LTV real estate investing decisions aren’t just about how much you can borrow. They’re about which kind of money matters more to you right now.

There’s a default assumption in real estate investing that goes something like this: borrow as much as the lender will give you, pull out as much equity as possible, and use that cash to buy the next property. More leverage, more properties, more wealth.

For a certain phase of portfolio building, that logic makes sense. But I came across a conversation between a father and son investor that made me think harder about the other side of that equation — and the son’s reasoning on his most recent deal is worth unpacking carefully.

The Deal That Made Me Rethink LTV Real Estate Investing

The son owns six properties. On his most recent acquisition, he deliberately borrowed significantly less than he could have.

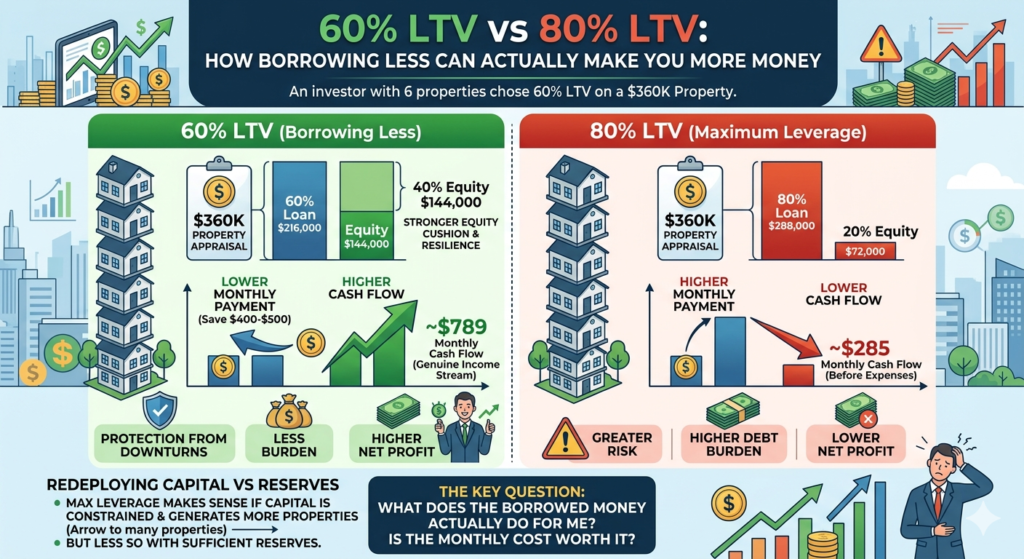

Here’s the setup. Total all-in cost: around $204,000–$205,000. Appraisal came back at $360,000 — higher than the $325,000 he’d originally projected.

At 80% LTV — the typical maximum for a conventional investment property loan — he could have pulled out $288,000. That would have returned his entire purchase price plus significant additional cash.

He didn’t do that. Instead, he borrowed at 60% LTV — $216,000 against the $360,000 appraised value. He left 40% equity sitting in the property.

His tenant pays $2,300 a month. With the lower loan amount, his monthly payment dropped enough that he’s saving $400–$500 per month compared to what an 80% LTV payment would have been.

The Math on LTV Real Estate Investing — Month to Month

Let’s look at what the difference actually means.

At 80% LTV on a $360,000 appraised value, you’re borrowing $288,000. At 7.5% on a 30-year loan, that’s roughly $2,015 per month in principal and interest — before taxes, insurance, and property management.

At 60% LTV, you’re borrowing $216,000. Same rate, same term — that payment drops to approximately $1,511 per month.

That’s roughly $500 per month in difference.

Against $2,300 in monthly rent:

- 80% LTV scenario → ~$285 cash flow before expenses

- 60% LTV scenario → ~$789 cash flow before expenses

That’s not a small difference in LTV real estate investing outcomes. That’s the difference between a property that feels like a burden and one that genuinely contributes to your financial picture every month.

When Maximum Leverage Makes Sense

I want to be clear — I’m not saying 80% LTV is wrong. There are situations where pulling maximum equity is absolutely the right move.

If you’re in active portfolio-building mode and every dollar of capital you redeploy can generate another cash-flowing property, leverage is your friend. The BRRRR strategy exists precisely because recycling capital efficiently accelerates growth faster than any other method.

If you’re early in your investing career and capital is the constraint — meaning the only thing stopping you from buying the next deal is cash — then pulling equity makes sense.

When Conservative LTV Real Estate Investing Makes Sense

But there’s a different phase where the calculus shifts. The son in this conversation was clearly in that phase.

When you already have enough capital reserves that additional cash doesn’t meaningfully change your options, the higher monthly payment just becomes friction. You’re paying more every month to hold money you don’t need.

When your portfolio has grown to the point where stability matters — six properties, multiple tenants, multiple moving parts — predictable cash flow becomes more valuable than maximum leverage.

When interest rates are high enough that the spread between your borrowing cost and your return on that borrowed capital is thin, the risk-reward on maximum LTV real estate investing gets less attractive.

He had all three conditions at once. So he borrowed less, kept payments manageable, maintained strong cash flow, and preserved a significant equity cushion.

The Equity Cushion Argument

Leaving 40% equity in a property isn’t just about monthly cash flow — it’s also a risk management decision.

If the market softens and property values drop 15–20%, an investor at 80% LTV is suddenly uncomfortably close to being underwater. An investor at 60% LTV has a lot more room before that becomes a real problem.

If a major repair comes up — roof, HVAC, foundation — an investor with tight cash flow and maximum leverage is in a difficult position. An investor with strong monthly cash flow and equity reserves has options.

According to the Mortgage Bankers Association, investors who maintained lower LTV ratios during the 2008 downturn were significantly more likely to hold their portfolios intact through the correction — while highly leveraged investors were forced to sell at the worst possible time.

What This Means for My Own LTV Real Estate Investing Roadmap

I’m still in earlier stages — getting back into flipping, building toward multifamily and eventually development. Right now, capital efficiency is the priority. Every dollar I can redeploy into the next deal matters.

But I’m filing this conversation away, because there’s going to come a point where the goal shifts from building the portfolio to stabilizing it. And when that point comes, the instinct to borrow maximum leverage needs to be questioned rather than assumed.

The son isn’t leaving money on the table. He’s choosing which kind of money matters more to him right now — a lump sum he doesn’t need, or $500 a month he’ll actually feel every single month for the life of the loan.

That’s not a bad trade.

Use the Rental Property ROI Calculator to run both scenarios on your next deal — 60% LTV vs 80% LTV — and see exactly what the monthly cash flow difference means before you decide how much to borrow.

Not financial advice — just someone doing a lot of research and asking a lot of questions.