You made it. The renovation is done, the GC has been paid, and you’re standing in a house that actually looks good now. This is the part where all those months of stress either pay off — or teach you something expensive.

Part 3 is about the finish line: selling the property, renting it out, or pulling your cash back out through a refinance if you’re doing BRRRR. Let’s go through each path.

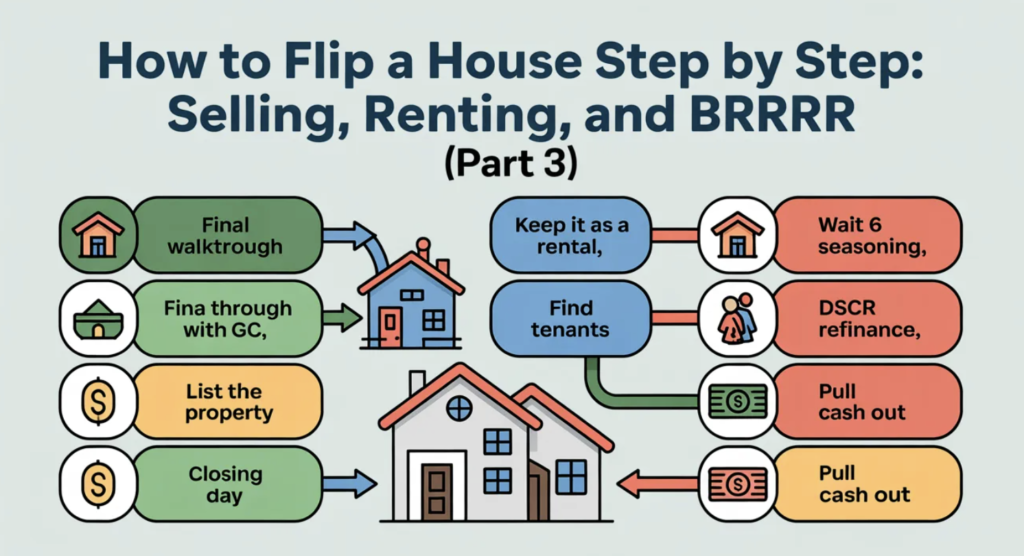

Step 10: The Renovation Is Done — Now What?

Before you do anything else, do a final walkthrough with your GC and go through the punch list. Every single item needs to be complete before you release that final payment. Check:

- All fixtures working (lights, faucets, toilets, appliances)

- Paint clean and consistent throughout

- Floors finished with no gaps or damage

- Doors and windows opening and closing properly

- Exterior and curb appeal — first impressions matter enormously when you’re selling

Once you’re satisfied, release the final draw to your GC.

Now call your realtor.

Step 11: Selling — Do You Use the Same Realtor?

You can — but you don’t have to.

The realtor who helped you buy (your buyer’s agent) is great at finding deals and negotiating purchases. Selling is a different skill set. You want a listing agent who knows how to market properties, stage them correctly, price them strategically, and negotiate offers from buyers.

Sometimes it’s the same person. Sometimes it’s not. Ask your buyer’s agent if they have strong experience on the listing side — look at their recent sales, how long properties sat before selling, and whether they sold close to asking price.

Pricing the property:

Your realtor will pull fresh comps and recommend a listing price. Don’t get emotional about this number — the market decides what the property is worth, not what you need to make. Price it right from the start. Overpriced properties sit, and every extra week costs you hard money interest.

Staging:

You don’t need to go all out, but an empty house is harder to sell than a furnished one. At minimum, consider virtual staging or renting key pieces — a couch, a dining table, a bed frame. It helps buyers visualize the space and consistently leads to faster sales and higher offers.

The selling process timeline:

- List the property

- Showings start (your realtor handles scheduling)

- Offers come in — your realtor presents them, you decide

- Negotiate and accept an offer

- Buyer does their inspection — they may ask for repairs or credits

- Buyer’s financing gets approved (or they pay cash)

- Escrow opens, title search happens

- Closing day — escrow pays off your hard money loan, closing costs come out, and the rest goes to you

From listing to closing typically takes 30-60 days in a normal market, depending on how fast you get an offer and how smooth the buyer’s financing goes.

Step 12: What If You Want to Rent It Instead?

Maybe the market feels soft. Maybe you ran the numbers and the rental cash flow looks better than the flip profit right now. Either way, you’ve decided to keep it and rent it out.

You have two options: find tenants yourself, or hire a property management company.

Finding tenants yourself:

- List on Zillow, Apartments.com, Facebook Marketplace

- Screen applicants — credit check, income verification (ideally 3x monthly rent), rental history

- Draft a lease (use a standard Pennsylvania lease template, or have a real estate attorney review it)

- Collect first month, last month, and security deposit at signing

- Handle maintenance calls yourself

This saves you money but costs you time. If you’re local and have bandwidth, it’s doable — especially for one property.

Hiring a property management company:

A property manager handles everything: advertising the vacancy, screening tenants, collecting rent, handling maintenance requests, dealing with late payments, and if it comes to it — the eviction process.

Their fee is typically 8-12% of monthly rent. On a $1,500/month rental that’s $120-$180/month. For a lot of investors, especially those managing multiple properties or living far away, that’s worth every dollar.

What to look for in a property management company:

- How many units do they currently manage?

- What’s their average vacancy rate?

- How do they handle maintenance — do they have in-house staff or use contractors?

- How do they communicate with owners — monthly statements, online portal?

- What’s their process when a tenant doesn’t pay?

In Philadelphia specifically, tenant protections are strong — evictions take time and have to follow strict legal process. Having a property manager who knows the local rules is genuinely valuable.

Step 13: BRRRR — When Do You Actually Refinance?

If your plan was BRRRR all along — Buy, Rehab, Rent, Refinance, Repeat — the refinance is how you get your cash back out to do it again.

Here’s how the timing works:

Seasoning period:

Most conventional lenders require you to own the property for at least 6 months before they’ll refinance it based on the new appraised value. This is called the seasoning requirement. Some lenders require 12 months. DSCR lenders (more on this in a second) are often more flexible.

So your timeline typically looks like:

- Close on the property

- Renovate (2-3 months)

- Find and place a tenant

- Wait out the seasoning period

- Refinance

DSCR loan vs. conventional refinance:

A conventional refinance looks at your personal income, debt-to-income ratio, tax returns — the full picture of you as a borrower. If your income on paper is low (common for self-employed investors), this can be a challenge.

A DSCR loan (Debt Service Coverage Ratio) doesn’t look at your personal income at all. It looks at whether the rental income covers the mortgage payment. If your rent is $1,500/month and your new mortgage would be $1,100/month, your DSCR is 1.36 — most lenders want to see 1.25 or higher. You qualify based on the property’s income, not yours.

For investors who are self-employed or have complicated tax situations, DSCR is often the more realistic path.

How much cash can you pull out?

Most lenders will refinance up to 75-80% of the appraised value on an investment property. So if your property appraises at $280k, you can refinance up to $210-$224k. If your total project cost was $190k, you get that back — plus a little extra — and your new loan payment is covered by rent.

That’s the whole BRRRR magic: you recycled your capital. Now you go do it again.

Step 14: Final Profit Calculation — What Did You Actually Make?

Let’s put it all together with a real example:

- Purchase price: $140,000

- Renovation cost: $55,000

- Hard money interest + points (6 months): $18,000

- Closing costs (buy + sell): $10,000

- Realtor commission (selling): $16,800 (6% of $280k)

- Total costs: $239,800

- Sale price: $280,000

- Profit: $40,200

Not bad — but notice how much the hard money interest and realtor commissions eat into the number. This is why speed matters on a flip. Every extra month of hard money costs you $2,000-$3,000 in interest. Get in, renovate fast, sell fast.

On taxes:

If you sell within a year of buying, your profit is taxed as ordinary income — same rate as your salary. If you hold longer than a year, you get long-term capital gains rates, which are lower. Most flips happen within a year, so budget for the higher tax rate. Talk to a CPA before your first deal — the tax planning matters.

The Whole Picture

Three parts, one complete process. From running numbers on Zillow to getting a wire transfer at closing — now you know how it actually works.

The goal of this series wasn’t to make it sound easy. It’s not always easy. But it’s also not magic, and it’s not as mysterious as it seems from the outside. It’s a process. Learn the process, find the right people, run the math honestly — and the deals start to make sense.

Philadelphia is full of opportunity right now. The numbers work here in a way they don’t in most major cities. And knowing exactly how the process works — start to finish — puts you miles ahead of most people who say they want to flip houses but never actually start.

Now you have no excuse.

Run your final numbers before you list — use the calculator below to see your real profit after all costs.