan.

He was now holding a fully renovated, appreciating asset with conventional long-term financing — and had recovered whatever small costs he’d incurred along the way.

Twenty years later: $5 million.

Is This Still Possible in 2026?

This is the question everyone asks. And the honest answer is: yes, but it’s harder.

What’s the same:

- Seller financing still exists. Motivated sellers still exist. Banks still lend at 70-75% LTV on commercial deals.

- Government grants and renovation programs still exist — Philadelphia has some of the best in the country.

- Creative deal structuring is still legal and still works.

What’s different:

- Interest rates are higher. A seller carrying a second note in 2004 at 6% is a different conversation than today at 8-9%.

- Lenders scrutinize deals more carefully post-2008.

- Finding motivated sellers willing to carry financing requires more work in a market where most sellers have options.

What makes it still possible:

- Distressed properties still exist everywhere

- Estate sales, tax-delinquent owners, out-of-state landlords who just want out

- Philadelphia specifically has a large inventory of properties with motivated sellers and strong grant programs

The investor in this story said something that stuck with me:

“People put limits on themselves. If you’re willing to work harder, there’s always a way to make a deal work without capital.”

That’s not motivational poster talk. That’s someone who proved it on a $1.2 million asset and held it for 20 years.

The Takeaway for Beginners

You don’t need to replicate this exact deal on day one. But understanding how it works changes how you look at every negotiation.

When a seller says their price is firm — that’s when you start asking about terms. Can they carry part of the financing? Can they credit closing costs? Is there flexibility in the structure even if there isn’t flexibility in the number?

The price isn’t always the deal. Sometimes the deal is in how you pay.

Not financial advice — just someone doing a lot of research and asking a lot of questions.