When I first started researching DSCR loans, I focused on the obvious stuff — credit score, down payment, DSCR ratio. Those are the things every article talks about.

But there’s one factor that can move your interest rate by 0.50% to 0.75% that almost nobody mentions upfront: the type of property you’re buying.

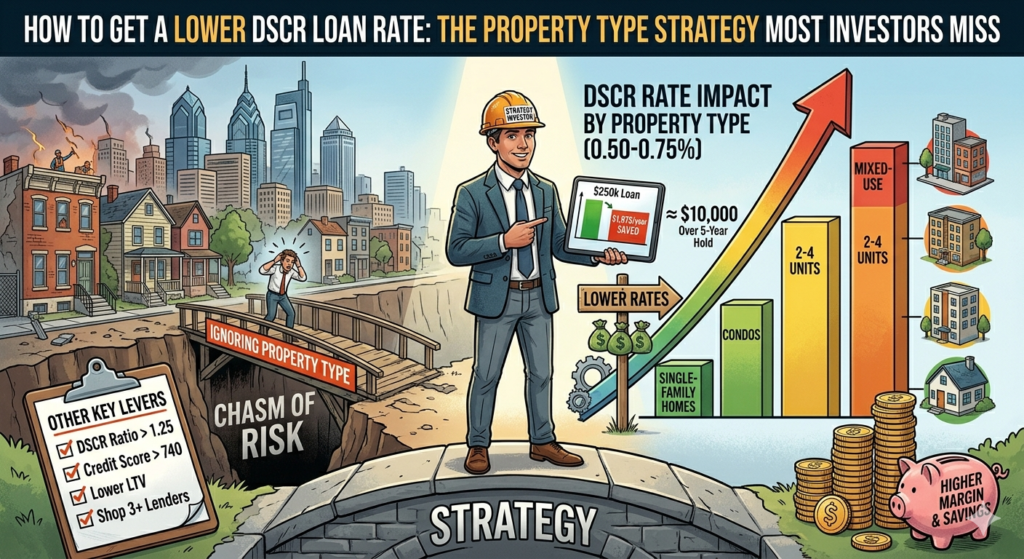

That might not sound like a lot. But on a $250,000 loan, 0.75% is $1,875 per year. Over a 5-year hold, that’s nearly $10,000 — coming directly out of your cash flow.

Here’s what’s actually going on.

Why Property Type Changes Your DSCR Rate

DSCR lenders price loans based on risk. The higher the perceived risk of the property, the higher the rate they charge to compensate.

And different property types carry very different risk profiles in a lender’s eyes — not based on your neighborhood or your renovation quality, but on the fundamental nature of the asset itself.

The logic is simple: in any market condition, some properties are easier to sell and rent than others. Lenders think about what happens if you default. How quickly can they get their money back? The easier the exit, the lower the rate.

The Property Type Hierarchy — Best to Worst Rates

Single-family homes — best rates

Single-family homes get the best DSCR rates across the board. Lenders view them as the lowest risk because they have the broadest buyer and renter pool. In any market — up, down, or sideways — single-family homes sell and rent faster than any other property type.

If you’re looking to optimize your DSCR rate, a single-family rental is your best starting point. The rate advantage over other property types can be 0.50% to 0.75% — which is significant when you’re talking about a loan you might hold for years.

2-4 unit multifamily — slightly higher rates

Duplexes, triplexes, and fourplexes are still residential under most DSCR programs, but they carry a modest rate premium over single-family. The buyer pool is smaller — not everyone wants to be a landlord — and lenders factor that into their pricing.

The cash flow potential is usually better on a 2-4 unit, which can offset the slightly higher rate. But going in, expect to pay more than you would on a comparable single-family deal.

Condos — higher rates, more complications

Condos are tricky for DSCR lenders for a few reasons. First, the resale market is narrower. Second, HOA issues — special assessments, litigation, delinquency rates in the building — can affect the property’s value in ways that are outside your control. Lenders price that uncertainty into the rate.

Some DSCR lenders won’t touch non-warrantable condos at all. If you’re looking at a condo, ask your lender upfront about their condo approval requirements before you get too far into the process.

5+ unit multifamily — different product entirely

Once you cross into 5+ units, you’re out of residential DSCR territory and into commercial lending. Different underwriting, different rates, different requirements. Not necessarily worse — just a completely different product. Don’t assume your residential DSCR lender can do a 10-unit building.

Mixed-use properties — highest rates

Mixed-use — commercial space on the ground floor, residential above — gets the least favorable DSCR rates. The commercial component adds complexity and risk. Vacancy in a retail space is harder to recover from than a residential vacancy. Lenders price that in aggressively.

If you’re buying a mixed-use property in Philadelphia — and there are some interesting ones in neighborhoods like Germantown and Fishtown — go in knowing your financing costs will be higher, and make sure your deal math accounts for it.

What This Means for Philadelphia Investors Specifically

Philadelphia has a lot of multifamily inventory — rowhouses that were converted to duplexes, old triplexes, the occasional mixed-use building on a commercial corridor. It’s part of what makes the market interesting.

But if you’re choosing between a single-family rental and a duplex at a similar price point, the DSCR rate difference is worth factoring into your cash flow analysis. A duplex might generate more gross rent — but if your rate is 0.75% higher, some of that advantage gets eaten up in financing costs.

Run both scenarios. The duplex might still win. But know the actual numbers before you decide.

Other Factors That Move Your DSCR Rate

Property type is the biggest lever most people don’t think about — but it’s not the only one.

DSCR ratio itself — the stronger your cash flow relative to the mortgage payment, the better your rate. A 1.40 DSCR gets better pricing than a 1.05 DSCR. If you’re on the edge, a slightly lower purchase price or a larger down payment can improve your ratio and your rate.

Credit score — above 740 gets you the best pricing tier at most lenders. The difference between a 680 and a 740 can be 0.25-0.50% on its own.

Loan-to-value — more equity means less risk. A 70% LTV loan gets better pricing than an 80% LTV loan. If you have the cash to put more down, it might be worth it on a long-term hold.

Rate shopping — this one is obvious but consistently underutilized. Rate spreads between DSCR lenders on the same file in 2026 routinely run 0.375% to 0.75%. Getting three quotes isn’t courtesy — it’s math.

Prepayment penalty structure — some lenders offer lower rates in exchange for longer prepayment penalties. If you’re planning a long hold, a 5-year step-down might be fine. If you’re planning to sell or refinance within two years, a shorter penalty period might be worth paying a slightly higher rate for.

The Bottom Line

DSCR loan rates aren’t fixed — they’re negotiated, and they’re heavily influenced by decisions you make before you ever talk to a lender. Choosing the right property type, optimizing your DSCR ratio, and shopping multiple lenders can move your rate by a full percentage point or more.

On a long-term rental hold, that’s tens of thousands of dollars over the life of the loan.

Know the levers before you pull the trigger on a property.

Use the DSCR Calculator below to see how your property type and cash flow ratio affect your qualifying numbers.